The first day of the much-hyped Rajasthan Resurgent Summit concluded with 295 proposals worth Rs 3.3 lakh crore. These proposals, however, were received over the past year and barely left much scope for industry heavyweights and the Union government to announce any new big-ticket projects.

The first day of the much-hyped Rajasthan Resurgent Summit concluded with 295 proposals worth Rs 3.3 lakh crore. These proposals, however, were received over the past year and barely left much scope for industry heavyweights and the Union government to announce any new big-ticket projects.

“These proposals are just the tip of the iceberg. A lot of work has to be done,” Chief Minister Vasundhara Raje said in her inaugural speech. “This investment will create 2.5 lakh jobs,” she added.

In the past year, Rajasthan has undertaken a raft of economic and industry reforms to create an investment-friendly image. Her government was left with a huge debt, including Rs 70,000 crore of debt from the power sector, by the previous Congress government.

THE PROPOSALS

• Rs 11,000 cr investments announced by Kumar Mangalam Birla

• Rs 10,000 cr pledged by Gautam Adani

• Rs 6,500 cr worth investments by Anil Ambani

• Rs 10,000 cr worth projects to be undertaken by chemical & fertiliser ministry

• 24 model railway stations to be developed in the state

Lauding Raje’s role, Union Finance Minister Arun Jaitley said, after leading the state in reforms, the chief minister should now lead the state in ease of doing business. The government should provide land for business. “The India of 2015 is not the India of 1971. For that matter, it is also not the India of 1991. The aspirational constituency, which supports growth wants India to reform at a much faster speed,” he said. “Everything should be corruption free. Taxation should be reasonable and the policy should not be so aggressive that it deters investors, ” he added.

Among the investments made public on Thursday, the biggest perhaps came from Kumar Mangalam Birla, chairman of the Aditya Birla Group. Birla promised investment of nearly Rs 11,000 crore, including Rs 7,000 crore for setting up two new cement plants and Rs 3,000 crore for establishing a 500 MW solar power plant in the state. Gautam Adani, head of the Adani Group, also promised to invest an additional sum of Rs 10,000 crore over four years for the expansion of thermal power plants and generation of solar power in the state.

However, then there was a word of caution by Hero Motocorp chairman Pawan Munjal. Though he lauded the government’s role in making the state investor friendly, he requested the chief minister to ensure speedy clearance of projects.

“We need speedy clearances for setting up our industries,” Munjal said, disclosing that his company is setting up a state-of-the-art Research and Development Centre on the outskirts of Jaipur.

Uday Kotak, chief executive officer of Kotak Mahindra Bank, found special mention from Raje for the bank’s financial services. Kotak said his bank’s lending ratio is more than the deposit in the state.

For instance, against a deposit of Rs 100, his bank lends Rs 250. “We plan to double our lending from Rs 5,000 crore to Rs 10,000 crore in the next three years… this will help small, medium-scale industries and farmers in the state,” Kotak said.

From the central government, the biggest announcements came from chemicals and fertiliser minister Ananth Kumar, who promised Rs 10,000-crore of projects. This includes setting up a National Institute of Pharmaceutical Education and Research in Jhalawar district in two years, upgrade of the Central Institute of Plastic Engineering and Technology in Jaipur, and setting up a plastics park and a medical devices park, a first in the country. Railways minister Suresh Prabhu said they were going to set up 24 modern railway stations in the state.

Tourism was another key sector, which received special attention from the Central government, as well as the summit’s international partners including Singapore, Japan, Italy and Australia. Singapore Home Affairs Minister K Shanmugam said Singapore Airlines has decided to operate a direct flight from Singapore. “The airlines knew that it might not be earning profit in one or two years, but it is a long-term partnership,” he said.

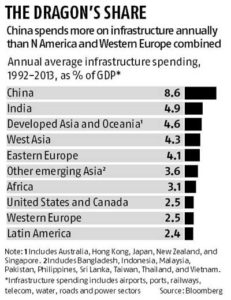

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run.

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run. In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.

In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.