After taking a break from buying into Indian equities in August and September, FPIs bought equities in abundance in November.

Foreign investors pumped over Rs 19,700 crore into the country’s stock markets in November, the highest in eight months, mainly due to government’s plan to recapitalise PSU banks and surge in India’s ranking in the World Bank’s ease of doing business.

In addition, such investors put in Rs 530 crore in the debt markets during the period under review.

According to depositories data, foreign portfolio investors (FPIs) invested a net amount of Rs 19,728 crore in equities last month.

This is the highest net investment by FPIs since March, when they had poured in Rs 30,906 crore in the equity market.It has been a tremendous journey for the Indian equity markets in 2017. After taking a break from buying into Indian equities in August and September, FPIs bought equities in abundance in November.

The strong inflow could be largely attributed to the government’s decision to recapitalise public-sector banks, which is expected to enhance lending and propel economic growth, said Morningstar India’s senior analyst manager (research) Himanshu Srivastava.

“This is particularly seen as a positive step after the questions have been raised from various quarters on the government’s ability to effectively implement economic reforms. Further, the slow pace of economic growth was also believed to be due to rising non performing assets (NPAs) problem in public sector banks, hence this decision provided a much-needed impetus to FPIs to again look back at Indian equity space,” he added.

Finance Minister Arun Jaitley had announced the PSU bank recapitalisation plan of Rs 2.11 trillion, out of which Rs 1.35 trillion will come from recapitalisation bonds, and the rest from markets and budgetary support.

Additionally, the news about India faring well in the World Bank’s Ease of Business index and a jump in core sector growth also turned the tide in India’s favour, Srivastava said.

India gained 30 places in the World Bank’s ease of doing business index for 2018 to 100th among 190 nations.

“These (bank’s recapitalisation plan and world bank’s ranking) and positive developments in the recent times provided a much-needed breather to FPIs who were concerned about the short-term impact of demonetisation and goods and services tax (GST) on the domestic economy and sluggish pace of economic recovery,” he added.

Yet another positive piece of news has come from Moody’s Investor Services, which upgraded its India rating by a notch to ‘Baa2’ from ‘Baa3’ with a stable outlook, citing improved economic growth prospects driven by the government reforms.

Overall, FPIs have invested Rs 53,800 crore in equities so far in 2017 and another Rs 1.46 lakh crore in debt markets.

Around 56% of the registered taxpayers have filed their GSTR-3B returns for October by 20 November, says GSTN

Over 3.9 million assessees filed the summary return for September and over 2.8 million for August.

Taxpayer compliance under the goods and services tax (GST) system is steadily improving with 4.4 million assessees filing summary of the transactions made in October, an improvement of 11% from the filings reported for the previous month, said an official statement from GSTN, the company that processes tax returns.

The statement said the number of taxpayers filing their GSTR 3B returns showed a “marked improvement” with the highest number of assessees filing returns for October till 20th November 2017.

Around 56% of the registered taxpayers have filed their GSTR-3B returns for October by 20 November, it said. The “steady increase” in filings is encouraging, the statement said further, citing chairman Prakash Kumar.

“The trend of taxpayers filing their returns on the last day continues though. Taxpayers are urged to file their returns early to avoid last minute hassles” Kumar said.

Over 3.9 million assessees filed the summary return for September and over 2.8 million for August.

Close to 1.5 million taxpayers filed their returns on 20 November, the highest number of filings in a day.

Punjab topped the list of states in compliance. About 73% of taxpayers in Punjab filed their GSTR 3B returns for October by the deadline.

Federal indirect tax body, the GST Council, has taken a series of steps including deadline relaxations, waiver of late fee, suspension of invoice matching and simplification of forms to encourage voluntary compliance under the new indirect tax regime.

The World Bank’s ease of doing business report showed that eight reforms were key in helping businesses in 2016/17. India is also among the 10 economies to have improved the most, alongside El Salvador, Malawi, Nigeria and Thailand.

Doing business in India became much easier over the past one year because of a raft of policy reforms, an annual World Bank index showed on Tuesday, in what is possibly a shot in the arm for Prime Minister Narendra Modi’s efforts to win big-ticket investments.

For the first time, India jumped 30 places to break into the top 100 in the ease of doing business rankings for the year to June 2017. The 190-country index is an influential barometer of competitiveness among countries that likely also helps businesses make investment decisions.

India’s impressive performance was largely due to reforms in taxation, insolvency laws and access to credit, part of measures Prime Minister Modi’s government has pushed to boost investment and jobs that would help absorb a million people who join the workforce every month.

“India’s performance is not based on efforts of just one year but consistent efforts made over the last three years to continuously improve the regulatory environment of doing business,” Annette Dixon, vice president South Asia, told a press conference.

“It is the result of a number of reforms that the government has undertaken that India is becoming a preferred destination to do business.”

India saw improvements in six of 10 indicators, including on winning construction permits, enforcing contracts, paying taxes and resolving insolvency. It, however, slipped when it came to starting a business, getting an electricity connection, cross-border trade and registering property.

Underlining how reforms had helped India improve its overall ranking, the World Bank said the establishment of debt recovery tribunals reduced non-performing loans by 28% and lowered interest rates on larger loans, suggesting that faster processing of debt recovery cases cut the cost of credit.

India was also among the 10 economies to have improved the most, alongside El Salvador, Malawi, Nigeria and Thailand.

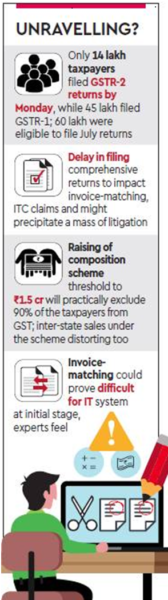

Increasing the fear of an unravelling of the exercise of invoices-matching, which is crucial to realising the presumed merits of the goods and services tax (GST), like reduction of tax evasion and cascades, three-fourths of the 60 lakh eligible taxpayers haven’t completed the formalities of filing.

Increasing the fear of an unravelling of the exercise of invoices-matching, which is crucial to realising the presumed merits of the goods and services tax (GST), like reduction of tax evasion and cascades, three-fourths of the 60 lakh eligible taxpayers haven’t completed the formalities of filing both the inward and outward supplies-based returns for July till a day before the October 31 deadline. This has forced the government to give another window till November-end “to facilitate about 30.81 lakh taxpayers” to file details of inward supplies (GSTR-2). The triplicate comprehensive returns for July, the first month since GST’s launch, were originally required to be filed in the subsequent month itself, but due to the GST Network’s technical glitches and low levels of compliance, the deadlines have been extended multiple times. The schedule for filing these returns for August onwards has not even been announced yet, as this was to follow from the July-cycle learning. While invoice-matching is getting unduly delayed, piling up a huge job for the taxmen, the consequent blockage of input tax credits is bound to hit the working capital for large sections of the industry.

Since the launch of GST, small and medium enterprises have faced cash crunch, while exporters have got the refunds of July and August taxes only recently. Of course, the government has allowed industries with turnover up to Rs 1.5 crore to file the detailed returns on a quarterly basis while assuring them of prompt release of input tax credits claimed via monthly interim returns, but the deferment of invoices-matching would mean large-scale adjustments of the tax and ITC figures later. The government has faced much criticism for the imperfections of the GST it launched (multiple rates, high peak rates, exclusion of real estate and five petro- leum products etc). Also, since the GST was introduced, it has had to make more compromises that besmirched the new tax further. While dozens of items saw rate changes post-July, the GST Council, on October 6, accorded virtual tax waiver for exporters till March 31, 2018, despite exemptions running contrary to the GST’s basic tenet.

Besides, units with up to Rs 1.5 crore turnover were allowed to file quarterly instead of monthly returns, a move that would allow 90% of the non-composition GST registrants to shift to the easier system of filing returns every quarter, but could make prompt invoices-matching difficult. As reported by FE on Monday, the council may allow all taxpayers to move to quarterly mode of filing returns as it meets at Guwahati on November 10. The composition scheme — that allows businesses to pay taxes as a small percentage of turnover annually — is set to be made available to units with turnover up to Rs 1.5 crore, in what could effectively exclude 90% of the taxpayers from being part of the multi-point destination-based tax chain.

GST Network, which is the IT backbone of GST, estimates that about 80 crore invoices would be uploaded on to the system every month. A tax official said that even if 2-3 crore of the invoices don’t match, it will lead to numerous disputes, which would be arduous to resolve. “Besides, tax evasion takes place when transactions are off-book which will never be captured through invoices. The government needs precise and visible enforcement to minimise tax evasion,” the official said. To begin with, GST Council should have implemented matching at the GST level where sale and purchase are matched on the basis of the unique GST registration number of each taxpayer. Invoice matching should ideally have been brought in a few months later after the system stabilised. Now that some taxpayers are allowed to file returns only quarterly, the matching should also be harmonised with it and not be carried out every month.

These steps alone will make the process smoother,” Rahul Renavikar, managing director of Acuris Advisors said. Aditya Singhania, of Taxmann, said: “The matching concept is a much appreciated step for allowing input tax credit which is regulated by the GSTR 1, 2 and 3 mechanism. But with the brilliant concept, the IT platform of GST i.e. www.gst.gov.in should equally work in same wavelength for achieving the objective. Due to certain bugs and frictions, coupled with totally new forms of returns, taxpayers were unable to file the (returns) on time.” While industrialised states like Maharashtra, Gujarat and Karnataka among others had invoice-matching systems prior to GST, although these were not granular-level matching. A Maharashtra tax official, who requested anonymity, said that matching at the level of VAT number –much simpler than invoice-level matching – had enabled identification of 80% mismatches, which enabled the tax department to take action against hawala operations.

However, some tax officials have doubted the efficacy of invoice-matching, saying this wasn’t much of a success in any country with GST-type tax. “The first two month would pose immense challenges on how to deal with invoice mismatches and the provision may eventually have to be done away with,” a revenue department officials told FE on the condition of anonymity. The tax department is also worried that about 40% of taxpayers who filed the returns for July have claimed nil-tax liability. “It is indeed a large number. If enforcement is required, we will carry it out, though not in the nature of search and seizure. We may opt for discreet inquiries and meetings with such groups of taxpayers, to find out the reasons for the trend,” revenue secretary Hasmukh Adhia had told FE earlier.

GST Network (GSTN), the company handling IT infrastructure for the indirect tax regime, has from October 10 started issuing refunds to exporters for Integrated GST (IGST).

Exporters can soon start claiming refunds for GST paid in August and September as GSTN will this week launch an online application for processing of refund, its Chief Executive Officer Prakash Kumar said today.

GST Network (GSTN), the company handling IT infrastructure for the indirect tax regime, has from October 10 started issuing refunds to exporters for Integrated GST (IGST) they paid for the month of July, after matching GSTR-3B and GSTR-1.

For August and September, while the initial return GSTR- 3B has already been filed, the final return GSTR-1 has not yet been filed.

“A separate online app for claiming Integrated GST (IGST) refunds for August and September would be made available on GSTN portal this week,” Kumar told .

GSTN has developed the app wherein exporters can save and upload their sales data which are part of GSTR-1 after filling up export details in Table 6A.

The table will be then extracted separately and after exporters digitally sign it, it would automatically go to the customs department.

The customs department will then validate the information provided in the table with the shipping bill data and also the taxes paid in GSTR-3B. The refund amount would be either credited to exporter’s bank account through ECS or a cheque would be issued.

As per data, 55.87 lakh GSTR-3B returns were filed for July, 51.37 lakh for August and over 42 lakh for September. Preliminary returns GSTR-3B for a month is filed on the 20th day of the next month after paying due taxes.

Thereafter, final returns in form GSTR-1, 2, 3 are filed by businesses giving invoice wise details of sales. The final return filing for August and September has not started yet.

Over July-August, an estimated Rs 67,000 crore has accumulated as the Integrated GST (IGST), of which only about Rs 5,000-10,000 crore will be due as refunds to exporters.

The Goods and Services Tax (GST), the amalgamation of over a dozen indirect taxes like excise duty and VAT, does not provide for any exemption, and so exporters are required to first pay Integrated-GST (IGST) on manufactured goods and claim refunds after exporting them. This had put severe liquidity crunch, particularly on aggregators or merchant exporters.

To ease their problems, the GST Council earlier this month decided a package for them that includes extending the Advance Authorisation / Export Promotion Capital Goods (EPCG) / 100 per cent EOU (Export Oriented Unit) schemes to sourcing inputs from abroad as well as domestic suppliers till March 31, thus not requiring to pay IGST.

The government is aiming to clear pending GST refunds of exporters by November-end. The first cheque after processing of July refunds was issued on October 10.

Country’s growth is expected to accelerate in the medium-term as temporary disruptions due to demonetization and GST.

India must prioritise implementation of public banking sector structural reforms, enhance the efficiency of labour and product markets, and modernise agriculture sector to accelerate its growth, the IMF said Friday.

The country’s growth is expected to accelerate in the medium-term as temporary disruptions due to demonetisation and the Goods and Services Tax (GST) fade, the International Monetary Fund said in its Asia and Pacific Regional Economic Outlook Update.

The economic growth slowed in India in recent quarters due to the temporary disruptions from the currency exchange initiative demonetisation that took place in November 2016, and the recent rollout of the GST, it said.

The GST is a landmark tax reform that should help unify the domestic market and encourage businesses to move from the informal to the formal sector, the IMF noted.

Inflation has been low compared with the mid-point target in recent months, driven by lower food prices, allowing the central bank to cut its policy rate in August, it added.

“Growth in 2017 was revised downward to reflect the recent slowdown, but is expected to accelerate in the medium term as these temporary disruptions fade,” it said.

In India, growth was revised down to 6.7 per cent in FY2017 and to 7.4 per cent in FY2018.

“Growth will be underpinned by private consumption, which has benefited from low food and energy prices, as well as civil service allowance increases,” IMF said.

Headline inflation is projected to stay close to the midpoint of the target band (4 per cent 2 per cent) in FY2017, while moving to the upper half of the target band in the medium term as food prices recover, it said.

The current account deficit should remain modest, financed by robust foreign direct investment inflows, it noted.

According to the outlook, in India, priorities should be strengthening public banks loss-absorbing buffers, implementing further public banking sector structural reforms, and enhancing public banks debt recovery mechanisms.

“Reform efforts should aim at tackling supply bottlenecks, enhancing the efficiency of labour and product markets, and modernising the agricultural sector,” the IMF said, adding that labour market reforms should be a priority to facilitate greater and higher-quality job creation.

More than 90 days after the roll-out of the goods and services tax (GST), lenders are gravitating to sanctioning working capital loans, especially to micro and small units, against documents used in the new tax regime.

They are no longer looking at just sales of the units concerned to decide on loan sanctions.

Banks are looking at input credit in deciding how much working capital loans they should advance.

The country’s largest lender, State Bank of India, and Union Bank of India, also a public sector bank, have started giving loans, especially to micro, small and medium enterprises (MSMEs) after assessing their input tax credit claims.

A public sector bank executive said the large number of small and medium enterprises (SMEs) had been included under the ambit of formal trade with the introduction of the GST.

SMEs are facing a working capital crunch because in the absence of proper financial returns, they are unable to access bank credit.

In the traditional route, banks make working capital assessments based on sales, as indicated in the balance sheet.

Besides this, entrepreneurs are facing a credit crunch because in the GST regime SMEs are entitled to input tax credit, and it is stretching their operating cycle.

A Punjab National Bank (PNB) official said the banking system is shifting to looking at the history of transactions such as GST credit-based decisions about credit, especially for SMEs.

SBI Chief General Manager (SME) V Ramling said using GST claims by banks would give SMEs the time to manage their working capital requirements till the time they got input tax credit. It will also help stabilise SMEs to run their operations without any hurdles.

SBI said the loan would be sanctioned outside Assessed Bank Finance (ABF) at 20 per cent of the existing fund-based working capital limit or 80 per cent of input tax claim due on purchases, whichever is lower.

Units and companies seeking a loan under the product need to give a certificate from their chartered accountant, confirming the input credit claims.