MCA has further revised/ increased the ‘paid-up capital’ and ‘turnover’ thresholds applicable in the case of ‘small companies’ under the Companies Act, 2013, to reduce compliance burden for more number of companies to be treated as ‘small companies’, as part of ‘ease of doing business’ initiative.

Earlier, the definition of “small companies” under the Companies Act, 2013 was revised by increasing these thresholds, i.e. paid up capital threshold was increased from not exceeding Rs 50 lakh to Rs 2 crore and turnover threshold was increased from not exceeding Rs 2 crore to Rs 20 crore.

These thresholds, now have been further revised/ increased to amend the definition of small companies, so that more number of companies can be treated as ‘small companies’, eventually to reduce their compliance burden. Now the paid up capital threshold has been increased from not exceeding Rs 2 crore to Rs 4 core and turnover threshold has been increased from not exceeding Rs 20 crore to Rs 40 crore, which effectively means that number of small companies will increase substantially.

In the recent past, MCA has taken several initiatives/ measures in the direction of ease of doing business for corporates, like decriminalization of various provisions of the Companies Act, 2013/ LLP Act, 2008, extending fast track mergers to start ups, incentivizing incorporation of One Person Companies (OPCs) etc.

Lakhs of small companies significantly contribute to the growth of Indian economy and generation of employment. Therefore, Government is making continuous efforts by such initiatives/ measures which create a more conducive business environment for law-abiding small companies, by reducing their compliance burden so that they can focus more on their core business.

It may be noted that small companies are eligible for certain benefits/ relaxations, in the form of reduced compliance burden, some of which are listed hereunder:

i) No need to prepare cash flow statement by small companies, forming part of financial statement,

ii) Advantage of preparing and filing an Abridged Annual Return,

iii) Mandatory rotation of auditor not required,

iv) An Auditor of a small company is not required to report on the adequacy of the internal financial controls and its operating effectiveness in the auditor’s report,

v) Holding of only two board meetings in a year,

vi) Annual Return of the company can be signed by the company secretary, or where there is no company secretary, by a director of the company,

vii) Lesser penalties for small companies, etc.

In view of the fact that ‘paid up capital’ and turnover’ thresholds applicable for ‘small companies’ under the Companies Act, 2013 have been further revised/ increased, this will allow more number of companies to enjoy relaxation from certain compliance burdens.

The Double Tax Avoidance Agreement (DTAA) is essentially a bilateral agreement entered into between two countries. The basic objective is to promote and foster economic trade and investment between two Countries by avoiding double taxation.

WHAT IS DOUBLE TAXATION OF INCOME?

When the same income is taxed more than once, due to levying of tax by two or more jurisdictions, on the same income asset or financial transaction, this results in double taxation. This may happen, when an assessee – an Individual or a company, is taxed more than once for the same income in India, either on the basis of place of residence or on the basis of source of accrual, which leads to double taxation.

Countries have started entering into Double Taxation Avoidance Agreements (DTAA) with other countries to resolve double taxation issue so as to ease out the tax burden of their taxpayers. This relief for taxes paid in foreign country is given to taxpayer while taxing the same income in India, which is termed as Foreign Tax Credit (FTC).

B. HOW DOUBLE TAXATION AVOIDANCE AGREEMENT (DTAA) WORKS?

In any country, the tax is levied based on 1) Source Rule and 2) the Residence Rule.

The source rule holds that income is to be taxed in the country in which it originates irrespective of whether the income accrues to a resident or a non-resident whereas the residence rule stipulates that the power to tax should rest with the country in which the taxpayer resides.

If both rules apply simultaneously to a business entity and it were to suffer tax at both ends, the cost of operating on an international business would become prohibitive and would deter the process of globalization. It is from this point of view that Double Taxation Avoidance Agreements (DTAA) have become significant.

Where the Central Government has entered into an agreement with the Government of any country outside India or specified territory outside India, for granting relief of tax, or as the case may be, avoidance of double taxation, then, in relation to the assessee to whom such agreement applies, the provisions of this Act shall apply to the extent they are more beneficial to that assessee.

Impact of Double Taxation Avoidance Agreement:

1. WHERE DTAA EXISTS (SECTION 90):

There are two methods of granting relief under Double Taxation Avoidance Agreement.

Exemption method – A particular income is taxed in one of the both countries and exempted in the other

Example- For the Income from Dividend, Interest, royalty and fees for technical services Source Rule is applicable in treaty with Greece, Libyan and United Arab Republic. So for citizen of these 3 countries if the dividend, interest, royalty or fees for technical services is arising in India, then it will be solely taxable in India only and for a resident if such income is arising in any of these 3 countries then the income will solely be taxed in these 3 countries and it will not at all be taxable in India.

Tax Credit method- The income is taxed in both the countries as per the treaty and the country of residence will allow the tax credit / reduction for the tax charged in the country of Origin.

Example- Mr. A (an Indian resident) has received salary from a US company for job in US. Since Mr. A is a resident so his global Income will be taxable in India. In this case, source country is US (since the service has been rendered in US) and resident country is India. So at the time of computation of tax liability of Mr. A, the tax paid in US will be allowed as set off against his total tax liability but limited to the tax payable on such foreign income at Indian tax rates.

Therefore DTAA determines which method to be used first and, if the income is taxable only in one country then exemption method shall be used, but if the same is taxable in both countries then tax credit method comes into play.

In case where Bilateral agreement has been entered under section 90 of the Income Tax Act, 1961 with a foreign country then the assessee has an option either to be taxed as per the Double Taxation Avoidance Agreement (hereinafter referred as “DTAA”) or as per the normal provisions of Income Tax Act 1961, whichever is more beneficial to assessee.

Example- As per DTAA between India and Germany, tax on Interest is specified @ 10% whereas under Income Tax Act 1961, it depends on slab rates for individuals & HUF and flat rates (generally 30%) for other kind of assessees (like firm, company etc). Hence, one can follow DTAA and pay tax @ 10% only.

2. WHERE DTAA DOES NOT EXIST (SECTION 91):

i. If any person who is resident in India in any previous year, in respect of income which arose outside India (and which is not deemed to accrue or arise in India), and paid in any country with which there is no agreement under section 90 for the relief or avoidance of double taxation, then he shall be entitled to the deduction from the tax payable in India,

ii. Deduction shall be lower of:

Tax calculated on such double taxed income at the Indian rates.

Tax calculated on such double taxed income at the rate of tax of the said country

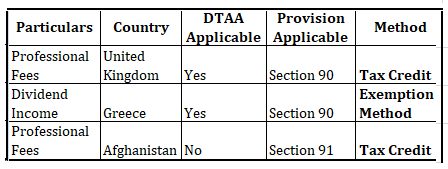

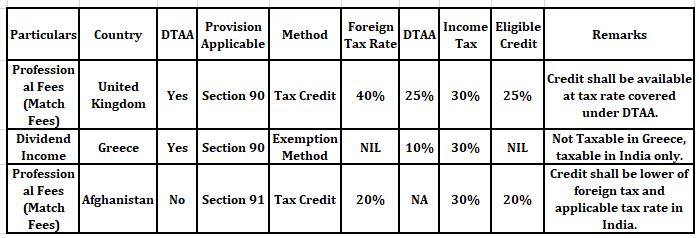

Example :Suppose Indian Sportsman, resident of India who earns foreign income in form of match fees being professional and dividend income as his other foreign income from the below mentioned countries, then in such case following provisions and method shall govern his taxability:

Therefore, both Tax Credit method u/s 90 and Section 91 deals with Foreign Tax Credit, but still having DTAA is beneficial because assessee is taxed at rate beneficial to him, which is not so in case of NO DTAA.

C. HOW CREDIT OF FOREIGN TAX IS AVAILED IN INDIA?

Rule 128 governs the credit of taxes paid on income earned in foreign country. An assessee shall be eligible to claim credit of foreign tax paid if he complies with provisions stated under Rule 128 of the Income Tax Rules which are discussed as follows:

1. Analysis of Rule 128 introduced under Indian Income Tax Rules

Applicability of the rules

The rules came into force with effect from 1.4.2017 applicable only for resident assessee for the amount of foreign taxes paid by him in a foreign country. The credit is available only if income corresponding to the taxes is offered for tax or assessed to tax in India during the year in which the credit is claimed.

In the cases where the income for which the foreign taxes paid or deducted is offered to taxes for more than one year, the credit will be given across the years in the same proportion to which the income is offered to tax in India during the year in which credit is claimed.

2. Foreign Tax Credit Defined under sub-rule 2:

i. FTC in case of DTAA countries: Taxes that are covered under the said agreement.

ii. FTC in case of other countries (No DTAA): Tax payable under the law in force in that country in the nature of income-tax referred in Section 91.

The LOWER OF tax payable under the act on such income or the foreign tax paid is eligible as FTC. However, while considering the foreign tax paid, it cannot exceed the amount arrived as per DTAA with that country.

3. Utilization of Foreign Tax Credit:

FTC is eligible for adjustment against the tax, surcharge and cess payable under the IT Act. FTC cannot be adjusted against interest, fee or penalty payable under the IT Act. FTC is not available in case foreign tax or part thereof is disputed by the assessee in any manner.

4. Exception & Conditions relating to Foreign Tax Credits:

Credit is allowed in the year in which the income is offered/assessed in India upon the assessee within six months from the end of the month in which dispute is finally settled and assessee furnishes:

Evidence of settlement of dispute

Evidence that the liability for payment of such foreign tax has been discharged and

Undertaking that no refund in respect of such amount is directly or indirectly been claimed. Further, credit for each source of income shall be calculated separately for a specific country and then aggregated. The rate of exchange to be taken for this purpose is TT buying rate on the last day of the month immediately preceding month in which the tax is paid or deducted.

5. Documents required under Foreign Tax Credit:

Furnish FORM 67 duly verified and certified by a Chartered Accountant on or before furnishing return of income u/s 139(1)

Furnishing following certificates or statement specifying:

Nature of income and,

Amount of Tax paid of which statement given by:

Tax authority of that country, or

Person responsible for deduction of such tax, or

Signed by the assessee:

In this case, it should be accompanied with – an acknowledgment of online payment or receipt or bank counterfoil for proof of payment of tax, if tax is paid by the assessee

In case of tax deduction, proof of such Tax deducted at source

D. JUDICIAL PRECEDENTS UNDER FOREIGN TAX CREDIT

1. WIPRO LIMITED F TS – 565 – HC – 2015 (KAR)

The judgment of WIPRO provides that merely because the taxpayer’s income is exempt from tax due to a limited tax holiday provided under the ITA, does not mean that foreign tax credit can be simply denied.

2. TATA SONS [2011] 43 SOT 27 (MUM AT)

Though DTAA with USA provides credit only the tax paid with the Federal Government, credit was extended to the Taxes paid to State taxes as well. It has considered the relief u/s 91 which was beneficial to the assessee than that of the DTAA.

3. VIJAY ELECTRICALS [2015] 54 COM 19 (HYD AT)

Tax credit is available even if the same is not deposited with the overseas Government in the year in which the income is taxable.

Taxpayers can make GST payments through challan every month either by self-assessment of monthly liability or 35 per cent of net cash liability of previous filed GSTR-3B of the quarter. Quarterly GSTR-1 and GSTR-3B can also be filed through an SMS.

The government has launched the Quarterly Return Filing and Monthly Payment of Taxes (QRMP) scheme in a bid to ease the return filing experience of the Goods and Services Tax (GST) taxpayers. The scheme will come into effect from January 1, 2021, it will impact 9.4 million taxpayers, who constitute 92% of the total tax base of GST and have an annual aggregate turnover (AATO) of up to Rs 5 crore.

With the introduction of the QRMP scheme, sources say, small taxpayers would need to file only eight returns – four each GSTR-3B and GSTR-1 – instead of the existing requirement of 16 returns in a financial year, of which 12 are GSTR-3B. The new scheme would also significantly reduce taxpayers’ professional expenses on return filing as they would have to file just half the number of returns as against the current requirement of 16. Also, the QRMP scheme would be available on the common GST portal with the facility to opt-in and opt-out, and opt-in again, as per a taxpayer’s wishes.

The scheme would bring in the concept of providing input tax credit (ITC) only on the reported invoices, thus putting a curb on the menace of fake invoice frauds. Additionally, the QRMP scheme is also likely to have the optional feature of Invoice Filing Facility (IFF) to mitigate the business-related hardships of the small and medium taxpayers. Under the IFF, taxpayers who opt to file their returns quarterly would be able to upload and file such invoices even in the first and second month of the quarter for which there is a demand from the recipients.

The taxpayers won’t need to upload and file all the invoices of the month. Only those invoices, which are required to be filed in IFF as per the recipients’ demands, are to be uploaded. The remaining invoices of the first and second months can be uploaded in the quarterly GSTR-1 return.

The QRMP scheme is based on the existing return system with suitable modifications in a bid to give much-needed flexibility to the small and medium enterprises with regards to GST compliance. It was approved in principle by the GST Council in its 42nd meeting on October 5, 2020.

The Direct Tax Vivad se Vishwas Act, 2020 was enacted on March 17, 2020 to settle direct tax disputes locked up in various appellate forums.

The Ministry of Finance has extended the deadline for making a declaration under Vivad Se Vishwas Scheme till 31′ January, 2021 from 31st December, 2020.

The Ministry of Finance has extended the deadline for making a declaration under Vivad Se Vishwas Scheme till 31′ January, 2021 from 31st December, 2020.

The date for the passing of order or issuance of notice by the authorities under the Direct Taxes & Benami Acts which are required to be passed/ issued/ made by 30th March 2021 has also been extended to 31st March 2021.

The Vivad se Vishwas scheme was announced by Union Finance Minister Nirmala Sitharaman during her budget speech on February 1, 2020.

Given below are all the aspects you have to know about this amnesty scheme: Under this scheme, taxpayers whose tax demands are locked in dispute in multiple forums, can pay due to taxes by March 31, 2020, and get a complete waiver of interest and penalty.

If a taxpayer is not able to pay within the deadline, he gets a further time till June 30, but in that case, he would have to pay 10% more on the tax.

For improving the ease of doing business in India and to reduce the cost of compliance, RBI has made a review of requirements of submission of various forms and reports under FEMA and has decided to discontinue submission of 17 such returns/ reports with immediate effect.

Discontinuation of Returns/ Reports under Foreign Exchange Management Act, 1999

1. The attention of Authorised Persons is invited to the Master Direction- Reporting under Foreign Exchange Management Act, 1999 dated January 01, 2016, as amended from time to time, and other reporting related instructions issued by the Reserve Bank of India.

2. With a view to improve the ease of doing business and reduce the cost of compliance, the existing forms and reports prescribed under FEMA, 1999, were reviewed by the Reserve Bank. Accordingly, it has been decided to discontinue the 17 returns/ reports as listed in the Annexure with immediate effect.

3. The Master Direction- Reporting under Foreign Exchange Management Act, 1999 dated January 01, 2016, shall accordingly be updated to reflect the above changes. AD banks may bring the contents of this circular to the notice of their constituents.

4. The directions contained in this circular have been issued under Section 10(4) and 11(2) of the Foreign Exchange Management Act, 1999 (42 of 1999) and are without prejudice to permissions/ approvals, if any, required under any other law.

List of Discontinued Reports

Sl. No.

Name of Report

Reporting Entity

Frequency

1

Category-wise transaction where the amount exceeds USD 5000 per transaction

AD Category-II

Monthly

2

Category-wise, transaction-wise statement where the amount exceeds USD 25,000 per transaction

AD Category- II

Monthly

3

Statement of Purchase transactions of USD 10,000 and above (including transactions of their franchisees)

FFMCs and AD Category- II

Monthly

4

Extension of Liaison Offices (LOs)

AD Category-I banks

As and when extension is granted

5

Extension of Project Offices (POs)

AD Category-I banks

As and when extension is granted

6

FII/FPI daily: Daily inflow/outflow of foreign fund on account of investment by FPIs

AD banks

Daily

7

FII/FPI Return (Monthly): Data relating to actual inflow/ outflow of remittances on account of investments by Foreign Institutional Investors (FIIs) in the Indian Capital market

AD Category-I banks

Monthly

8

FVCI reporting: Inflows/outflows of remittances on account of investments by Foreign Venture Capital Investor (FVCIs) and Market value of Investments made by FVCIs

AD Category-I banks/Custodian banks

Monthly

9

Reporting of Inflow/ Outflow details in respect of Mutual Fund by Asset Management Companies

Asset Management Companies

Quarterly

10

Market value of FII Investment in India on fortnightly basis

AD Category-I banks

Fortnightly

11

Market value of FII Investment in India on Monthly basis

AD Category-I banks

Monthly

12

FII holdings as percentage of floating stock

AD Category-I banks

Monthly

13

Form DRR for Issue/ transfer of sponsored/ unsponsored Depository Receipts (DRs)-Hardcopy**

Custodian

At the time of issue/transfer of depository receipts

14

ADR/ GDR Movement Report- two way fungibility

AD Category-I banks

Monthly

15

Repatriation of Sales proceeds of underlying shares represented by FCCBs/ GDRs/ ADRs

Custodian

Monthly

16

GDR/ ADR underlying shares issued, re deposited and released monthly reporting

Custodian

Monthly

17

Monitoring of disinvestments by Overseas Corporate Bodies

AD banks

Monthly

** Please note that it is only the hardcopy filing of form DRR that has been discontinued. The domestic custodian may continue to report the form DRR on FIRMS application in terms of Regulation 4(5) of FEM (Mode of Payment and Reporting of Non-Debt Instruments) Regulations, 2019.

In a statement, the Department of Revenue (DoR) reiterated that there will be no extra compliance burden on the taxpayers for GST turnover displayed in the Form 26AS, which is an annual consolidated tax statement that can be accessed from the income-tax website by taxpayers using their Permanent Account Number (PAN).

Prime Minister Narendra Modi launched GST into operation on the 1 st of July, 2017. GST was publicised as ‘one nation, one tax’ by the government, aimed to provide a simplified, single tax regime. GST is a dual levy where the Central Government levies and collects Central GST (CGST) and the State levies and collects State GST (SGST) on intra-state supply of goods or services. Centre also levies and collects Integrated GST (IGST) on inter-state supply of goods or services. The GST Portal is a website where all the compliance activities of GST can be done before and after GST login. Activities such as the GST registration return filing, payment of taxes, application for refund, etc. can be done on the GST Portal.

GSTN, recently launched many new features on GSTN portal. One of its features is that GSTN portal is now showing aggregate annual turnover for previous financial year after logging in to the portal.

The GST turnover is being shown in 26AS just for the information of the taxpayer. DoR acknowledged that there may be some differences in GSTR-3Bs filed and the GST shown in the Form 26AS but it can’t happen that a person shows turnover of crores of rupees in GST and doesn’t pay a single rupee of income tax.

The DoR said that the notified Income Tax Return for the current AY 2020-21 already requires reporting of GST outward supplies in the Schedule GST.

Therefore, the information displayed in Form 26AS would provide ease of compliance to the taxpayers in filling Schedule GST.

The revenue department has noticed that many unscrupulous persons are trying to avail or pass on input tax credit fraudulently by generating fake invoices and has already formulated a strategy for identifying these fake invoice generators which inter alia takes into account the income tax profiles of the suspected fake invoice generators.

These persons in most of the cases never file their income tax returns or disclose very meagre taxable income in the income tax return.

The suspected fake invoice generators are being identified for serious action under GST and other laws including suspension of their GST registration based on the fact that whether their income tax payment commensurate with the expected profit margin on turnover reported by them in the GST returns, the DoR said.

What “aggregate turnover” means?

“Aggregate turnover” is the aggregate value of all taxable supplies, exports of goods or/and services or both, exempt supplies and interstate supplies of persons having the same PAN, to be computed on all India basis. However, such taxable supplies do not include the value of inward supplies on which GST is being paid under reverse charge basis. The aggregate turnover also excludes Central tax, State tax, Union territory tax, Integrated tax and cess.

Basically, sum of the following shall be considered as an aggregate turnover:

Value of all taxable supplies of goods and services

Value of all Inter-state supplies

Value of all exempt supplies of goods and services

Value of all export of goods or services or both

However, the following items would be excluded from Turnover:

Inward supplies on which taxes are paid under reverse charge

Taxes and cesses under GST

Interstate supply of services

Transactions which are neither supply of goods or service.

Supplies provided outside India or received outside India

Extrapolation of Turnover at GSTIN level (for those who have not filed all the returns as per their eligibility or liability)

GSTIN-wise GSTR-3B turnover for FY 2019-2020 has been extrapolated by the formula: >> Total turnover declared as per all GSTR-3B filed / No. of GSTR-3B filed) X No. of GSTR-3B eligible or liable to be filed

GSTIN-wise CMP-08 outward supply has been extrapolated by the formula: >> Total outward supply declared as per all CMP-08 filed / No. of CMP-08 filed) X No. of CMP- 08 eligible or liable to be filed

Added both the values of S. No. (a) and S. No. (b).

For those taxpayers who have filed all the returns as per their respective eligibilities, value of S. No. (c) will be the actual turnover)

Aggregation of extrapolated turnover at PAN level or Annual Aggregate Turnover Resultant values as per S.No. (c) above are aggregated or rolled up at PAN level to arrive at the Annual Aggregate Turnover.

What is the relevance of knowing aggregate turnover?

The aggregate turnover is a crucial parameter for determining the following aspects:

Determining whether registration is required or not-

Aggregate Turnover is relevant for a person to determine threshold limit to obtain registration under GST.

Threshold turnover limit for exclusively supply of goods = Rs 40 lakh (Rs 20 lakh in case of supplies effected from special category states)

Threshold turnover limit for supply of Services or (goods and services both): Rs 20 lakh (Rs 10 lakh in case of supplies effected from special category states)

Determine the limit of composition levy – Threshold limit to opt for composition scheme: Rs 1.5 crore in a financial year (Rs 75 lakh in case of supplies effected from special category states).

To determine a “Taxable person” – Section 2 of CGST Act defines the “taxable person” as a person who has obtained registration or is liable to register as per section 22 and 24 of CGST Act. Here the Section 22 provides a liability to register when the tax payer’s turnover exceeds the limit as determined in certain cases. This is again based on aggregate turnover.

Calculation of Late fee –

Under section 33 any registered taxable person person who fails to file the return u/s 30 i.e Annual return shall be liable to pay late fees of Rs. 100 for every day when such failure continues subject to a maximum of an amount of 0.25% of his aggregate turnover.

This can escalate the amount of late fee because aggregate turnover will include all supplies except reverse charge.

To determine whether Audit is required –

Registered persons with an aggregate turnover exceeding the prescribed GST audit limit of Rs 2 Crore during a financial year are liable for GST Audit. The turnover limit of Rs 2 Crore is same for the registered tax persons across all States and UTs. Thus, no separate turnover limit is defined for Special Category States for GST Audit.

Therefore, it is advised to carry on the computation of aggregate turnover accurately as the same will be used at a number of places which will in turn determine the tax liability of a person.

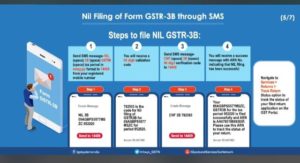

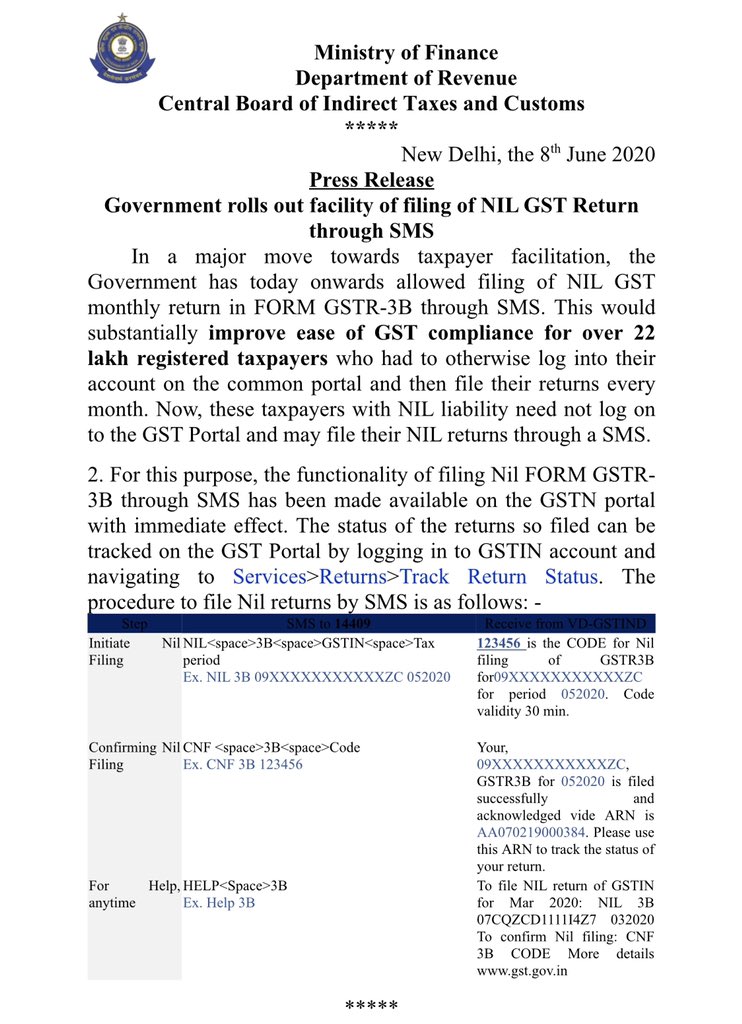

This would substantially improve ease of GST compliance for over 22 lakh registered taxpayers who had to otherwise log into their account on the common portal and then file their returns every month.

In a significant move towards taxpayer facilitation, the Government has today onwards allowed filing of NIL GST monthly return in FORM GSTR-3B through SMS.

This would substantially improve ease of GST compliance for over 22 lakh registered taxpayers who had to otherwise log into their account on the common portal and then file their returns every month.

Now, these taxpayers with NIL liability need not log on to the GST Portal and may file their NIL returns through an SMS.

For this purpose, the functionality of filing Nil FORM GSTR-3B through SMS has been made available on the GSTN portal with immediate effect.

The status of the returns so filed can be tracked on the GST Portal by logging in to GSTIN account and navigating to Services>Returns>Track Return Status.

MCA has further revised/ increased the ‘paid-up capital’ and ‘turnover’ thresholds applicable in the case of ‘small companies’ under the Companies Act, 2013, to reduce compliance burden for more number of companies to be treated as ‘small companies’, as part of ‘ease of doing business’ initiative.

MCA has further revised/ increased the ‘paid-up capital’ and ‘turnover’ thresholds applicable in the case of ‘small companies’ under the Companies Act, 2013, to reduce compliance burden for more number of companies to be treated as ‘small companies’, as part of ‘ease of doing business’ initiative.