The Circular from Ministry of Corporate Affairs extends one more month time, for Annual Filings of MGT -7 , Annual Return & AOC-4, Audited Financial Statements, without additional fees, to Tamil Nadu & Pondicherry, which were affected by floods.

The extract of the circular issued today, i.e., 30 December, 2015 is as below:

In continuation of the ministry’s circular 15/2015 dated 30.11.2015, keeping in view the requests received from various stakeholders stating that due to heavy rains and floods in the State of Tamil Nadu and Union Territory of Puducherry, the normal life/work was affected, it has been decided to relax the additional fees payable for the State of Tamil Nadu and UT of Puducherry on e-forms AOC-4, AOC (CFS) AOC-4 XBRL and e- Form MGT-7 up to 30.01.2016, wherever additional fee is applicable.

The last date of filing forms AOC-4 (XBRL, non-XBRL & CFS) and MGT-7 till 30th Dec 2015, without additional fees, has ended.

The Ministry of Corporate Affairs, Government of India has earlier vide its General Circular No.15/2015 dated 31/11/2015, extended the last date for filing the Annual Returns by 30 days and relaxed the additional fees for the forms filed till December 31, 2015. This has ended now.

Immaterial frauds will now form a part of the annual report, and the requirement to report immaterial frauds to the central government has been done away with, it noted.

Statutory auditors will now have to mandatorily report to the Centre all corporate frauds amounting to Rs. 1 crore or above.

By specifying a threshold of Rs. 1 crore, the Corporate Affairs Ministry (MCA) has now done away with the requirement to report immaterial frauds to the Centre.

The Ministry has also now spelt out the procedure for fraud reporting to the Centre. First, the auditor has to inform the Board or audit committee and seek their views within 45 days.

On receipt of audit committee’s views, the auditor would have to within 15 days send his report to the Centre.

For frauds involving amounts lower than Rs. 1 crore, statutory auditors now need to report this matter only to the audit committee of the company, the Ministry has said amending rules for this purpose.

The reporting to the audit committee would have to be done not later than two days of his knowledge of the fraud.

Prior to this Ministry move, the company law required statutory auditors to report to the Centre all frauds by the company or against it.

Vishal Seth. Managing Director and National Leader IFRS and Financial Reporting Advisory, Protiviti India, Indian arm of a global consulting firm, said this threshold of Rs. 1 crore was a “fairly reasonable” given the magnitude of transactions in India.

“This is a big change in India. There was a need for a threshold and the Ministry has now specified it,” Seth told Business Line here.

Meanwhile, KPMG in India said in a note that the Ministry’s move on fraud reporting would increase responsibility of auditors. The amended rule prescribing the timelines for fraud reporting indicates the effort the Ministry is putting to increase the efficiency and timelines of such reporting, KPMG has said.

Related party transactions

The Ministry has now amended rules to specify that an audit committee would be empowered to provide “omnibus approvals” for related party transactions (RPTs) so long as certain conditions are met.

The conditions specified by the Ministry are largely similar to the Listing Regulations.

Yogesh Sharma, Partner, Grant Thornton India LLP, said this will certainly assist in ease of doing business without compromising the intent of the law.

Moreover, omnibus approval process was already included in the SEBI listing guidelines and hence this change will align the two requirements, he added.

For RPTs, the Company Law enacted in 2013 required every individual transaction to be approved by the Audit Committee. This made the approval process inefficient and delayed the decision making. For instance, each repeat transaction also required a separate approval.

The company law amendments in 2015 enabled “omnibus approval” for RPTs on annual basis that meet specified conditions prescribed in rules. The Ministry has now specified the conditions under which such omnibus approvals could be provided.

Reacting to the Ministry’s move, CA Institute President Manoj Fadnis welcomed the threshold specified by the Ministry. “This will bring certainty to the auditors as to the frauds that are to be reported to the central government and those that are to be reported to the audit committee,” he told Business Line .

Greater vigil

The auditor must first report the fraud to the company’s audit panel

The audit panel will have to give its views in 45 days

Within 15 days of that, the auditor will have to send his report to the Centre

Frauds amounting to less that Rs. 1 crore will need to be reported only to the company’s audit panel

Analysis of integrated e-Form INC-29 for Company Incorporation and Ease of doing business

With the introduction of the INC-29, the Ministry of Corporate Affairs (MCA) has begun to make good on its promise to improve India’s ranking on the World Bank’s Ease of Starting a Business Index to within the top 50 from the current 158.

The INC-29 form for company registration, combines the application for DIN allotment, name reservation, incorporation and even PAN & TAN, while making the process faster and simpler. As the entire incorporation process is in a single form, correct filing could mean approval in 48 hours. Compared to the old process, this helps in formation of company saving a lot of time, if properly implemented.

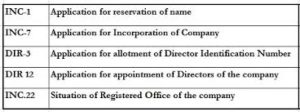

Purpose of the eForm – eForm INC-29 deals with the single application for reservation of name, incorporation of a new company and/or application for allotment of DIN. This eForm is accompanied by supporting documents including details of Directors & subscribers, MoA and AoA etc. Once the eForm is processed and found complete, company would be incorporated with Corporate Identification Number (CIN) and the Certificate of Incorporation would be issued. Also DINs gets issued to the proposed Directors, who do not have a valid DIN. Maximum three Directors are allowed for using this integrated form for allotment of DIN while incorporating a company.

Key Features of e-form INC-29

The integrated e-Form INC-29 is available with effect from 01.05.2015 for One Person Company, Private Company as well as Public Company.

INC-29 does away with filing of multiple applications/forms saving time and payable fees.

It combines the processes relating to:-

Allotment of Director Identification Number (DIN) (up to three Directors),

Incorporation of a company, and

Appointment of first Directors of the company.

3. The new e-Form does away with the need for reserving a name for the company prior to applying for its incorporation.

Declarations are in-built in the e-Form. Separate attachments containing such declarations are not required.

The e-Form is enabled for future integration with e-Biz platform of DIPP for generating applications for PAN, ESIC and EPFO numbers on the platform and therefore provides a single interface for these applications also.

Forms no longer to be filed individually as per the new Form INC 29:

During the past one year, Corporate Affairs Ministry has taken a number of steps, and is further streamlining processes and regulatory framework, to reduce the overall time taken for incorporating a company as a part of ‘ease of doing business’ effort, Finance Ministry has said.

The Government of India proposes to bring down the average number of days required for incorporating a company to one to two days, a move aimed at further improving ‘ease of doing business’ in the country.

During the past one year, Corporate Affairs Ministry has taken a number of steps, and is further streamlining processes and regulatory framework, to reduce the overall time taken for incorporating a company as a part of ‘ease of doing business’ effort, Finance Ministry said in a statement.

As a result of the many steps, the average number of days taken for incorporation of a company has come down significantly from 9.57 days in December, 2014 to 4.51 days in November, 2015.

“It (Ministry of Corporate Affairs) is targeting that the average number of days would be further reduced to one to two days for approval in normal cases,” the statement said.

Giving details of the step, it said the introduction of an Integrated Incorporation Form INC29 and tighter monitoring of Registrar of Companies’ (ROCs’) performance has resulted in faster approvals and lesser number of clarifications being asked from the stakeholders.

The Corporate Affairs Ministry will soon introduce a new version of Form INC29, incorporating suggestions received from the stakeholders, allowing up to five directors to be appointed and greater flexibility in proposing a name for a company, it said.

“This will allow an even more wider use of this integrated Form, which is already gaining popularity,” the statement added.

Further, the rules with regard to reserving and approving of names for companies are also being simplified, and a centralised new process will be introduced soon for strictly time bound approval of names for companies.

Private equity investors, who have stayed away from investing in online retail companies, have instead quietly reaped a windfall by backing logistics companies providing back-end support in the e-commerce rush.

In the latest deal, Peepul Capital recorded an over six-fold return on its investment in Ecom Express according to people aware of the transaction. Earlier this year Multiples Alternate Asset Management also made a partial exit from Delhivery, when the company raised fresh capital led by Tiger Global Management.

“These kinds of returns are only possible if there is multiple re-rating of both a company and a sector, which is not very common,” said Prakash Nene, MD at Multiples, who declined to comment on specifics of the deal.

The PE firm made a partial exit after Tiger Global led a round of about Rs 542 crore in the Delhi-based firm in May.

Peepul Capital is estimated to have earned Rs 500 crore on an initial investment of Rs 80 crore in Ecom Express. The firm made an exit when the logistics firm raised fresh capital in a round led by Warburg Pincus according to two people privy to the details.

The returns have been even higher for early seed and angel investors in these two companies, which handle delivery for top online retailers like Flipkart, Amazon and Snapdeal.

According to filings with the ministry of corporate affairs (MCA), seed fund Oliphans Capital bought shares in Ecom Express at around Rs 70 per share in 2013. The fund is estimated to have sold some of these shares to Warburg Pincus during the investment round in June this year. Regulatory filings indicate Warburg — through its unit Eaglebay Investments — paid Rs 2,276 per share of Ecom Express; this would imply that Oliphans netted a return of over 30 times.

“It’s only logical that investment is also about exits,” said Anish Jhaveri, MD at Oliphans, declining to comment on returns made by his firm. “When we invested around $1 million in the company (Ecom Express) there were just four people in front of us who had just quit Blue Dart.”

Ecom Express was founded in 2012 by TA Krishnan, Sanjeev Saxena, K Satyanarayana and Manju Dhawan who had launched the e-tailing business at Blue Dart. The Delhi-based company expects to deliver goods in over 10,000 pin codes covering more than 1,500 towns and cities, across the country in the next few years.

The increasing interest in these companies is driven by the rapid growth in logistic support for online retail. A recent report on the Indian internet sector by brokerage IIFL estimates that the order volume for e-commerce shipments will increase 13x by 2020, with overall volume of e-commerce orders amounting to 2,000 tonnes per day.

Investors are of the view that just as tower companies gained in the telecom boom, the online retail rush will benefit from the back-end support companies.

“There are a lot of enablers which are important from a shadow driving perspective broadly similar to what telecom towers are to telco industry and EPC companies are to infrastructure,” said Sreeni Vudayagiri, investment director at Peepul Capital, a PE firm with $700 million under management which primarily invests in mid-sized consumption and manufacturing businesses.

Punishment for Contravention of Section 73 and Section 76 of Companies Act, 2013 for Acceptance of Deposits by Companies [New Section 76A inserted]

The Companies (Amendment) Act, 2015 has inserted a new Section 76A after Section 76 which introduces penal provisions for contravention of provisions of Section 73 and Section 76 (pertaining to acceptance of deposits by a company) or rules made thereunder, or if a company fails to repay deposits within the time specified.

As per the amended law:

A company, if it fails to repay deposits within the specified time, shall be punishable with a fine which shall not be less than Rs.1 crore but which may extend to Rs. 10 crores, in addition to the payment of the amount of deposit or part thereof and the interest due.

Every officer of the company who is in default shall be punishable with imprisonment which may extend to seven years or with a fine which shall not be less than Rs. 25 lakhs but which may extend to Rs. 2 crore, or with both.

Thus, specific punishment is prescribed for non-compliance to norms governing deposits taking activities.

MCA had changed the structure of Additional Fees to be levied for delay in filing E Forms over the companies while filing their Balance Sheet and Annual Returns with concerned Registrar of Companies through MCA Portal. Such change of Additional Fee Structure encouraged the Corporate to file their returns as early as possible so that they can avoid the heavy additional fees. That has resulted in increase the percentage of filing within the due time.

More than 15 days and up to 30 days (Sections 93, 139 & 157) and up to 30 days in remaining forms.

2 times of normal filing fees

03

More than 30 days and up to 60 days

4 times of normal filing fees

04

More than 60 days and up to 90 days

6 times of normal filing fees

05

More than 90 days and up to 180 days

10 times of normal filing fees

06

More than 180 days and up to 270 days

12 times of normal filing fees

Further Note:

1) The additional fee shall also applicable to revised financial statement or board’s report under sections 130 and 131 of the Act and secretarial audit report filed by the company secretary in practice under section 204 of the Act.

(2) The belated filing of documents /forms (including increasing in nominal capital and delay caused thereon) which were due to be filed whether in Companies Act, 1956 Act or the Companies Act, 2013 Act i.e due for filing prior to notification of these fee rules, the fee applicable at the time of actual filing shall be applicable.

(3) Delay beyond 270 days, the second proviso to sub-section (1) of section 403 of the Act may be referred.