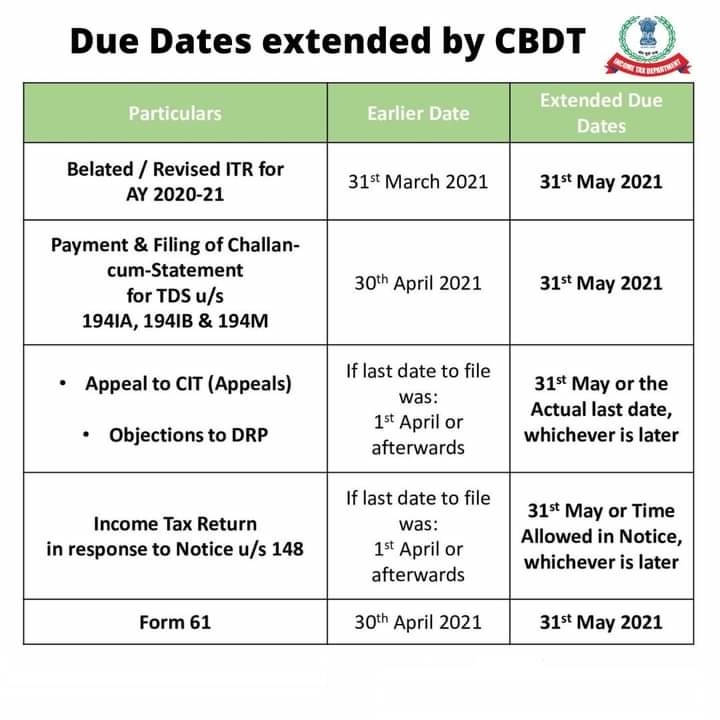

Last chance to revise ITR for financial year 2019-20

In view of the adverse circumstances arising due to the severe Covid-19 pandemic and also in view of the several requests received from taxpayers, tax consultants & other stakeholders from across the country, requesting that various compliance dates may be relaxed, the Government has extended certain timelines on Saturday.

In the light of multiple representations received (supra) and to mitigate the difficulties being faced by various stakeholders, the Central Board of Direct Taxes (CBDT) has, under section 119 of the Income-tax Act, 1961(the Act), provided the following relaxation in respect of compliances by the taxpayers:

a) Appeal to Commissioner (Appeals) under Chapter XX of the Act, for which the last date of filing under that Section is 1st April, 2021 or thereafter, may be filed within the time provided under that Section or by 31st May, 2021, whichever is later;

b) Objections to Dispute Resolution Panel (DRP) under Section 144C of the Act, for which the last date of filing under that Section is 1st April, 2021 or thereafter, may be filed within the time provided under that Section or by 31st May, 2021, whichever is later;

c) Income-tax return in response to notice under Section 148 of the Act, for which the last date of filing of return of income under the said notice is 1st April, 2021 or thereafter, may be filed within the time allowed under that notice or by 31st May, 2021, whichever is later;

d) Filing of belated return under sub-section (4) and revised return under sub-section (5) of Section 139 of the Act, for Assessment Year 2020-21, which was required to be filed on or before 31st March, 2021, may be filed on or before 31st May, 2021;

e) Payment of tax deducted under Section 194-IA, Section 194-IB and Section 194M of the Act, and filing of challan-cum-statement for such tax deducted, which are required to be paid and furnished by 30th April, 2021(respectively) under Rule 30 of the Income-tax Rules, 1962, may be paid and furnished on or before 31st May, 2021;

f) Statement in Form No. 61, containing particulars of declarations received in Form No.60, which is due to be furnished on or before 30th April, 2021, may be furnished on or before 31st May, 2021.

The above relaxations are the latest among the recent initiatives taken by the Government to ease compliances to be made by the taxpayers with the aim to grant respite during these difficult times.