According to IMF’s Regional Economic Outlook, India’s growth slowed in recent quarters due to the temporary disruptions from the currency exchange initiative– demonetisation and GST.

The IMF has suggested a three- pronged approach for structural reform in India that includes addressing the corporate and banking sector weaknesses, continued fiscal consolidation through revenue measure, and improving the efficiency of labour and product markets.

Deputy Director Asia Pacific Department of IMF, Kenneth Kang, said the favorable outlook for Asia was an important opportunity for India to push forward with difficult reforms.

“As such, there should be three policy priorities in the area of structural reforms,” Kang, Deputy Director Asia pacific Department IMF told reporters at a news conference here.

“First priority is to address the corporate and banking sector weaknesses, by accelerating the resolution of non- performing loans, rebuilding the capital buffers for the public sector banks, and enhancing banks’ debt recovery mechanisms,” he said.Secondly, Kang said, India should continue with the fiscal consolidation through revenue measures, as well as further reductions in subsidies.

“And lastly, it’s to maintain the strong momentum for structural reforms in addressing the infrastructure gaps, improving the efficiency of labour and product markets as well as furthering agricultural reforms,” said Kang.

Responding to a question on labour market reforms, Kang suggested reforming the market regulations in order to create a more favorable environment for investment and employment.

“There is a need to reduce the number of labour laws which currently number around 250 across the central and the state level,” said Kang.He said India should also focus on closing the gender gap which may help a great deal in boosting the employment opportunities for women in India.

“Improvements in infrastructure can be one important way to facilitate the entry of women into the labour force. But in addition, there is a need to strengthening the implementation of specific gender regulations, as well as to invest more in gender-specific training and education,” Kang said.

According to IMF’s Regional Economic Outlook, India’s growth slowed in recent quarters due to the temporary disruptions from the currency exchange initiative– demonetisation– that took place in November 2016, and the recent roll-out of the Goods and Services Tax (GST).

The report, however, went on to say that the growth in 2017 was revised downward to reflect the recent slowdown, but is expected to accelerate in the medium term as these temporary disruptions fade.

Insolvency and Bankruptcy Board of India has published draft rules dealing with insolvency resolution process of individuals and firms on its website . The existing insolvency and bankruptcy code, at present, applies only to corporate defaulters

The government on Tuesday expanded the scope of the new insolvency rules to bring individual businesses under its purview.

On Tuesday, the Insolvency and Bankruptcy Board of India (IBBI) published the draft rules dealing with insolvency resolution process of individuals and firms on its website (www.ibbi.gov.in) ; public comments can be submitted till 31 October.

Once notified, even individual businesses such as proprietorships will come under the bankruptcy regime. This will enable an orderly bankruptcy resolution within the purview of a transparent rules-based regime. The existing insolvency and bankruptcy code, at present, applies only to corporate defaulters.

“These rules shall apply to matters relating to the insolvency resolution process for individuals and firms under Part III of the code,” said the draft rules issued by IBBI.

Part III of the Insolvency and Bankruptcy Code, 2016, deals with insolvency and bankruptcy of individuals and partnership firms.

According to a statement issued by IBBI on Tuesday, the draft rules and regulations have been submitted by a working group which was formed to recommend the strategy and approach for implementation of the provisions of the Insolvency and Bankruptcy Code, 2016, dealing with insolvency and bankruptcy in respect of guarantors to corporate debtors, i.e., personal guarantors, and individuals having businesses.

“So far, the rules were only in respect of the Corporate Insolvency Resolution Process (CIRP) and the rules concerning individuals and partnership firms were yet to come,” said Satwinder Singh, partner at Vaish Associates, a law firm. “The jurisdiction for corporate, companies, limited liability partnership (LLP) lies before the National Company Law Tribunal (NCLT) and with the Debt Recovery Tribunal (DRT) for individuals and firms. The provisions relating to insolvency and bankruptcy of individuals and firms had not been notified earlier, so now the IBBI has come out with the draft rules.”

Harsh Pais, partner at law firm Trilegal, said, “It is a positive step towards consolidating the bankruptcy regime for individuals, for whom there was no systematic approach previously. For companies, at least there was recourse to the Companies Act, whereas for individuals there were only some archaic laws from the early 1900s, which were hardly relied upon in practice.”

Most of the small and medium enterprises (SMEs) take the legal form of either partnership or proprietorship firms. Though the loans are smaller in value, SME borrowers far outnumber companies, resulting in their borrowings exerting a significant influence in the financial sector’s stability.

Bankruptcy resolution is high on the agenda of the central government, which is keen to improve the ease of doing business in India and attract more private investments from domestic and overseas sources. An efficient exit route from failed projects is an essential factor that lenders consider before participating in projects.

SEBI has tightened the noose on listed companies not adhering to norms with regard to minimum public shareholding (MPS). Those that are non-compliant will have to pay a fine of Rs.5,000 a day. In addition, the entire promoter holding, except for compliance to MPS, will be frozen by depositories, and the promoter group and directors of the particular company will not be allowed to hold any position in other companies.

According to MPS norms, any listed company must have at least 25 per cent as public share holders while the remaining 75 per cent can be held by promoters. Government-promoted companies were given time till August 2018 to comply with these norms. Newly listed companies are given a three-year window to comply.

De-listing

Further, if the non-compliance continues for over one year the amount of fine per day will double to Rs.10,000 and such companies may even face compulsory de-listing of their shares from stock exchanges. Stock exchanges have been asked to share all the details of non-compliant companies on their website.

“Mandating penalties for non-compliance of MPS norms will surely act as a deterrent for the violators,” said Anjali Aggarwal, Partner & Head, Capital Market & Stock Exchange Services at Corporate Professionals, a law firm.

“But for any listed company, there may be many corporate actions such as forfeiture of partly paid shares/ buybacks/ takeover offers, etc, wherein promoter holding crossing the threshold of 75 per cent is beyond that company’s control, as it can’t be ascertained as to how many shareholders may tender their holding. A distinction needs to be carved for routine defaulters and for lapses that may happen because of any such corporate actions.”

In the past, SEBI has taken action against non-compliant firms but the penalty was not specified in the rule book.

In 2013, SEBI had first cracked the whip on 105 companies, including Adani Ports, BGR Energy Systems, Tata Teleservices and Videocon, for not complying with the MPS norms by freezing voting rights and corporate benefits of promoters, the promoter group and directors of these companies, until they complied.

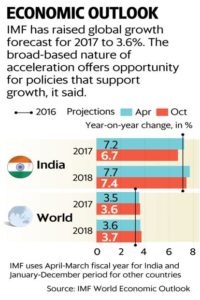

IMF expects the Indian economy to recover sharply in 2018 to grow at 7.4%, though 30 basis points lower than its earlier estimate in April.

The International Monetary Fund (IMF) on Tuesday pared its growth forecast for the Indian economy by half a percentage point to 6.7% for 2017, blaming the lingering disruptions caused by demonetisation of high value currencies last year and the roll out of the Goods and Services Tax (GST).

However, IMF said the structural reforms undertaken by the Prime Minister Narendra Modi-led government would trigger a recovery—above 8% in the medium term.

In its latest World Economic Outlook, IMF said the global economy is going through a cyclical upswing that began midway through 2016. It raised the global growth estimate marginally for 2017 to 3.6% while flagging downside risks. The upward revisions in its growth forecasts including for the euro area, Japan, China, emerging Europe, and Russia more than offset downward revisions for the United States, the United Kingdom, and India.

“In India, growth momentum slowed, reflecting the lingering impact of the authorities’ currency exchange initiative as well as uncertainty related to the midyear introduction of the countrywide Goods and Services Tax,” it said in the WEO.

However, IMF expects the Indian economy to recover sharply in 2018 to grow at 7.4%, though 30 basis points lower than its earlier estimate in April.

One basis point is one-hundredth of a percentage point.

In its South Asia Economic Focus (Fall 2017) released on Monday, the World Bank reduced India’s GDP growth forecast to 7% for 2017-18 from 7.2% estimated earlier, blaming disruptions caused by demonetisation and GST implementation, while maintaining at the same time that the Indian economy would claw back to grow at 7.4% by 2019-20.

Both the Asian Development Bank as well as the Organisation for Economic Cooperation and Development (OECD) have also cut their growth projections for India to 7% and 6.7%, respectively, for fiscal 2017-18.

IMF said a gradual recovery in India’s growth trajectory is a result of implementation of important structural reforms. GST, “which promises the unification of India’s vast domestic market, is among several key structural reforms under implementation that are expected to help push growth above 8% in the medium term,” it added.

The multilateral lending agency said India needs to focus on simplifying and easing labour market regulations and land acquisition procedures which are long-standing requirements for improving the business climate. It also called for briding the gender gap in accessing social services, finance and education to accelerate growth in developing countries like India.

IMF said given faster-than-expected declines in inflation rates in many larger economies, including India, “the projected level of monetary policy interest rates for the group is somewhat lower than in the April 2017 WEO.”

In its monetary policy review last week, the Reserve Bank of India (RBI) kept its policy rates unchanged and marginally raised its inflation forecast for rest of the year.

Highlighting the growing income inequality within and among emerging market economies, IMF said a country’s growth rate does not always foretell matching gains in income for the majority of the population. “In China and India, for example, where real per capita GDP grew by 9.6% and 4.9% a year, respectively, in 1993–2007, the median household income is estimated to have grown less—by 7.3% a year in China and only 1.5% a year in India,” it said.

GST Council has considered the implementation experience of the last 3 months and gave relief to small traders, says Arun jaitley.

More than three months after the Goods and Services (GST) was introduced, the GST Council made a number of big changes today, to give some relief to small and medium businesses (SMEs) on filing and payment of taxes. The panel also eased rules for exporters and cut tax rates on some items. Those businesses with annual turnover of up to Rs 1.5 crore and which constitute 90 percent of the taxpayer base but pay only 5-6 percent of overall tax, have been permitted to file quarterly income returns. “GST Council has considered the implementation experience of the last 3 months and gave relief to small traders… Compliance burden of medium and small taxpayers in GST has been reduced,” Finance Minister Arun Jaitley said. The SMEs had earlier complained of tedious compliance burden under the new regime. Below is the full text of the recommends made by GST today:

The GST Council, in its 22nd Meeting which was held today in the national capital under Chairmanship of the Union Minister of Finance and Corporate Affairs, Shri Arun Jaitley has recommended the following facilitative changes to ease the burden of compliance on small and medium businesses:

Composition Scheme

1. The composition scheme shall be made available to taxpayers having annual aggregate turnover of up to Rs. 1 crore as compared to the current turnover threshold of Rs. 75 lacs. This threshold of turnover for special category States, except Jammu & Kashmir and Uttarakhand, shall be increased to Rs. 75 lacs from Rs. 50 lacs. The turnover threshold for Jammu & Kashmir and Uttarakhand shall be Rs. 1 crore. The facility of availing composition under the increased threshold shall be available to both migrated and new taxpayers up to 31.03.2018. The option once exercised shall become operational from the first day of the month immediately succeeding the month in which the option to avail the composition scheme is exercised. New entrants to this scheme shall have to file the return in FORM GSTR-4 only for that portion of the quarter from when the scheme becomes operational and shall file returns as a normal taxpayer for the preceding tax period. The increase in the turnover threshold will make it possible for greater number of taxpayers to avail the benefit of easier compliance under the composition scheme and is expected to greatly benefit the MSME sector.

2. Persons who are otherwise eligible for composition scheme but are providing any exempt service (such as extending deposits to banks for which interest is being received) were being considered ineligible for the said scheme. It has been decided that such persons who are otherwise eligible for availing the composition scheme and are providing any exempt service, shall be eligible for the composition scheme.

3. A Group of Ministers (GoM) shall be constituted to examine measures to make the composition scheme more attractive.

Relief for Small and Medium Enterprises

4. Presently, anyone making inter-state taxable supplies, except inter-State job worker, is compulsorily required to register, irrespective of turnover. It has now been decided to exempt those service providers whose annual aggregate turnover is less than Rs. 20 lacs (Rs. 10 lacs in special category states except J & K) from obtaining registration even if they are making inter-State taxable supplies of services. This measure is expected to significantly reduce the compliance cost of small service providers.

5. To facilitate the ease of payment and return filing for small and medium businesses with annual aggregate turnover up to Rs. 1.5 crores, it has been decided that such taxpayers shall be required to file quarterly returns in FORM GSTR-1,2 & 3 and pay taxes only on a quarterly basis, starting from the Third Quarter of this Financial Year i.e. October-December, 2017. The registered buyers from such small taxpayers would be eligible to avail ITC on a monthly basis. The due dates for filing the quarterly returns for such taxpayers shall be announced in due course. Meanwhile, all taxpayers will be required to file FORM GSTR-3B on a monthly basis till December, 2017. All taxpayers are also required to file FORM GSTR-1, 2 & 3 for the months of July, August and September, 2017. Due dates for filing the returns for the month of July, 2017 have already been announced. The due dates for the months of August and September, 2017 will be announced in due course.

6. The reverse charge mechanism under sub-section (4) of section 9 of the CGST Act, 2017 and under sub-section (4) of section 5 of the IGST Act, 2017 shall be suspended till 31.03.2018 and will be reviewed by a committee of experts. This will benefit small businesses and substantially reduce compliance costs.

7. The requirement to pay GST on advances received is also proving to be burdensome for small dealers and manufacturers. In order to mitigate their inconvenience on this account, it has been decided that taxpayers having annual aggregate turnover up to Rs. 1.5 crores shall not be required to pay GST at the time of receipt of advances on account of supply of goods. The GST on such supplies shall be payable only when the supply of goods is made.

8. It has come to light that Goods Transport Agencies (GTAs) are not willing to provide services to unregistered persons. In order to remove the hardship being faced by small unregistered businesses on this account, the services provided by a GTA to an unregistered person shall be exempted from GST.

Other Facilitation Measures

9. After assessing the readiness of the trade, industry and Government departments, it has been decided that registration and operationalization of TDS/TCS provisions shall be postponed till 31.03.2018.

10. The e-way bill system shall be introduced in a staggered manner with effect from 01.01.2018 and shall be rolled out nationwide with effect from 01.04.2018. This is in order to give trade and industry more time to acclimatize itself with the GST regime.

11. The last date for filing the return in FORM GSTR-4 by a taxpayer under composition scheme for the quarter July-September, 2017 shall be extended to 15.11.2017. Also, the last date for filing the return in FORM GSTR-6 by an input service distributor for the months of July, August and September, 2017 shall be extended to 15.11.2017.

12. Invoice Rules are being modified to provide relief to certain classes of registered persons.

Rates have dipped to a third to 6 per cent from 9-18 per cent about 6-9 months ago.

Interest rates that money lenders charged borrowers hardly budged for decades irrespective of policy decisions. But even that is collapsing faster than what it is in the formal banking system, thanks to the implementation of Goods and Services Tax.

Borrowing in the informal market is no more lucrative.

Lenders who fund small traders and merchants have lowered their rates to just a third of what they were charging, but still the demand is not showing up.

Rates have dipped to a third to 6 per cent from 9-18 per cent about 6-9 months ago, said two dealers aware of the market dynamics.

“Those businessmen have now limited options to run operations in cash especially after GST implementation and demonetisation,” said a textile business owner, who did not want to be identified.

“From a local politician to an industrialist or local trader whoever has additional unaccounted cash are normally the lenders in this informal loan market.”

A huge army of businessmen borrowed in an informal market from money lenders to avoid getting trapped by the banking system and the tax department. This was known as ‘Kachha Credit’ among practitioners.

With the implementation of GST which produces a chain of transactions till it reaches the ultimate consumer, merchants have little scope to escape accounting for their trades.

So, instead of funding their purchases through informal credit at high rates which was beneficial since it allowed escaping the tax net, they are choosing to fund businesses through formal credit. To keep businesses running, money lenders have lowered rates.

Since the tax department is keeping close watch on businesses, all traders preferred anonymity. This market is known as a plat form for lending and borrowing unaccounted or untaxed money without any collateral. Traders now shy away from availing such credit amid cash squeeze triggered by reform measures like GST and demonetisation. Sometimes, people take highly leveraged positions borrowing such money, which a bank would have declined.

A garment trader who may be eligible to borrow say, Rs 10 lakh in the absence of creditworthy balance sheet, can take a loan up to Rs 50 lakh due to personal knowledge of businesses, dealers said. The practice is prevalent in the garment industry.

Mumbai’s Bhiwandi, a business centre, used to be the hotbed of it. It has died down after the Central Value Added Tax, a central government tax levy introduced by Vajpayee led NDA, was introduced.

MCA had taken another bold initiative in Government Process Re-engineering (GPR) and launched Simplified proforma for Incorporating Company Electronically (SPICe) e-Form.

The Ministry of Corporate Affairs plans to simplify the existing processes for setting up a company, according to a public notice.

In this regard, the ministry — which is implementing the Companies Act — has sought views from the stakeholders.

The government has already centralised name reservation and incorporation services. There were more than 11.34 lakh active companies at the end of August.

Now, comments have been sought for “further simplification of processes aimed at further easing the starting of a business,” the ministry said in a public notice.

Registration of new companies is being done by way of the integrated SPICe form.

The procedures for obtaining DIN (Director Identification Number) by the proposed directors, name reservation, incorporation as well as allotment of PAN and TAN have been integrated — a move that brings down the time taken for starting a new business under the companies law.

According to the notice, DIN allotment or name reservation services can also be done independently by stakeholders “who wish to proceed with incorporation in a piecemeal manner.

Stakeholders can submit their comments to the ministry by November 5.

SPICe (Simplified Proforma for Incorporating a Company Electronically) is aimed at providing speedy incorporation related services.