Taxpayers can make GST payments through challan every month either by self-assessment of monthly liability or 35 per cent of net cash liability of previous filed GSTR-3B of the quarter. Quarterly GSTR-1 and GSTR-3B can also be filed through an SMS.

The government has launched the Quarterly Return Filing and Monthly Payment of Taxes (QRMP) scheme in a bid to ease the return filing experience of the Goods and Services Tax (GST) taxpayers. The scheme will come into effect from January 1, 2021, it will impact 9.4 million taxpayers, who constitute 92% of the total tax base of GST and have an annual aggregate turnover (AATO) of up to Rs 5 crore.

With the introduction of the QRMP scheme, sources say, small taxpayers would need to file only eight returns – four each GSTR-3B and GSTR-1 – instead of the existing requirement of 16 returns in a financial year, of which 12 are GSTR-3B. The new scheme would also significantly reduce taxpayers’ professional expenses on return filing as they would have to file just half the number of returns as against the current requirement of 16. Also, the QRMP scheme would be available on the common GST portal with the facility to opt-in and opt-out, and opt-in again, as per a taxpayer’s wishes.

The scheme would bring in the concept of providing input tax credit (ITC) only on the reported invoices, thus putting a curb on the menace of fake invoice frauds. Additionally, the QRMP scheme is also likely to have the optional feature of Invoice Filing Facility (IFF) to mitigate the business-related hardships of the small and medium taxpayers. Under the IFF, taxpayers who opt to file their returns quarterly would be able to upload and file such invoices even in the first and second month of the quarter for which there is a demand from the recipients.

The taxpayers won’t need to upload and file all the invoices of the month. Only those invoices, which are required to be filed in IFF as per the recipients’ demands, are to be uploaded. The remaining invoices of the first and second months can be uploaded in the quarterly GSTR-1 return.

The QRMP scheme is based on the existing return system with suitable modifications in a bid to give much-needed flexibility to the small and medium enterprises with regards to GST compliance. It was approved in principle by the GST Council in its 42nd meeting on October 5, 2020.

The Direct Tax Vivad se Vishwas Act, 2020 was enacted on March 17, 2020 to settle direct tax disputes locked up in various appellate forums.

The Ministry of Finance has extended the deadline for making a declaration under Vivad Se Vishwas Scheme till 31′ January, 2021 from 31st December, 2020.

The Ministry of Finance has extended the deadline for making a declaration under Vivad Se Vishwas Scheme till 31′ January, 2021 from 31st December, 2020.

The date for the passing of order or issuance of notice by the authorities under the Direct Taxes & Benami Acts which are required to be passed/ issued/ made by 30th March 2021 has also been extended to 31st March 2021.

The Vivad se Vishwas scheme was announced by Union Finance Minister Nirmala Sitharaman during her budget speech on February 1, 2020.

Given below are all the aspects you have to know about this amnesty scheme: Under this scheme, taxpayers whose tax demands are locked in dispute in multiple forums, can pay due to taxes by March 31, 2020, and get a complete waiver of interest and penalty.

If a taxpayer is not able to pay within the deadline, he gets a further time till June 30, but in that case, he would have to pay 10% more on the tax.

For improving the ease of doing business in India and to reduce the cost of compliance, RBI has made a review of requirements of submission of various forms and reports under FEMA and has decided to discontinue submission of 17 such returns/ reports with immediate effect.

Discontinuation of Returns/ Reports under Foreign Exchange Management Act, 1999

1. The attention of Authorised Persons is invited to the Master Direction- Reporting under Foreign Exchange Management Act, 1999 dated January 01, 2016, as amended from time to time, and other reporting related instructions issued by the Reserve Bank of India.

2. With a view to improve the ease of doing business and reduce the cost of compliance, the existing forms and reports prescribed under FEMA, 1999, were reviewed by the Reserve Bank. Accordingly, it has been decided to discontinue the 17 returns/ reports as listed in the Annexure with immediate effect.

3. The Master Direction- Reporting under Foreign Exchange Management Act, 1999 dated January 01, 2016, shall accordingly be updated to reflect the above changes. AD banks may bring the contents of this circular to the notice of their constituents.

4. The directions contained in this circular have been issued under Section 10(4) and 11(2) of the Foreign Exchange Management Act, 1999 (42 of 1999) and are without prejudice to permissions/ approvals, if any, required under any other law.

List of Discontinued Reports

Sl. No.

Name of Report

Reporting Entity

Frequency

1

Category-wise transaction where the amount exceeds USD 5000 per transaction

AD Category-II

Monthly

2

Category-wise, transaction-wise statement where the amount exceeds USD 25,000 per transaction

AD Category- II

Monthly

3

Statement of Purchase transactions of USD 10,000 and above (including transactions of their franchisees)

FFMCs and AD Category- II

Monthly

4

Extension of Liaison Offices (LOs)

AD Category-I banks

As and when extension is granted

5

Extension of Project Offices (POs)

AD Category-I banks

As and when extension is granted

6

FII/FPI daily: Daily inflow/outflow of foreign fund on account of investment by FPIs

AD banks

Daily

7

FII/FPI Return (Monthly): Data relating to actual inflow/ outflow of remittances on account of investments by Foreign Institutional Investors (FIIs) in the Indian Capital market

AD Category-I banks

Monthly

8

FVCI reporting: Inflows/outflows of remittances on account of investments by Foreign Venture Capital Investor (FVCIs) and Market value of Investments made by FVCIs

AD Category-I banks/Custodian banks

Monthly

9

Reporting of Inflow/ Outflow details in respect of Mutual Fund by Asset Management Companies

Asset Management Companies

Quarterly

10

Market value of FII Investment in India on fortnightly basis

AD Category-I banks

Fortnightly

11

Market value of FII Investment in India on Monthly basis

AD Category-I banks

Monthly

12

FII holdings as percentage of floating stock

AD Category-I banks

Monthly

13

Form DRR for Issue/ transfer of sponsored/ unsponsored Depository Receipts (DRs)-Hardcopy**

Custodian

At the time of issue/transfer of depository receipts

14

ADR/ GDR Movement Report- two way fungibility

AD Category-I banks

Monthly

15

Repatriation of Sales proceeds of underlying shares represented by FCCBs/ GDRs/ ADRs

Custodian

Monthly

16

GDR/ ADR underlying shares issued, re deposited and released monthly reporting

Custodian

Monthly

17

Monitoring of disinvestments by Overseas Corporate Bodies

AD banks

Monthly

** Please note that it is only the hardcopy filing of form DRR that has been discontinued. The domestic custodian may continue to report the form DRR on FIRMS application in terms of Regulation 4(5) of FEM (Mode of Payment and Reporting of Non-Debt Instruments) Regulations, 2019.

In a statement, the Department of Revenue (DoR) reiterated that there will be no extra compliance burden on the taxpayers for GST turnover displayed in the Form 26AS, which is an annual consolidated tax statement that can be accessed from the income-tax website by taxpayers using their Permanent Account Number (PAN).

Prime Minister Narendra Modi launched GST into operation on the 1 st of July, 2017. GST was publicised as ‘one nation, one tax’ by the government, aimed to provide a simplified, single tax regime. GST is a dual levy where the Central Government levies and collects Central GST (CGST) and the State levies and collects State GST (SGST) on intra-state supply of goods or services. Centre also levies and collects Integrated GST (IGST) on inter-state supply of goods or services. The GST Portal is a website where all the compliance activities of GST can be done before and after GST login. Activities such as the GST registration return filing, payment of taxes, application for refund, etc. can be done on the GST Portal.

GSTN, recently launched many new features on GSTN portal. One of its features is that GSTN portal is now showing aggregate annual turnover for previous financial year after logging in to the portal.

The GST turnover is being shown in 26AS just for the information of the taxpayer. DoR acknowledged that there may be some differences in GSTR-3Bs filed and the GST shown in the Form 26AS but it can’t happen that a person shows turnover of crores of rupees in GST and doesn’t pay a single rupee of income tax.

The DoR said that the notified Income Tax Return for the current AY 2020-21 already requires reporting of GST outward supplies in the Schedule GST.

Therefore, the information displayed in Form 26AS would provide ease of compliance to the taxpayers in filling Schedule GST.

The revenue department has noticed that many unscrupulous persons are trying to avail or pass on input tax credit fraudulently by generating fake invoices and has already formulated a strategy for identifying these fake invoice generators which inter alia takes into account the income tax profiles of the suspected fake invoice generators.

These persons in most of the cases never file their income tax returns or disclose very meagre taxable income in the income tax return.

The suspected fake invoice generators are being identified for serious action under GST and other laws including suspension of their GST registration based on the fact that whether their income tax payment commensurate with the expected profit margin on turnover reported by them in the GST returns, the DoR said.

What “aggregate turnover” means?

“Aggregate turnover” is the aggregate value of all taxable supplies, exports of goods or/and services or both, exempt supplies and interstate supplies of persons having the same PAN, to be computed on all India basis. However, such taxable supplies do not include the value of inward supplies on which GST is being paid under reverse charge basis. The aggregate turnover also excludes Central tax, State tax, Union territory tax, Integrated tax and cess.

Basically, sum of the following shall be considered as an aggregate turnover:

Value of all taxable supplies of goods and services

Value of all Inter-state supplies

Value of all exempt supplies of goods and services

Value of all export of goods or services or both

However, the following items would be excluded from Turnover:

Inward supplies on which taxes are paid under reverse charge

Taxes and cesses under GST

Interstate supply of services

Transactions which are neither supply of goods or service.

Supplies provided outside India or received outside India

Extrapolation of Turnover at GSTIN level (for those who have not filed all the returns as per their eligibility or liability)

GSTIN-wise GSTR-3B turnover for FY 2019-2020 has been extrapolated by the formula: >> Total turnover declared as per all GSTR-3B filed / No. of GSTR-3B filed) X No. of GSTR-3B eligible or liable to be filed

GSTIN-wise CMP-08 outward supply has been extrapolated by the formula: >> Total outward supply declared as per all CMP-08 filed / No. of CMP-08 filed) X No. of CMP- 08 eligible or liable to be filed

Added both the values of S. No. (a) and S. No. (b).

For those taxpayers who have filed all the returns as per their respective eligibilities, value of S. No. (c) will be the actual turnover)

Aggregation of extrapolated turnover at PAN level or Annual Aggregate Turnover Resultant values as per S.No. (c) above are aggregated or rolled up at PAN level to arrive at the Annual Aggregate Turnover.

What is the relevance of knowing aggregate turnover?

The aggregate turnover is a crucial parameter for determining the following aspects:

Determining whether registration is required or not-

Aggregate Turnover is relevant for a person to determine threshold limit to obtain registration under GST.

Threshold turnover limit for exclusively supply of goods = Rs 40 lakh (Rs 20 lakh in case of supplies effected from special category states)

Threshold turnover limit for supply of Services or (goods and services both): Rs 20 lakh (Rs 10 lakh in case of supplies effected from special category states)

Determine the limit of composition levy – Threshold limit to opt for composition scheme: Rs 1.5 crore in a financial year (Rs 75 lakh in case of supplies effected from special category states).

To determine a “Taxable person” – Section 2 of CGST Act defines the “taxable person” as a person who has obtained registration or is liable to register as per section 22 and 24 of CGST Act. Here the Section 22 provides a liability to register when the tax payer’s turnover exceeds the limit as determined in certain cases. This is again based on aggregate turnover.

Calculation of Late fee –

Under section 33 any registered taxable person person who fails to file the return u/s 30 i.e Annual return shall be liable to pay late fees of Rs. 100 for every day when such failure continues subject to a maximum of an amount of 0.25% of his aggregate turnover.

This can escalate the amount of late fee because aggregate turnover will include all supplies except reverse charge.

To determine whether Audit is required –

Registered persons with an aggregate turnover exceeding the prescribed GST audit limit of Rs 2 Crore during a financial year are liable for GST Audit. The turnover limit of Rs 2 Crore is same for the registered tax persons across all States and UTs. Thus, no separate turnover limit is defined for Special Category States for GST Audit.

Therefore, it is advised to carry on the computation of aggregate turnover accurately as the same will be used at a number of places which will in turn determine the tax liability of a person.

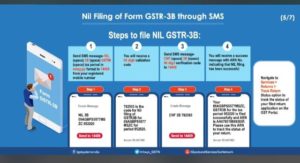

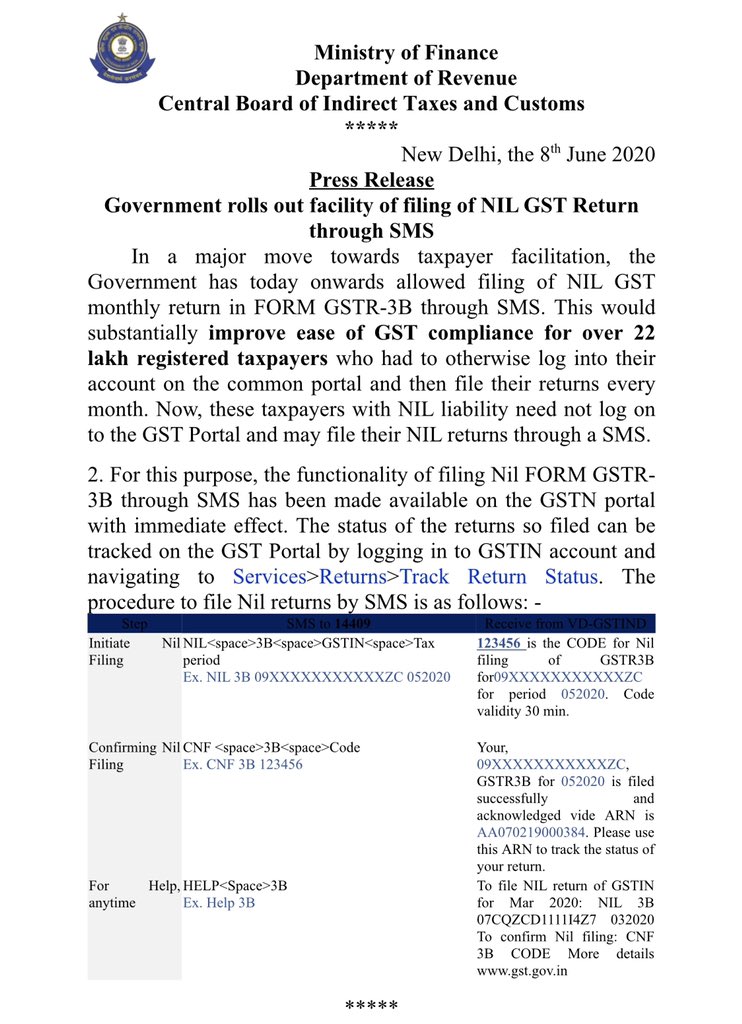

This would substantially improve ease of GST compliance for over 22 lakh registered taxpayers who had to otherwise log into their account on the common portal and then file their returns every month.

In a significant move towards taxpayer facilitation, the Government has today onwards allowed filing of NIL GST monthly return in FORM GSTR-3B through SMS.

This would substantially improve ease of GST compliance for over 22 lakh registered taxpayers who had to otherwise log into their account on the common portal and then file their returns every month.

Now, these taxpayers with NIL liability need not log on to the GST Portal and may file their NIL returns through an SMS.

For this purpose, the functionality of filing Nil FORM GSTR-3B through SMS has been made available on the GSTN portal with immediate effect.

The status of the returns so filed can be tracked on the GST Portal by logging in to GSTIN account and navigating to Services>Returns>Track Return Status.

At as much as 10% of GDP, the big stimulus package did not appear to leave any major sphere untouched.

Over five consecutive days of interaction with the country’s financial media, FM Nirmala Sitharaman provided the break-up of PM Modi’s Rs 20 lakh crore COVID-19 stimulus for India.

At as much as 10% of GDP, the package did not appear to leave any major sphere untouched as Prime Minister Modi brought out the fiscal artillery to complement RBI’s monetary measures spread over the past few weeks, putting India firmly in the league of biggies that have gone all out against the virus.

In his speech, Mr. Modi said his package would focus on land, labour, liquidity and laws, and would deal with such sectors as cottage industries, MSMEs, the working class, middle class and industry. He also talked of focusing on empowering the poor, labourers and migrant workers, both in the organised and unorganised sectors.

Dubbed Atmanirbhar Bharat Abhiyaan, this Covid relief package puts bold reforms at the heart of Modi’s stated plan to make India self-reliant so that any other crisis that may emerge in future could be efficiently tackled. Below we collate all the details that emerged in five tranches over the past five days.

FIRST TRANCHE

MSME measures

Collateral free automatic loans- a move that’ll enable 45 lakh units to restart work and save jobs. 4 year tenor with 12 months moratorium. 100% credit guarantee on principal and interest – Rs. 3 Lakh Crores (60k Cr cover)

Subordinate debt provision of Rs 20,000 crores for 2 lakh stressed MSMEs. Besides, there will be Rs 50,000 crore equity infusion via Mother fund-Daughter fund for MSMEs that are viable but need handholding. A fund of funds with corpus of Rs 10,000 crore will be set up to help these units expand capacity and help them list on markets if they choose.

Definition of MSMEs revised — the move will allow MSMEs to aim for expansion without losing benefits. Differentiation between manufacturing and service units to be removed.

Small units – Investments upto 10 Cr + Turnover upto 50 Cr

Medium units – Investments upto 20 Cr + Turnover upto 100 Cr

Government tenders upto 200 Crores will no longer be on global tender basis. Global tenders will be disallowed for upto 200 Crores. This will make MSMEs eligible to participate in Government purchases.

Post Covid, e-market linkage to be provided for all MSMEs. Receivables by MSMEs from the Central Government and all PSUs will be cleared in next 45 days

For non-bank lenders

Rs 30,000 crore special liquidity scheme for investing in investment grade debt paper of NBFCs, HFCs and MFIs. These NBFCs are those that are also funding MSMEs. These will be fully guaranteed by government of India.

Rs 45,000 crore partial credit guarantee scheme 2.0 for NBFCs. The first 20% loss will be borne by the guarantor that is government of India.

For Discoms, a one-time emergency liquidity injection of Rs 90,000 crore against all their receivables. The states will guarantee it.

For employees

Liquidity relief of Rs 2,500 crore EPF support to all EPF establishments. The EPF contribution will be paid by the govt for another 3 months (till August). It will benefit more than 72 lakh employees.

Statutory EPF contribution for all organisations and their employees covered by EPFO to be reduced to 10% from 12% earlier (This doesn’t apply to govt organisations). This will help infuse Rs 6,750 cr of liquidity into these organisations.

For Power distribution companies

Power distribution companies will get Rs 90,000 crore liquidity against receivables from state-owned Power Finance Corp. and Rural Electrification Corp. This will allow these discoms to pay dues to power producers.

For Contractors & others

An extension of up to 6 months (without costs to contractor) to be provided by all Central Government Agencies like Railways, Ministry of Road Transport & Highways, Central Public Works Dept.

On real estate, urban development ministry will issue advisory to states/UTs so that the regulators can invoke force majeure. The regulators can suo moto extend completion/registration dates for six months for projects expiring on or after March 25, 2020.

A reduction of 25% of existing rates of Tax Deducted at Source (TDS) & Tax Collection at Sources (TCS) from tomorrow till March 31, 2021. This will release Rs 50,000 crores.

Due date of all Income Tax Return filings extended from July 31 to November 30. Vivaad se Vishwas scheme extended till December 31,2020, without any extra payments.

All pending refunds to charitable trusts and non-corporate taxpayers (but including LLP) will be issued immediately

Date of assessments getting barred as on Sep 30, 2020 extended to December 31, 2020. Date of assessments getting barred as on March 31, 2021 extended to September 30, 2021.

SECOND TRANCHE

Focus on migrant workers, small farmers and the poor, in the manner shown below:

Free food for migrants

For those migrants who don’t have NFSA cards or state cards, 5 Kgs of wheat or rice per person and one kg channa per family per month for next two months to be provided and it will reach through the state governments. This will entail Rs 3,500 crore and is likely to benefit around 8 crore migrants.

One Nation, One Ration Card

National Portability Ration Cards can be used in any ration shops that will be applicable across the country. By August 2020, 67 cr beneficiaries in 23 states or 83% of all PDS beneficiaries will get covered. By March 2021, 100 per cent will be covered.

Rental accomodation

Under PM Awas Yojaana, scheme for rental housing for migrant workers. Under the scheme incentives will be offered to private manufacturing units and industrial units to develop affordable housing, converting govt funded houses into affordable renting accommodations for migrant workers. Shall be done on PPP on concessionaire basis. State government agencies will also be incentivised to develop affordable housing.

MUDRA Shishu loan

Those who have availed loans up to Rs 50,000, an interest subvention of 2% for next 12 months after the moratorium period extended by RBI ends. Three crore people will get benefit of Rs 1500 crore.

Street Vendor

Special scheme for street vendors to avail Rs 5,000 crore loan facility. Will be given Rs 10,000 of working capital.

Affordable Housing

Credit-linked subsidy scheme for middle income households in the income group Rs 6-18 Lakh extended to March 2021. The CLSS scheme was operationalised from May 2017 and extended up to March, 2020. Now, it has been extended till March 2021. This will lead to investments of Rs 70,000 crore in housing and kick-start sectors like steel, cement and create jobs.

For Tribals

Rs 6,000 crore worth of proposals have come from states under CAMPA funds. Tribal people will get employment in forest management, wildlife protection/management and other forest related activities.

For Small/Marginal Farmers

The government is extending Rs 30,000 crore additional capital emergency funds through NABARD for post-harvest Rabi and Kharif related activities for small and marginal farmers.

Under the PM Kisan Credit Card, Rs 2 lakh crore of concessional credit to boost farming activities and it will benefit 2.5 crore farmers. Those in animal husbandry and fisheries will also be included.

THIRD TRANCHE

For framers, and such sectors as food processing and allied activities.

For Upgrading Infrastructure

One lakh crore fund for strengthening the farm gate infrastructure like cold chains, post harvest storage infrastructures etc.

Rs 10,000 crore fund for micro food scheme will be executed with cluster based approach. Will benefit 2 lakh Micro Food Enterprises. For instance, Bihar can have Makhana cluster, Kashmir can have Kesar cluster, Telangana can have Turmeric cluster, Andhra can have chilli cluster.

Govt will launch Pradhan Mantri Matsya Sampada Yojana for development of marine and inland fisheries. Rs 20,000 crore will be spent to fill the gaps in value chains. This will lead to an additional fish production of 70 lakh tons in next five years and provide employment to 55 lakh people.

Rs 13,343 crore for vaccination of livestock in India to eradicate foot and mouth disease.

Rs 15,000 crore will be spent on ramping up the dairy infrastructure. Also, investments will be made in cattle feed.

Rs 4,000 crore for growing of herbal and medicinal plants. Ten lakh hectares of land will be used for growing medicinal and herbal plants and will provide income of nearly Rs 5,000 crore for farmers.

Rs 500 crore have been allocated for beekeeping. This will help 2 lakh beekeepers.

TOP to TOTAL: Rs 500 crore for Operation Greens that will be extended beyond tomatoes, potatoes and onion and will applicable to all vegetables.

Proposes amendment to Essential Commodities Act to enable better price realisation for farmers. Food stuffs including edible oils, oilseeds, pulses, onions and potato will be deregulated. And stock limits will be imposed only under exceptional circumstances like famine and surge in prices.

Agriculture Marketing Reforms

32. A central law will be formulated to provide (a) Adequate choices to sell produce at attractive price, (b) Barrier free inter-state trade, and (c) Framework for e-trading of agriculture produce.

Agriculture Produce Price and Quality Assurance

33. Facilitative legal framework will be created to enable farmers for engaging with processors, aggregators, large retailers, exporters etc. in a fair and transparent manner. Risk mitigation for farmers, assured returns and quality standardisation shall form integral part of the framework.

FOURTH TRANCHE

For Upgrading Infrastructure

Included structural reforms in 8 critical sectors- Coal, Minerals Defence Production, Airspace management, Social Infrastructure Projects, Power distribution companies, Space sectors and Atomic Energy.

Coal Sector

Government is introducing the commercial mining of coal. India needs to reduce import of substitutable cal and increase self-reliance in coal production.

34. The investment of Rs. 50,000 crores is for the evacuation of enhanced CIL’s (Coal India Limited) target of 1 billion tons of coal production by 2023-24 plus coal production from private blocks.

Minerals

35. Enhancing private investment in mineral sector.

36. FMalso explained the rationalisation of stamp duty payable at the time of award of mining leases.

37. 500 mining blocks would be offered through an open and transparent auction process, a joint auction of Bauxite & Coal mineral blocks will be introduced to enhance Aluminum industry’s competitiveness.

Defence Production

38. Indigenization of imported spares, separate budget provisioning for domestic capital procurement.

39. FDI limit in defence manufacturing under automatic route is being raised from 49% to 74%.

40. Corporatisation of Ordnance factory board was also announced.

Civil Aviation (Airspace Management, World Class Airports Through PPP, MRO HUB)

41. Restrictions on the utilisation of Indian Air Space will be eased so that civilian flying becomes more efficient.

42. Government is working hard to make India a global hub for for aircraft maintenance, repair and overhaul.

43. Airports Authority of India has awarded 3 airports out of 6 bid for operation & maintenance on (PPP) basis. Additional investment by private players in 12 airports in first & second rounds expected around Rs 13,000 crores.

Power Sector Reforms

44. Power Distribution Companies in Union Territories to be privatised in line with the new tariff policies. This will enable to strengthen industries and bring in efficiency in the entire power sector. This will also enable stability in the sector, announced the FM.

Boosting Private Sector investment

45. Boosting private sector investment in Social Infrastructure through revamped Viability Gap Funding Scheme of Rs 8,100 crores.

Space Sector

46. Boosting private participation in space sectors. Government is working on a liberal geo-spatial policy. Private sector to be co-traveller in India’s space sector journey through launches, satellite services, commented the Finance Minister.

Atomic Energy

47. The government intends to link India’s robust start-up ecosystem to the nuclear sector – Technology Development cum Incubation Centres will be set up for fostering synergy between research facilities and tech entrepreneurs. Establishment of research reactor in PPP mode for production of medical isotopes.

Fifth Tranche

48. MGNREGS: Additional funding of Rs 40,000 crore to the scheme over and above the Budgetary Estimate.

49. Health: All districts will have infectious disease hospitals while at the block-level, public health labs will be set up.

50. Education: PM eVidya programme to be launched immediately. Each Classroom from 1 to 12 will have one TV channel. Special e-content for visually & hearing impaired. Top 100 universities will be permitted to start online courses by May 30, 2020.

51. IBC reforms: Covid-related debt to be excluded from definition of default under the IBC. No fresh insolvency for next one year. Minimum threshold to initiate insolvency raised to Rs one crore from Rs one lakh earlier.

52. Decriminalising Companies Act: Violations under most of the Companies Act to be decriminalised. This will ease the burden on courts and tribunals. Seven compoundable offences under Companies Act being dropped, 5 offences to be dealt under alternative framework.

53. Listing norms: Companies can now list securities directly in foreign jurisdictions

54. New Public Sector Policy: Public sector enterprise policy: All sectors are open to the private sector while public sector enterprises will play an important role in defined areas. Govt will notify strategic areas and in them at least one PSE will remain but private sector will be allowed. In other sectors, PSEs will be privatised.

55. Additional resources to States: Centre has decided to increase borrowing limit of states from 3% to 5% for FY21. This will give extra resources of Rs 4.28 lakh crore to states. This despite, states having borrowed only 14% of the limit authorised to them. 86% remains unutilised. The additional borrowing limit has been linked with initiating reforms.

The finance minister also gave a break up of how the Rs 20 lakh crore was allocated among the five tranches and the previous schemes as well as the RBI measures.

Also coronavirus related debt would be excluded from the definition of “default” under the insolvency and bankruptcy code (IBC)

Finance Minister Nirmala Sitharaman on Sunday raised the minimum threshold to initiate insolvency proceedings to Rs 1 crore from the earlier Rs 1 lakh.

In addition, with an eye on further enhancement of ease of doing business, the government announced suspension of fresh initiation of insolvency proceedings up to one year.

Also corona virus related debt would be excluded from the definition of “default” under the insolvency and bankruptcy code (IBC). “No fresh insolvency proceeding will be initiated up to 1 year.

At the moment MCA has extended this by 6 months, we intend to extend this by another 6 months. For MSMEs a special insolvency framework will be notified under section 240-A of IBC.

The minimum threshold to initiate insolvency proceedings raised to Rs 1 crore from the earlier Rs 1 lakh, which largely insulates MSMEs,” she added.

The Finance Minister, in her fourth presser on Saturday, had announced structural reforms in sectors such as coal, minerals, civil aviation, power distribution, defence production, space, and atomic energy sector.

The reforms were unveiled as a part of the government’s efforts to make India ‘Aatmanirbhar‘ (self-dependent).

Sitharaman has already announced four phases of relief measures to support agriculture, MSMEs, migrant workers, individuals, coal mining, defence, aviation sector, among others amid the ongoing corona virus-induced lock down.