Infosys Nilekani gave GST Network presentation to Council.

Council ask Infosys to improve GST Network by July.

Filing to be mandatory for taxpayers over Rs 5cr of annual

turnover

Decides to extend deadline for filing of GSTR9 & GSTR9C

for FY18-19 till June 30, 2020,

GST Council to continue with 3B till September & defer the new return system.

Council defers the proposal on taxability of economic surplus of brand owners of alcohol for human consumption,

Reassures states towards payment of compensation dues,

Where Cancellation have been cancelled till March 14,

application for cancellation of revocation can be filed till March 31, 2020.

GSTR-1 to be made compulsory only for making B2B supplies,

exports & amendments

B2C & non-filers of GSTR-3B to be exempted from filing

GSTR-1

Before 10th for turnover greater than Rs 1.5 cr

Before 13th for turnover lesser than Rs 1.5 cr

GSTR-2A to be generated on 14th of every month

Council approves “Know your Supplier” Scheme

Major Reliefs:

Interest for delay in GST payment will now be charged on next cash liability under Section 50, to be applicable from July 2017

GST on mobile phones and specified parts was increased from 12% to 18%. This decision was taken to avoid difficulties due to the inverted duty structure.

All types of matches have been rationalised to a single GST rate of 12%. Till now, the handmade ones were taxed at 5% and the rest was taxed at 18%.

GST on Maintenance, Repair and Overhaul (MRO) service in respect to aircraft was reduced from 18% to 5% with full ITC.

All these rate changes will come into effect from 01 April 2020.

A new scheme called ‘Know your Supplier’ has been introduced so that the taxpayers are informed about the basic details of the suppliers with whom they transact or propose to conduct business.

On a day when the Economic Survey acknowledged the fact that both GST system is complex, taxpayers found it impossible to file their returns.

The Central Board of Indirect Taxes and Customs (CBIC) late on Friday night extended the due date for furnishing GST Annual Return and Reconciliation Statement (GSTR-9 / 9A and GSTR-9C) for FY 2017-18 in a staggered manner. The last date to file the Returns was January 31, 2020.

This came after thousands of taxpayers took to social media complaining about the GST portal not working. “Considering the difficulties being faced by taxpayers in filing GSTR-9 and GSTR-9C for FY 2017-18 it has been decided to extend the due dates in a staggered manner for different groups of States to 3rd, 5th and 7th February 2020 as under,” CBIC said in a Tweet.

Accordingly under Group 1, the states of Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Puducherry, Telangana, Andhra Pradesh, Other Territory has been placed and they will need to file their returns by 3rd February 2020.

Group 2 includes Jammu and Kashmir, Himachal Pradesh, Punjab, Chandigarh, Uttarakhand, Haryana, Delhi, Rajasthan and Gujarat that have to file by 5th February 2020.

Lastly group 3 includes the states of Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Andaman & Nicobar Islands, Jharkhand, Odisha, Chhattisgarh, Dadra and Nagar Haveli and Daman and Diu, Lakshadweep, Madhya Pradesh, and Uttar Pradesh, which now have to file by 7th February 2020.

On a day when the Economic Survey acknowledged the fact that both GST system is complex, taxpayers found it impossible to file their returns. By evening of January 31, #gstnfailed was the top trend on Twitter. At 10 30 pm CBIC tweeted the extension dates, but early reports suggest the portal is still not working.

The ministry further said it has also taken a note of difficulties and concerns expressed by the taxpayers regarding filing of GSTR-3B and other returns.

The Finance Ministry has announced the three due dates for filing GSTR-3B for different categories of Taxpayers.

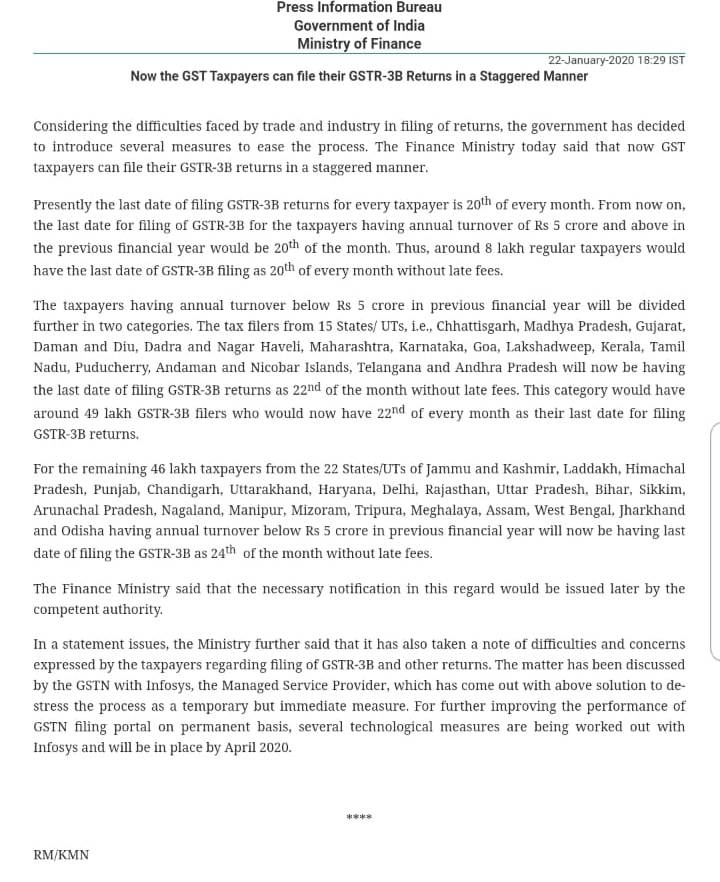

The Finance Ministry today said that now GST taxpayers can file their GSTR-3B returns in a staggered manner. Considering the difficulties faced by trade and industry in the filing of returns, the government has decided to introduce several measures to ease the process.

Presently the last date of filing GSTR-3B returns for every taxpayer is 20th of every month. From now on, the last date for filing of GSTR-3B for the taxpayers having annual turnover of Rs 5 crore and above in the previous financial year would be 20th of the month. Thus, around 8 lakh regular taxpayers would have the last date of GSTR-3B filing as 20th of every month without late fees.

The taxpayers having annual turnover below Rs 5 crore in the previous financial year will be divided further into two categories. The tax filers from 15 States/ UTs, i.e., Chhattisgarh, Madhya Pradesh, Gujarat, Daman and Diu, Dadra and Nagar Haveli, Maharashtra, Karnataka, Goa, Lakshadweep, Kerala, Tamil Nadu, Puducherry, Andaman and Nicobar Islands, Telangana and Andhra Pradesh will now be having the last date of filing GSTR-3B returns as 22nd of the month without late fees. This category would have around 49 lakh GSTR-3B filers who would now have 22nd of every month as their last date for filing GSTR-3B returns.

For the remaining 46 lakh taxpayers from the 22 States/UTs of Jammu and Kashmir, Laddakh, Himachal Pradesh, Punjab, Chandigarh, Uttarakhand, Haryana, Delhi, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand and Odisha having annual turnover below Rs 5 crore in previous financial year will now be having last date of filing the GSTR-3B as 24th of the month without late fees.

The Finance Ministry said that the necessary notification in this regard would be issued later by the competent authority.

In a statement issued, the Ministry further said that it has also taken note of difficulties and concerns expressed by the taxpayers regarding the filing of GSTR-3B and other returns. The matter has been discussed by the GSTN with Infosys, the Managed Service Provider, which has come out with the above solution to de-stress the process as a temporary but immediate measure. For further improving the performance of GSTN filing portal on a permanent basis, several technological measures are being worked out with Infosys and will be in place by April 2020.

Changes under the GST applicable for New Year 2020

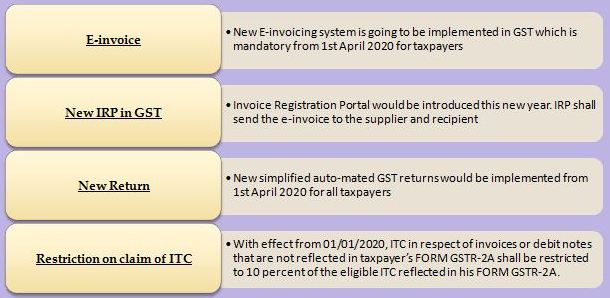

E-invoice : New E-invoicing system is going to be implemented in GST which is mandatory from 1st April 2020 for taxpayers having an annual turnover exceeding Rs. 100 crore and then gradually to all B2B suppliers in the future. A mechanism for the continuous upload of revenue invoices on a real-time basis. This is the most remarkable change coming in Indian Book Keeping.

New IRP in GST: Invoice Registration Portal would be introduced this new year. IRP shall make an e-invoice of the invoices uploaded by the supplier. IRP shall send the e-invoice to the supplier and recipient. IRP shall send e-invoices data to GSTN portal

New Return: New simplified auto-mated GST returns would be implemented from 1st April 2020 for all taxpayers. This new returns system will increase compliance and reduce tax evasion to a larger extent.

Annexure 1 and Annexure 2: Anx-1 of Outward Supplies and Anx-2 of Inward Supplies will be the future base for filing of all GST Returns, thus these 2 reports will be the key for future reports of GST which will replace GSTR 1 and GSTR-2A.

Restriction on claim of ITC: With effect from 01/01/2020, ITC in respect of invoices or debit notes that are not reflected in taxpayer’s FORM GSTR-2A shall be restricted to 10 percent of the eligible ITC reflected in his FORM GSTR-2A. Earlier the restriction was 20%. A major change in ITC availment.

E-way Bill and GSTR-1: From 11th January, 2020 non-filing of GSTR-1 for two consecutive periods would block generation of E-way Bill. Thus, regular filing of GSTR-1 and GSTR-3B in year 2020 should go hand in hand.

Waiver of late fees for Non-filing of GSTR-1: If the taxpayer has failed to file GSTR-1 from July 2017 to November 2019, then the taxpayers can file such returns till 10 January, 2020 and the late fees for the same has been waived of. This will also affect GSTR-2A of the recipient to claim ITC.

GST Audit and Annual Return: The due date for filing GST Annual Return and Audit Report for F.Y. 2017-18 has been further extended to 31st January, 2020.The due date for filing GST Annual Return and Audit Report for F.Y 2018-19 has been extended to 31st March, 2020. For F.Y 2019-20 new format may be brought in because of inherent limitations in current forms.

DIN notices and E-scrutiny: Due to decline in collection of revenue from GST, large scale e-scrutiny and e-assessment notices with DIN for the returns from July 2017 may be taken up. It would be done in order to check significant deviations in returns.

GSTN Network is proposed to be reengineered for more taxpayer-centric services like reminder of return filing, status of refund, ITC matches and mismatches, etc.

Late fee to be waived on GSTR-1 if filed by Jan 10, 2020

The Goods and Services Tax (GST) council has decided to waive off late fees for all taxpayers who have filed GSTR 1, if all refunds are filed by 10 January 2020.

In the 38th meeting of the GST Council on December 18, authorities had also waived of a late fee to be given all taxpayers in respect of all pending Form GSTR-1 from July 2017 to November 2019, if the same is filed by January 10th, 2020.

According to CBIC, the late fee waiver will be applicable only till 10 January 2020, beyond which a late fee of at least Rs 50 per day will be charged for non-filing of GSTR-1.

The late fine can also go up to a maximum of Rs 10,000 per statement as per existing provisions. The CBIC has also said that the government has planned to take a number of steps if the pending GSTR-1 is not filed by the 10th of next month, which may include steps such as blocking of the E-way bill, etc.

GSTR-1 is a monthly return that summarizes all sales (outward supplies) of a taxpayer. The due dates for GSTR-1 are based on turnover. Businesses with sales of up to Rs. 1.5 crore will file quarterly returns. Other taxpayers with sales above Rs. 1.5 crores have to file monthly return.

Businesses take advantage of facilities provided under existing system to generate fake invoices that cause loss to the Government

Tax authority given the right to restrict the use of balance in electronic credit ledger

In an effort to curb the menace of fake invoices and tax evasion, the Finance Ministry has notified a new norm of limiting the input tax credit to 10 per cent in case of GST details mismatch.

Experts feel that this will force businesses to restrict themselves to matched details and ignore the mismatched ones and thus incur losses, which could go into crores for big companies, due to complexities involved.

The change in the norm, the second in three months, has been initiated following a decision by the GST Council. Earlier, in October, the government limited ITC in case of details not uploaded by suppliers to 20 per cent which has now been halved. According to a new notification to be effective from January 1, ITC to be availed by a registered person in respect of invoices or debit notes, the details of which have not been uploaded by the suppliers, shall not exceed 10 per cent of the eligible credit available in respect of invoices or debit notes the details of which have been uploaded by the suppliers.

Two return forms

Businesses take advantage of facilities provided under existing system to generate fake invoices that cause loss to the Government. The existing system prescribes assessees to file two return forms — GSTR 1 (outward sales with tax liability) and GSTR 3B (summary returns with final tax payment). Since both are not auto linked, this could result in showing higher liability, claiming higher input tax credit and paying less tax in cash.

In other words, irrespective of the credit being visible in GSTR 2A (auto generated return for purchases), the service recipient used to claim credit without any restriction subject to having the invoice copy and satisfying other conditions laid down under the law. There is feeling that one of the reasons for availing higher input tax credit on the basis of fake invoices was the mismatch between the two — GSTR 1 and GSTR 3B.

This was affecting the government’s revenue. This has forced it to limit the ITC in case of details not matched and encourages the companies to monitor whether the suppliers are uploading their returns on a regular basis. However, experts feel that such a mechanism will lead to compliance cost for companies. Also, the companies might not prefer to go behind suppliers to see whether they have filed returns or not. Hence, they would focus only on matched details and incur loss on account of others.

Electronic Credit Ledger

The government has introduced additional conditions for use of amount available in Electronic Credit Ledger. It has given the right to the tax authority to restrict the use of balance in electronic credit ledger by recording the reasons to believe in writing. The key reasons for restricting credit are: invoice issued by registered person not in existence and recipient is not in procession of goods/services /invoice on which credit is claimed. Post restriction, the tax authority, upon being satisfied that conditions for disallowing debit of electronic credit ledger as above, no longer exist, can allow such credit in the electronic credit ledger.

Controlling tax evasion

According to Harpreet Singh, Partner at KPMG, one hopes that automatic blocking of credit is resorted to only where fraudulent intention is proved beyond doubt and the same is not used on a regular basis, as casual resort to the said provision may lead to harsh consequences for many innocent defaulters.

Rajat Mohan, Senior Partner with AMRG, said GST frauds are on the rise and so is the fiscal deficit which is forcing the government to introduce new methods to control tax evasion and take punitive action against the accused.

Here are some of the major announcements in GST council meet dt : 18th Dec 2019

The Council decided that input tax credit will now be restricted to 10 percent as against 20 percent earlier if invoices not uploaded.

Deadline for GSTR 9 and GSTR 9C return filing for 2017-18 extended to January 31, 2020 from December 31, 2019 .

Penalty for non-filing of GSTR-1 from July 2017 relaxed . Late fee waived for all assessees failed to file GSTR 1 , if they file it by 10th January 2019.

GST Council exempts long term lease on industrial plots to facilitate setting up of industrial parks.

Land lease GST rates to be applicable from January 1, 2020.

Uniform rate of 18% for woven and non-woven bags.

Uniform rate of 28% for lotteries.

At present, lotteries run by state governments attract 12% GST while those authorised by them and sold outside the state are taxed at 28%.

E-way bill for those who haven’t filed GSTR-1 for 2 tax periods shall be blocked.

Standard procedure for officers to be issued in respect of action to be taken in cases of non-filing of GSTR-3B.

Due date of filing GST returns for Nov 19 to be extended in certain north eastern states.

Grievance redressal committees will be constituted to address the general problems of the taxpayers at zonal and state level with both CGST and SGST officers and including certain representatives.

Infosys Nilekani gave GST Network presentation to Council.

Infosys Nilekani gave GST Network presentation to Council.