The disruptive impact of demonetisation announced last year is a temporary phenomenon and the scrapping of the high-value currency would bring “permanent and substantial benefits”, according to the International Monetary Fund (IMF).

The disruptive impact of demonetisation announced last year is a temporary phenomenon and the scrapping of the high-value currency would bring “permanent and substantial benefits”, according to the International Monetary Fund (IMF).

In an interview to CNBC TV18, IMF Economic Counsellor and Director of Research Maurice Obstfeld said that although demonetisation, as well as implementation of the Goods and Services tax (GST) caused short-term disruptions, both measures would bring long-term benefits.

“The costs of demonetisation are largely temporary and we see permanent and substantial benefits accruing from the move,” Obstfeld said.

Demonetisation caused long queues outside banks.

“Both demonetisation and the GST introduction will bring long-term benefits, though these caused short-term disruption,” he said.

The IMF Chief Economist described GST as a “work in progress” to which the Indian economy is “gradually adjusting”.

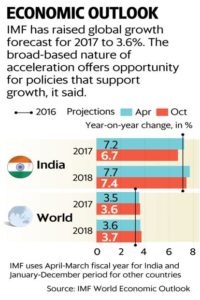

With businesses going into a “destocking” mode on inventories in anticipation of the GST rollout from July 1, sluggish manufacturing growth, among other factors, pulled down growth in the Indian economy during the first quarter of this fiscal to 5.7 percent, clocking the lowest GDP growth rate under the Narendra Modi dispensation.

Breaking a five-quarter slump, however, a rise in manufacturing sector output pushed the growth rate higher to 6.3 percent during the second quarter (July-September) of 2017-18.

Obstfeld also listed some of the reforms being undertaken by the Indian government that have impressed the multilateral agencies.

“The government has taken important first steps like bringing in the Insolvency and Bankruptcy Code, which helped India improve its position substantially in the World Bank’s ‘Ease of Doing Business’ rankings,” he said.

He also mentioned the recent recapitalisation plan for state-run banks announced by the government and the Asset Quality Review of commercial banks earlier ordered by the Reserve Bank of India (RBI).

In a report released in Washington on Thursday, the IMF cautioned that the high volume of NPAs and the slow pace of mending corporate balance sheets are holding back investment and growth in India even though structural reforms have helped the nation record stronger growth.

The IMF’s Financial System Stability Assessment (FSSA) for India said that overall “India’s key banks appear resilient, but the system is subject to considerable vulnerabilities”.

“The financial sector is facing considerable challenges, and economic growth has recently slowed down,” the report said.

“High non-performing assets and slow deleveraging and repair of corporate balance sheets are testing the resilience of the banking system, and holding back investment and growth.”

“Stress tests show that… a group of public sector banks are highly vulnerable to further declines in asset quality and higher provisioning needs,” it added.

Source: FirstPost