Atmanirbhar economic package: ITR deadline extended to Nov 30, 2020 for FY 2019-20 and tax audit from September 30, 2020 to 31st October 2020.”

The Central Government has extended the all due dates of all Income Tax Returns for the Financial Year 2019-20 amid COVID-19 outbreak.

Due date of all income-tax return for FY 2019-20 will be extended from 31st July, 2020 & 31st October, 2020 to 30th November, 2020 and Tax audit from 30th September, 2020 to 31st October, 2020.

The Finance Minister Nirmala Sitharaman also said that, All pending refunds to charitable trusts and non-corporate businesses & professions including proprietorship, partnership, LLP, and Co-operatives shall be issued immediately.

The Date of assessments getting barred on 30th September, 2020 extended to 31st December, 2020 and those getting barred on 31st March, 2021 will be extended to 30th September, 2021.

The Period of Vivad se Vishwas Scheme for making payment without an additional amount will be extended to 31st December, 2020.

The package works out to roughly 10 per cent of the GDP, making it among the most substantial in the world.

Key Highlights of the Special economic and comprehensive package of Rs 20 lakh crores Announced by the Govt. of India, for relief and credit support related to businesses, especially MSMEs to support Indian Economy, Atmanirbhar Bharat and to fight against COVID-19.

GOI Presentation on Rs. 20 Lac Crore Special Package: AtmaNirbhar Bharat (COVID-19)

Hon’ble Prime Minister Shri Narendra Modi yesterday announced a Special economic and comprehensive package of Rs 20 lakh crores, equivalent to 10% of India’s GDP. He gave a clarion call for आत्मनिर्भर भारत अभियान or Self-Reliant India Movement. He also outlined five pillars of Aatmanirbhar Bharat– Economy, Infrastructure, System, Vibrant Demography and Demand.

During the press conference here today, Union Minister of Finance & Corporate Affairs Smt. Nirmala Sitharaman said in her opening remarks that Prime Minister Shri Narendra Modi had laid out a comprehensive vision in his address to the Nation yesterday. She further said that after spending considerable time, the Prime Minister has himself ensured that inputs obtained from widespread consultation form a part of economic package in fight against COVID-19.

“Essentially, the goal is to build a self-reliant India that is why the Economic Package is called Aatma Nirbhar Bharat Abhiyaan. Citing the pillars on which we seek to build Aatma Nirbhar Bharat Abhiyaan, Smt. Sitharaman said our focus would be on land, labour, liquidity and law.

The Finance Minister further said that the Government under the leadership of Prime Minister Shri Narendra Modi has been listening and is a responsive Government, hence it is fitting to recall some reforms which have been undertaken since 2014.

“Soon after Budget 2020 came COVID-19 and within hours of the announcement of Lockdown 1.0, Pradhan Mantri Garib Kalyan Yojna (PMGKY) was announced,” Smt. Sitharaman said. She further said that we are going to build on this package.

“Beginning today, for the next few days, I shall be coming here with the entire team of the Ministry of Finance to detail the Prime Minister’s vision for Aatma Nirbhar Bharat laid out by the Prime Minister yesterday,” Smt Sitharaman said.

Smt. Nirmala Sitharaman today announced measures focused on Getting back to work i.e., enabling employees and employers, businesses, especially Micro Small and Medium Enterprises, to get back to production and workers back to gainful employment. Efforts to strengthen Non-Banking Finance Institutions (NBFCs), Housing Finance Companies (HFCs), Micro Finance Sector and Power Sector were also unfolded. Other than this, the tax relief to business, relief from contractual commitments to contractors in public procurement and compliance relief to real estate sector were also covered.

Over the last five years, the Government has actively taken various measures for the industry and MSME. For the Real Estate sector, the Real Estate (Regulation and Development) Act [RERA] was enacted in 2016 to bring in more transparency into the industry. A special fund for affordable and middle income housing was set up last year to help with the stress in this segment. To help MSMEs with the issue of delayed payment by any Government department or PSUs, Samadhaan Portal was launched in 2017. A Fund of Funds for startups was set up under SIDBI to boost entrepreneurship in the country and various other credit guarantee schemes to help flow of credit to the MSMEs.

Key Highlights of the Special economic and comprehensive package of Rs 20 lakh crores Announced by Govt. of India (COVID-19)

a) Rs 3 lakh crore Emergency Working Capital Facility for Businesses, including MSMEs

To provide relief to the business, additional working capital finance of 20% of the outstanding credit as on 29 February 2020, in the form of a Term Loan at a concessional rate of interest will be provided. This will be available to units with upto Rs 25 crore outstanding and turnover of up to Rs 100 crore whose accounts are standard. The units will not have to provide any guarantee or collateral of their own. The amount will be 100% guaranteed by the Government of India providing a total liquidity of Rs. 3.0 lakh crores to more than 45 lakh MSMEs.

b) Rs 20,000 crore Subordinate Debt for Stressed MSMEs

Provision made for Rs. 20,000 cr subordinate debt for two lakh MSMEs which are NPA or are stressed. Government will support them with Rs. 4,000 Cr. to Credit Guarantee Trust for Micro and Small enterprises (CGTMSE). Banks are expected to provide the subordinate-debt to promoters of such MSMEs equal to 15% of his existing stake in the unit subject to a maximum of Rs 75 lakhs.

c) Rs 50,000 crores equity infusion through MSME Fund of Funds

Govt will set up a Fund of Funds with a corpus of Rs 10,000 crore that will provide equity funding support for MSMEs. The Fund of Funds shall be operated through a Mother and a few Daughter funds. It is expected that with leverage of 1:4 at the level of daughter funds, the Fund of Funds will be able to mobilise equity of about Rs 50,000 crores.

d) New definition of MSME

Definition of MSME will be revised by raising the Investment limit. An additional criteria of turnover also being introduced. The distinction between manufacturing and service sector will also be eliminated.

e) Other Measures for MSME

e-market linkage for MSMEs will be promoted to act as a replacement for trade fairs and exhibitions. MSME receivables from Government and CPSEs will be released in 45 days.

f) No Global tenders for Government tenders of up to Rs 200 crores

General Financial Rules (GFR) of the Government will be amended to disallow global tender enquiries in procurement of Goods and Services of value of less than Rs 200 crores.

g) Employees Provident Fund Support for business and organised workers

The scheme introduced as part of PMGKP under which Government of India contributes 12% of salary each on behalf of both employer and employee to EPF will be extended by another 3 months for salary months of June, July and August 2020. Total benefits accrued is about Rs 2500 crores to 72.22 lakh employees.

h) EPF Contribution to be reduced for Employers and Employees for 3 months

Statutory PF contribution of both employer and employee reduced to 10% each from existing 12% each for all establishments covered by EPFO for next 3 months. This will provide liquidity of about Rs.2250 Crore per month.

i) Rs 30,000 crores Special Liquidity Scheme for NBFC/HFC/MFIs

Government will launch Rs 30,000 crore Special Liquidity Scheme, liquidity being provided by RBI. Investment will be made in primary and secondary market transactions in investment grade debt paper of NBFCs, HFCs and MFIs. This will be 100 percent guaranteed by the Government of India.

j) Rs 45,000 crores Partial credit guarantee Scheme 2.0 for Liabilities of NBFCs/MFIs

Existing Partial Credit Guarantee scheme is being revamped and now will be extended to cover the borrowings of lower rated NBFCs, HFCs and other Micro Finance Institutions (MFIs). Government of India will provide 20 percent first loss sovereign guarantee to Public Sector Banks.

k) Rs 90,000 crore Liquidity Injection for DISCOMs

Power Finance Corporation and Rural Electrification Corporation will infuse liquidity in the DISCOMS to the extent of Rs 90000 crores in two equal instalments. This amount will be used by DISCOMS to pay their dues to Transmission and Generation companies. Further, CPSE GENCOs will give a rebate to DISCOMS on the condition that the same is passed on to the final consumers as a relief towards their fixed charges.

l) Relief to Contractors

All central agencies like Railways, Ministry of Road Transport and Highways and CPWD will give extension of up to 6 months for completion of contractual obligations, including in respect of EPC and concession agreements.

m) Relief to Real Estate Projects

State Governments are being advised to invoke the Force Majeure clause under RERA. The registration and completion date for all registered projects will be extended up to 6 months and may be further extended by another 3 months based on the State’s situation. Various statutory compliances under RERA will also be extended concurrently.

n) Tax Relief to Business

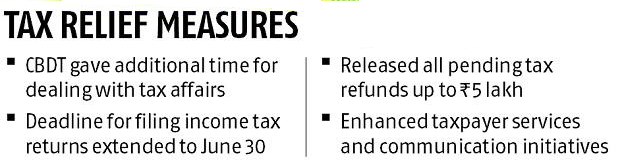

The pending income tax refunds to charitable trusts and non-corporate businesses and professions including proprietorship, partnership and LLPs and cooperatives shall be issued immediately.

o) Tax related measures

Reduction in Rates of ‘Tax Deduction at Source’ and ‘Tax Collected at Source” – The TDS rates for all non-salaried payment to residents, and tax collected at source rate will be reduced by 25 percent of the specified rates for the remaining period of FY 20-21.This will provided liquidity to the tune of Rs 50,000 Crore.

The due date of all Income Tax Returns for Assessment Year 2020-21 will be extended to 30 November, 2020. Similarly, tax audit due date will be extended to 31 October 2020.

The date for making payment without additional amount under the “Vivad Se Vishwas” scheme will be extended to 31 December, 2020.

The reduced TDS and TCS rate will be for specific payments such as payment for a contract, professional fees, interest, rent etc.

In order to provide more funds at the disposal of the taxpayers, the rates of Tax Deduction at Source (TDS) for non-salaried specified payments made to residents and rates of Tax Collection at Source (TCS) for the specified receipts has been be reduced by 25% of the existing rates.

The Finance Minister Nirmala Sitharaman said that, Payment for the contract, professional fees, interest, rent, dividend, commission, brokerage, etc. shall be eligible for this reduced rate of Tax Deduction at Source.

This reduction shall be applicable for the remaining part of the FY 2020-21 i.e. from tomorrow 14th May 2020 to 31st March, 2021.

The Finance Minister also said that, It will help to Rs 50,000 crores liquidity through TDS/TCS rate reduction.

She also said that the income tax department has already cleared Rs 18,000 crore worth of refunds where the quantum due was up to Rs 5 lakh and instructed that all pending refunds to charitable trusts and non-corporate business and professions will be issued immediately.

TDS rate was not deducted on salaries, after considering various eligible deductions such as 80C of the salaried person. This had been done to ensure that the salaried individual did not bear the burden of paying higher taxes at the year end.

Move comes after a group of IRS created panic and tax policy uncertainty.

After rejecting “ill-conceived” suggestions by a group of Indian Revenue Services (IRS) officers, the Central Board of Direct Taxes (CBDT) directed officials not to keep any communication with assessees or issue scrutiny notices to them without the board’s approval.

According to it, any such notice would have an “adverse effect” on the assessees amid the coronavirus (Covid-19) pandemic.

These directives are part of the interim action plan for the first quarter (April-June) prepared by the direct tax board. It highlights certain areas which need immediate attention and preparedness until normalcy returns.

The move comes at a time when the tax department faced widespread criticism on a report prepared by a group of IRS officers. It had created panic and tax policy uncertainty at a time when India is already going through a difficult economic situation.

“Identification and preparedness regarding the issuance of notice under Section 148, which deals with income escaping and return filing in all eligible cases, should be done by June 30. However, these notices are to be issued only after getting fresh communication from the board in this regard,” said the CBDT note.

It added that due to the unprecedented situation arising out of Covid-19-induced social distancing and lockdown this year, a relatively short interim action plan has been issued.

Considering the current situation, we have been putting a slew of tax relief measures to mitigate the impact on business and even on household.

Any such communication may put pressure on the taxpayers and create unnecessary panic. A new system had already been put in place to make officials accountable for their communication with assessees.

However, during the lockdown, even such communication would not go without the board consent, said a CBDT official. Other than keeping no communication with assessees, the tax officials have been asked to centralise cases where searches took place in the financial year 2019-202.

This is because once lockdown is lifted, the officials would work on disposing them on merit.

Moreover, the CBDT asked officials to be prepared for tax demands in cases of international taxation, tax deduction at source and exemption-related charges.

The board wants the department to examine all pending demands, according to permanent account number (PAN) and assessment years.

It also removed demands which are creating duplication and are lying in the system. Besides, officials were asked to reconcile brought-forward cases, especially on TDS, based on the information available on the Traces portal for TDS units. The interim action plan also instructed officials to dispose of all applications concerning granting registration to charitable trusts received upto March 31.

Meanwhile, the direct tax board told its officials to upload manual orders on the systems, especially those under Section 263. It deals with appeals where the principal commissioner or commissioner may call for and examine the record of any proceeding. He or she may consider an order passed by the assessing officer to be erroneous, if it is prejudicial to the interests of the revenue.

Earlier, such registrations/approvals were granted without any specific expiry period unless specifically withdrawn by concerned tax authority. Under the new law introduced by Finance Act 2020 and effective from June 1, 2020, all such registrations/ approvals would now be issued with an expiry period of 5 years.

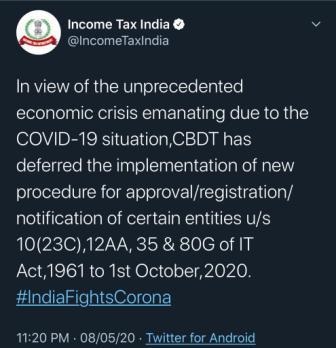

In a relief to religious trusts, educational institutions and other charitable institutions, the income tax department on Friday deferred by 4 months till October 1 the requirement of registration of these entities.

In a relief to religious trusts, educational institutions and other charitable institutions, the income tax department on Friday deferred by 4 months till October 1 the requirement of registration of these entities.

“In view of the unprecedented humanitarian and economic crisis, the CBDT has decided that the implementation of new procedure for approval/ registration/notification of certain entities shall be deferred to 1st October, 2020,” an official statement said.

Finance

Act 2020 prescribed substantial changes in law pertaining to

registration/approval of trusts and charitable institutions, whose

income are exempt under section 10(23C), Section 11 or for the purpose

of Section 80-G of the Act for tax deductible donations.

Earlier,

such registrations/approvals were granted without any specific expiry

period unless specifically withdrawn by concerned tax authority.

Under

the new law introduced by Finance Act 2020 and effective from June 1,

2020, all such registrations/ approvals would now be issued with an

expiry period of 5 years.

Further, all trusts/charitable institutions already having approval or registration were also supposed to file applications for renewal of there registration/approval within 3 months of new law coming into force, i.e. August 31, 2020.

Nangia

Andersen Consulting Shailesh Kumar said “in light of COVID-19 outbreak

and consequent lockdown, giving relief to the taxpayers, this timeline

has been deferred by 4 months. Thus, new law which was supposed to come

in effect from 01 June 2020 would now come in effect from 01st October

2020.

“All

existing trusts/ charitable institutions would now need to file

applications for renewal of their registrations/ approvals by December

31, 2020 instead of earlier August 31, 2020,” he added.

The

statement said various representations were received to the finance

ministry expressing concerns over the implementation of new procedure

from June 1, 2020 due to outbreak of coronavirus (COVID-19) and

consequent lockdown and there have been a number of requests to defer

the applicability of new procedure.

“This is a welcome move and provides expected relief in light of genuine hardships created by COVID-19. The entities benefited by this circular would be religious trusts, hospitals, educational institutions or other public charitable institutions created for welfare of public and allows exemption from income tax on account of their activities and charitable purpose,” Kumar added.

Consulting

firm AKM Global Tax Partner Amit Maheshwari said, “This is a welcome

clarification as in the absence of this extension, it was extremely

difficult to comply with these procedures. Several representations had

been made on this matter and this is indeed a welcome move.”

• An employee can change the option of tax structure at the time of filing the ITR • TDS will get adjusted accordingly

The Central Board of Direct Tax (CBDT) recently came out with a circular, offering clarifications for tax-paying employees on how they can migrate to the new concessional tax regime, which was announced in this year’s Union Budget.

The lower income tax rates under the new regime came to effect from April 1, 2020. However, there were many concerns raised on how employees can choose to opt between the old and regime.

In an April 13 release, the CBDT said employees, who do not have any income from a business, can opt for the new concessional tax slabs or the old regime by intimating the deductor (employer) through a declaration form.

The declaration will also help employers determine whether to deduct TDS as per the old regime or the new concessional rates.

Employees have an option to choose between the new tax regime and the old one. Experts have already said that each employee/taxpayer may opt for any of the two, based on investments.

Coming to the new slabs under the concessional tax regime, those earning Rs 2.5 lakh will have to pay no tax while people earning Rs 2.5-5 lakh will have to pay 5 per cent tax.

Individuals in the income bracket of Rs 7.5-10 lakh will pay 15 per cent tax. People earning over Rs 10-12.5 lakh will be taxed at 20 per cent and those earning Rs 12.5-15 lakh will pay 25 per cent taxes. Finally, people earning above Rs 15 lakh will pay 30 per cent tax under the concessional tax regime.

To sum up the clarifications: 1) Employees, who do not have any income from a business, can choose to inform their employer through a declaration if they want to opt for the new tax regime for deducting tax at source on TDS from salaries.

However, employees who do not submit any declaration to the employer will continue to be charged under the old regime as earlier.

2) The IT department also clarified that an employee can change the tax structure at the time of filing income tax and that the amount of TDS will be adjusted accordingly.

“The deductor shall compute his total income, and make TDS thereon in accordance with the provisions of section IISBAC of the Act. If such intimation is not made by the employee, the employer shall make TDS without considering the provision of section 11SBAC of the Act,” the CBDT notification said.

3) Another important clarification by the tax department was related to TDS. Once employees make their intention clear to opt for the concessional rates, it will remain the same for TDS purpose for the year without any scope of modification.

“It is also clarified that the intimation so made to the deductor (employee) shall be only for the purposes of TDS during the previous year and cannot be modified during that year,” it said.

“However, the intimation would not amount to exercising an option in terms of sub-section (5) of section 115BAC of the Act and the person shall be required to do so along with the return to be furnished under sub-section (1) of section 139 of the Act for that previous year. Thus, option at the time of filing of return of income under sub-section (1) of Section 139 of the Act could be different from the intimation made by such employee to the employer for that previous year.”

Infosys Nilekani gave GST Network presentation to Council.

Council ask Infosys to improve GST Network by July.

Filing to be mandatory for taxpayers over Rs 5cr of annual

turnover

Decides to extend deadline for filing of GSTR9 & GSTR9C

for FY18-19 till June 30, 2020,

GST Council to continue with 3B till September & defer the new return system.

Council defers the proposal on taxability of economic surplus of brand owners of alcohol for human consumption,

Reassures states towards payment of compensation dues,

Where Cancellation have been cancelled till March 14,

application for cancellation of revocation can be filed till March 31, 2020.

GSTR-1 to be made compulsory only for making B2B supplies,

exports & amendments

B2C & non-filers of GSTR-3B to be exempted from filing

GSTR-1

Before 10th for turnover greater than Rs 1.5 cr

Before 13th for turnover lesser than Rs 1.5 cr

GSTR-2A to be generated on 14th of every month

Council approves “Know your Supplier” Scheme

Major Reliefs:

Interest for delay in GST payment will now be charged on next cash liability under Section 50, to be applicable from July 2017

GST on mobile phones and specified parts was increased from 12% to 18%. This decision was taken to avoid difficulties due to the inverted duty structure.

All types of matches have been rationalised to a single GST rate of 12%. Till now, the handmade ones were taxed at 5% and the rest was taxed at 18%.

GST on Maintenance, Repair and Overhaul (MRO) service in respect to aircraft was reduced from 18% to 5% with full ITC.

All these rate changes will come into effect from 01 April 2020.

A new scheme called ‘Know your Supplier’ has been introduced so that the taxpayers are informed about the basic details of the suppliers with whom they transact or propose to conduct business.