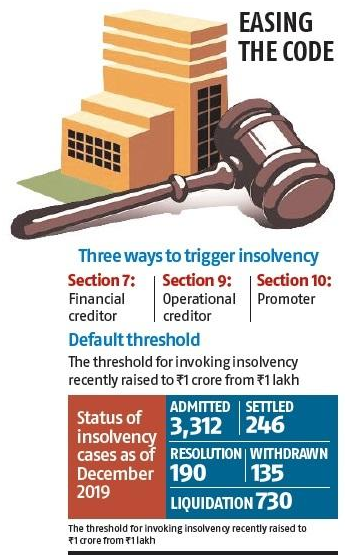

As per existing norms, if a payment default exceeds 90 days then the lender concerned has to refer the account for resolution under IBC or any other mechanism permitted by the Reserve Bank of India (RBI). The lender does not have the option to restructure the loan.

The government has decided to suspend insolvency and bankruptcy proceedings for at least six months owing to challenges businesses are facing due to the Covid-19 pandemic.

A new Section is likely to be added to the Insolvency and Bankruptcy Code (IBC).

It will suspend Sections 7, 9, and 10, which are used to trigger insolvency proceedings for six months or a period not exceeding one year from the date they commence, the official said.

A new Section is likely to be added to the Insolvency and Bankruptcy Code (IBC).

It will suspend Sections 7, 9, and 10, which are used to trigger insolvency proceedings for six months or a period not exceeding one year from the date they commence, the official said.

Section 7 of the Code enables

financial creditors to start insolvency proceedings against a company while

Section 9 gives operational creditors these powers.

Under Section 10, the promoter of the company can trigger insolvency proceedings against his or her own concern.

All the three Sections will cease to be effective for six months or further.

The provision is likely to require a change in the Act, according to experts.

“This is a positive step for companies.

But for companies, which were otherwise already in stress and could have found resolution under the IBC, their resolution may also be delayed due to this suspension,” said Anshul Jain, partner, PwC India.

Jain also said it needed to be seen if this move would have a positive impact on privately negotiated transactions on mergers and acquisitions.

In March, Union Finance Minister Nirmala Sitharaman had indicated the government would consider suspending the IBC for a few months if the Covid situation persisted and caused stress to businesses.

Already, the default threshold for stressed companies facing insolvency has been increased from Rs 1 lakh to Rs 1 crore.

In March, Union Finance Minister Nirmala Sitharaman had indicated the government would consider suspending the IBC for a few months if the Covid situation persisted and caused stress to businesses. Already, the default threshold for stressed companies facing insolvency has been increased from Rs 1 lakh to Rs 1 crore.

The Ministry of Corporate Affairs has introduced the “Companies Fresh Start Scheme, 2020” and revised the “LLP Settlement Scheme, 2020” which is already in vogue to provide a first of its kind opportunity to both companies and LLPs to make good any filing related defaults, irrespective of the duration of default, and make a fresh start as a fully compliant entity.

The Fresh Start scheme and modified LLP Settlement Scheme provide relief to law abiding companies and the Limited Liability Partnerships (LLPs) amid COVID-19 pandemic.

One Time Opportunity

The USP of both the schemes is a one-time waiver of additional filing fees for delayed filings by the companies or LLPs with the Registrar of Companies during the currency of the Schemes, i.e. during the period starting from 1st April 2020 and ending on 30th September 2020.

Fee Payable for CFSS

Only normal fees for filing of documents in the MCA-21 registry will be payable in such case during the currency or CFSS-2020. There will not be any additional fee for any documents.

Every defaulting company shall be required to pay normal fees as prescribed under the Companies (Registration Offices and FCC) Rules, 2014 on the date of filing of each belated document and no additional fee shall be payable.

Dormant Company

The scheme gives an opportunity to inactive companies to get their companies declared as ‘dormant company’ under Section 455 of the Act by filing a simple application at a normal fee.

Details of CFSS 2020

The scheme shall come into force on the 01.04.2020 and shall remain in force till 30.09.2020

“Defaulting company” means company defined under the Companies Act, 2013, and which has made default in filing of any or the documents, statement, returns, etc including annual statutory documents on the MCA-21 registry

“Immunity certificate”‘ means the certificate referred to in subparagraph (viii) of paragraph 6 of the Scheme;

“Inactive Company” means a company as defined in Explanation (i) to sub-section (l) of section 455(1) of the Companies Act, 2013;

Applicability of CFSS 2020

Any ‘defaulting company’ is permitted to file belated documents which were due for filing on any given date in accordance with the provisions of this Scheme.

Immunity from the launch of prosecution or proceedings for imposing penalty shall be provided only to the extent such prosecution or the proceedings for imposing penalty under the Act pertain to any delay associated with the filings of belated documents.

The Ministry received much representation from the stakeholders to provide a one-time opportunity to file all the pending documents including the annual filing of the company without charging higher additional fees on any delay. The Scheme provides the above opportunity to the inactive company to convert into a dormant company under section 455 of Companies Act, 2013 by filing form MSC-1 with nominal fees & help the inactive companies to remain on ROCs register with minimum compliance requirements.

The defaulting company shall be required to file the belated documents including annual filing by paying nominal fees (without including Additional Fees) as per Companies (Registration Offices and Feel Rules, 2014) as prescribed under the Companies Act, on the date of filing of each belated document.

Both the Schemes also contain a provision for giving immunity from penal proceedings, including against imposition of penalties for late submissions and also provide additional time for filing appeals before the concerned Regional Directors against the imposition of penalties, if already imposed. However, the immunity is only against delayed filings in MCA 21 and not against any substantive violation of the law.

Application for issue of immunity under the CFSS

An application for seeking immunity in respect of belated documents can be filed under the Scheme in the Form CFSS-2020, after closure of the Scheme and after the document(s) are taken on file, or on record or approved by the Designated authority as the case may be but not after the expiry of six months from the date of closure of the Scheme. There is no fee payable on this Form.

Provided also that no immunity shall provide in case any court has ordered conviction in any matter, or an order imposing penalty has been passed by an adjudicating authority under the Act and no appeal has been preferred against such orders of the court or of the adjudicating authority.

Immunity certificate under CFSS-2020

Based on the declaration made in the Form CFS-S-2020, an immunity certificate in respect of documents filed under this Scheme shall be issued by the designated authority.

Effect of immunity

After granting the immunity, the ROC office shall withdraw the prosecution(s) and the proceedings of adjudication of penalties under section 454 of the Act, if any, in respect of defaults against which immunity has been so granted and shall be deemed to have been completed without any further action.

Any other consequential proceedings, including any proceedings involving interests of any shareholder or any other person of the company for its directors or key managerial personnel, would not be covered by such Immunity. If the company appeals against any order of prosecution for penalty passed by the competent court or adjudicating authority, then the company first needs to withdraw its application of appeal and furnish the proof of withdrawal to avail immunity in this CFSS 2020 scheme.

Scheme not to apply

This scheme shall not apply

to companies against which action for final notice for striking off the name u/s 248 of the Act (previously section 560 of Companies Act, 1956 has already been initiated by the ROC.

where any application has already been filed by the companies for action of striking off the name of the company from the register of companies;

to companies which have amalgamated under a scheme of arrangement or compromise under the Act;

where applications have already been filed for obtaining Dormant Status under section 455 of the Act before this Scheme;

to vanishing companies;

Where any increase in Authorized Capital is involved (Form SH7);

also Charge related documents (CHG-I, CHG-A. CHG-8 and CHG-9).

The defaulting inactive companies while filing documents under CFSS-2020 can simultaneously apply for the following actions :

Apply to get themselves declared as Dormant Company under section 455 of the Companies Act, 2013 by filing e-form MSC-I at a normal fee on said form; or

Apply for striking off the name of the company by filing e-Form STK-2 by paying the fee payable on form STK-2.

The finance minister heads the Economic Task Force that was set up by the Prime Minister.

Finance minister Nirmala Sitharaman announced a slew of measures for extension of statutory and regulatory compliances in view of the corona virus pandemic spreading its wings and impacting the economy.

Allaying fears that there is no economic emergency in the country, FM said that the Economic Task Force will soon announce an economic relief package to deal with the impact of the corona virus pandemic on the economy.

These are largely in the area of ease of doing business, by providing reliefs in extension of due dates for compliances and reliefs from late fee and penalties, in view of the lock downs announced in several states and districts.

Income Tax

The last date for filing income tax returns for Financial Year 2018-19, extended from 31st March, 2020 to 30th June, 2020.

Aadhaar-PAN linking date extended from 31st March, 2020 to 30th June, 2020.

Vivad se Vishwas scheme – no additional 10% amount, if payment made by June 30, 2020.

Due dates for issue of notice, intimation, notification, approval order, sanction order, filing of appeal, furnishing of return, statements, applications, reports, any other documents and time limit for completion of proceedings by the authority and any compliance by the taxpayer including investment in saving instruments or investments for roll over benefit of capital gains under Income Tax Act, Wealth Tax Act, Prohibition of Benami Property Transaction Act, Black Money Act, STT law, CTT Law, Equalization Levy law, Vivad Se Vishwas law where the time limit is expiring between 20th March 2020 to 29th June 2020 extended to 30th June 2020.

For delayed payments of advanced tax, self-assessment tax, regular tax, TDS, TCS, equalization levy, STT, CTT made between 20th March 2020 and 30th June 2020, reduced interest rate at 9% instead of 12 %/18 % per annum ( i.e. 0.75% per month instead of 1/1.5 percent per month) will be charged for this period. No late fee/penalty shall be charged for delay relating to this period.

Necessary legal circulars and legislative amendments for giving effect to the aforesaid relief shall be issued in due course.

GST/Indirect Tax

Last date for filing GSTR-3B in March, April and May 2020 extended till the last week of 30th June, 2020 for those having aggregate annual turnover less than Rs. 5 Crore. No interest, late fee, and penalty to be charged.

For any delayed payment made between 20th March 2020 and 30th June 2020 reduced rate of interest @9 % per annum ( current interest rate is 18 % per annum) will be charged. No late fee and penalty to be charged, if complied before till 30th June 2020.

Date for opting for composition scheme is extended till the last week of June, 2020. Further, the last date for making payments for the quarter ending 31st March, 2020 and filing of return for 2019-20 by the composition dealers will be extended till the last week of June, 2020.

Date for filing GST annual returns of FY 18-19, which is due on 31st March, 2020 is extended till the last week of June 2020.

Due date for issue of notice, notification, approval order, sanction order, filing of appeal, furnishing of return, statements, applications, reports, any other documents, time limit for any compliance under the GST laws where the time limit is expiring between 20th March 2020 to 29th June 2020 extended to 30th June 2020.

Necessary legal circulars and legislative amendments to give effect to the aforesaid GST relief shall follow with the approval of GST Council.

Payment date under Sabka Vishwas Scheme extended to 30th June, 2020. No interest for this period shall be charged if paid by 30th June, 2020.

Customs

Custom clearance will operate 24X7 till June 30, 2020.

Due date for issue of notice, notification, approval order, sanction order, filing of appeal, furnishing applications, reports, any other documents etc., time limit for any compliance under the Customs Act and other allied Laws where the time limit is expiring between 20th March 2020 to 29th June 2020 shall be extended to 30th June 2020.

Financial Services

Relaxations for 3 months

Debit cardholders to withdraw cash for free from any other banks’ ATM for 3 months

Waiver of minimum balance fee

Reduced bank charges for digital trade transactions for all trade finance consumers

Corporate Affairs

No additional fees shall be charged for late filing during a moratorium period from 01st April to 30th September 2020, in respect of any document, return, statement etc., required to be filed in the MCA-21 Registry, irrespective of its due date, which will not only reduce the compliance burden, including financial burden of companies/ LLPs at large, but also enable long-standing non-compliant companies/ LLPs to make a ‘fresh start’;

The mandatory requirement of holding meetings of the Board of the companies within prescribed interval provided in the Companies Act (120 days), 2013, shall be extended by a period of 60 days till next two quarters i.e., till 30th September;

Applicability of Companies (Auditor’s Report) Order, 2020 shall be made applicable from the financial year 2020-2021 instead of from 2019-2020 notified earlier. This will significantly ease the burden on companies & their auditors for the year 2019-20.

As per Schedule 4 to the Companies Act, 2013, Independent Directors are required to hold at least one meeting without the attendance of Non-independent directors and members of management. For the year 2019-20, if the IDs of a company have not been able to hold even one meeting, the same shall not be viewed as a violation.

Requirement to create a Deposit reserve of 20% of deposits maturing during the financial year 2020-21 before 30th April 2020 shall be allowed to be complied with till 30th June 2020.

Requirement to invest 15% of debentures maturing during a particular year in specified instruments before 30th April 2020, may be done so before 30th June 2020.

Newly incorporated companies are required to submit commencement of Business certificate within 6 months of incorporation. This is now extended to 12 months.

Non-compliance of minimum residency in India for a period of at least 182 days by at least one director of every company, under Section 149 of the Companies Act, shall not be treated as a violation.

Due to the emerging financial distress faced by most companies on account of the large-scale economic distress caused by COVID 19, it has been decided to raise the threshold of default under section 4 of the IBC 2016 to Rs 1 crore (from the existing threshold of Rs 1 lakh). This will by and large prevent triggering of insolvency proceedings against MSMEs. If the current situation continues beyond 30th of April 2020, we may consider suspending section 7, 9 and 10 of the IBC 2016 for a period of 6 months so as to stop companies at large from being forced into insolvency proceedings in such force majeure causes of default.

Detailed notifications/circulars in this regard shall be issued by the Ministry of Corporate Affairs separately.

Department of Commerce

Extension of timelines for various compliance and procedures will be given. Detailed notifications will be issued by Ministry of Commerce.

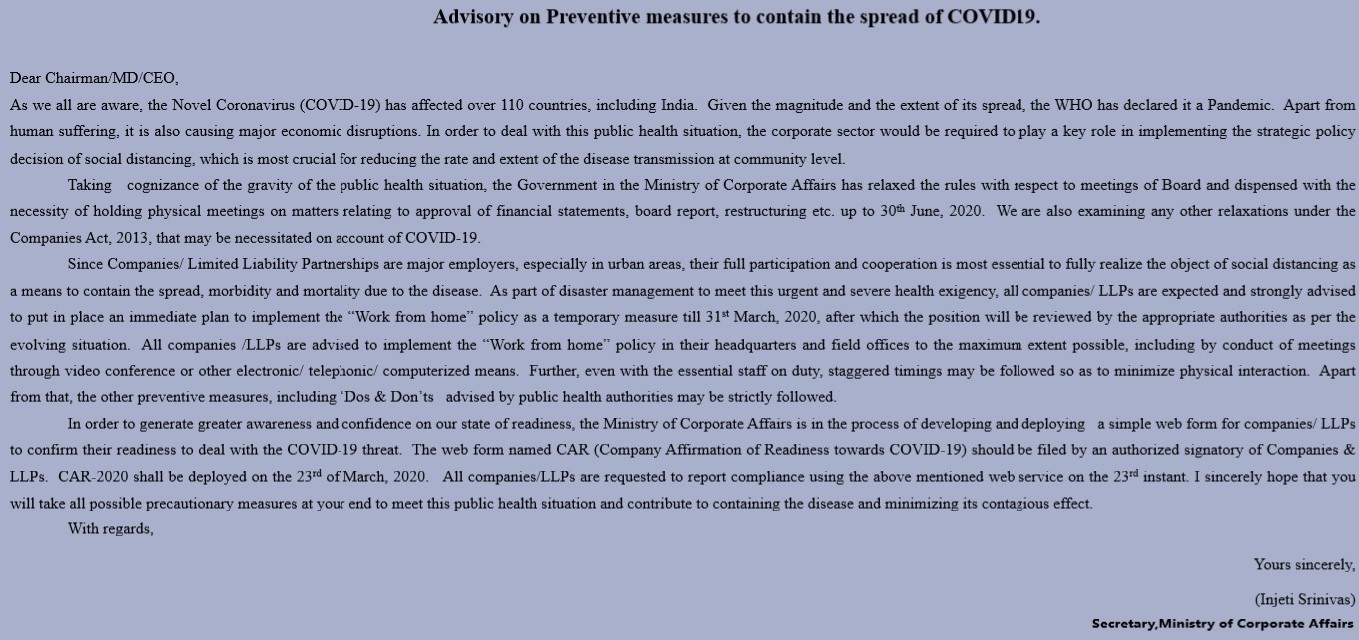

Advisory on Preventive measures to contain the spread of COVID19

Advisory on Preventive measures to contain the spread of COVID19

The Ministry of Corporate Affairs ( MCA ) is in the process of developing and deploying a simple web form named CAR (Company Affirmation of Readiness towards COVID-19) for companies/LLPs to confirm their readiness to deal with the COVID-19 threat.

Since the wake of the Novel Coronavirus(COVID-19) affecting over 110 countries including India, the WHO had declared it a Pandemic. Apart from human suffering, it is also causing major economic disruptions. In order to contain the spreading of the virus, the corporate sector is required to play a key role in implementing the strategic policy decision of social distancing, which is most crucial in reducing the rate and extent of disease transmission at the community level.

Taking cognizance of the gravity of the public health situation, the Government in the Ministry of Corporate Affairs has relaxed the rules with respect of Board and dispensed with the necessity of holding physical meetings on matters relating to approval of financial statements, board report, restructuring etc., up to 30th June, 2020. They are also examining any other relaxation under the Companies Act, 2013 that may be necessitated on account of COVID-19.

As part of disaster management to meet this urgent and severe health exigency, all companies/LLPs are strongly advised to put in place an immediate plan to implement the “Work from Home” in the Headquarters and field offices to the maximum extent possible, including by conduct of meeting through video conference or other electronic/telephonic/computerized means. They further instructed that even with the essential staff on duty, staggered timings may be followed so as to minimize physical interaction. Apart from that, the preventive measures including the Do’s and Don’t’s advised by the public health authorities are to be strictly followed.

The Webform named CAR will be deployed on 23rd March 2020. All companies/LLPs are requested to using compliance with the web form named CAR on the 23rd of March instant while following all possible preventive measures to contain the disease and its contagious effect.

Frequently Asked Questions on (CAR) – 2020

1. To whom is this form applicable?

To All Companies / LLP including small companies, private companies, One Person Company (OPC) .All Companies/LLP include the companies, whether incorporated in India or not, but having operations in India.

2. When will the form be deployed?

The form is expected to be deployed on 23rd March, 2020 and is required to be submitted by 30th March, 2020 (extended by a week).

3. Is there any fees for filing the form?

No.

4. Who can file the form on behalf of Companies / LLP?

CS, CFO, Managing Director, Director, Designated Partners or Authorized person who has been authorised for such purposes.

5. Whose Mobile number has to be entered in the form?

In case of Director / Designated Partner signing the form their mobile number will be automatically prefilled from database. In all other case, the Mobile Number shall be editable should be that of the person who is authenticating the form as it has to be verified by a One Time Password (OTP).

6. What if my organization does not have a whole time / permanent employee?

The form still has to be filed, but the Company / LLP will be eased of future compliance burden, if any.

7. Till when does such policy needs to be in place?

The policy needs to be in place till 31st March, 2020 as per present scenario but may be extended based on the review made by appropriate Govt. Authorities.

8. What if I do not adhere to filing of such web form?

There has not been any information on the same but going by the intent of the form, non – filing of it may not lead to any penal outcome.

9. On what basis can I prepare “Work from Home” policy?

This shall be prepared based on the guidelines and advisory issued by the Government from time to time to check the spread of COVID – 19.

10. How to track the filing of form?

Once the form is filed, a system based acknowledgement will be sent to:

The government had issued new norms for auditors, seeking more disclosures in reports, a move which comes after a series of corporate scams and frauds surfaced over the past few years.

CARO 2020 – Companies (Auditor’s Report) Order, 2020

MCA in place of existing the Companies (Auditor’s Report) Order, 2016, has notified CARO 2020 after consultation with the National Financial Reporting Authority constituted under section 132 of the Companies Act, 2013.

Auditor’s report to contain matters specified in paragraphs 3 and 4. – Every report made by the auditor under section 143 of the Companies Act on the accounts of every company audited by him, to which this Order applies, for the financial years commencing on or after the 1st April, 2019, shall in addition, contain the matters specified in paragraphs 3 and 4, of the CARO 2020.

Provided this Order shall not apply to the auditor’s report on consolidated financial statements except clause (xxi) of paragraph 3.

It shall come into force on the date of its publication in the Official Gazette.

CARO 2020 – Key changes/highlights

Matters to be included in auditor’s report, in CARO 2020 – the reporting clauses are more extensive and detailed than were in CARO2016

Unlike CARO 2016, which required reporting on all fixed assets, new reporting requirements pays attention to Property, Plant, Equipment and intangible assets.

Reporting on revaluation of Property, Plant and Equipments by company

Reporting of proceedings under the Benami Transactions (Prohibition) Act, 1988.

Reporting of compliances if company was sanctioned working capital limits in excess of Rs.5 crores or more from banks or financial institutions.

– whether the quarterly returns or statements filed by the company with such banks or financial institutions are in agreement with the books of account of the Company, if not, to give details;

Reporting of investments in or in providing of any guarantee or security or granting any loans or advances to companies, firms, Limited Liability Partnerships or any other parties.

Reporting of compliances with RBI directives and the provisions the Companies Act with respect to deemed deposits.

Reporting with respect to transactions not recorded in the books of account surrendered or disclosed as income in the income tax proceedings.

Comprehensive reporting requirement for default in the repayment of loans / other borrowings or in the payment of interest

– whether the company is a declared wilful defaulter by any bank or financial institution or other lender;

– whether term loans were applied for the purpose for which the loans were obtained; if not, the amount of loan so diverted and the purpose for which it is used may be reported;

– whether funds raised on short term basis have been utilised for long term purposes, if yes, the nature and amount to be indicated

Reporting on treatment by auditor of whistle-blower complaints received during the year by the company

Reporting on internal audit system

– whether the company has an internal audit system commensurate with the size and nature of its business;

– whether the reports of the Internal Auditors for the period under audit were considered by the statutory auditor;

Reporting on cash losses

Reporting on resignation of the statutory auditors

Reporting on uncertainty of company capable of meeting its liabilities

Reporting transfer of unspent CSR amount to Fund specified in Schedule VII

Reporting on qualifications or adverse remarks by the auditors in the CARO reports of companies included in the consolidated financial statements

It is expected that CARO, 2020 will improve the overall quality of reporting by the auditors and thereby lead to “greater transparency and faith in the financial affairs of the companies.”

As part of Government of India’s Ease of Doing Business (EODB) initiatives, the Ministry of Corporate Affairs would be shortly notifying & deploying a new Web Form christened ‘SPICe+’ (pronounced ‘SPICe Plus’) replacing the existing SPICe form.

SPICe+ would save as many procedures, time and cost for Starting a Business in India and would be applicable for all new company incorporation w.e.f 15th February 2020

Key Features of Spice+

SPICe+ would be an integrated Web Form i.e. fill form online like GST registration forms. The new web form would Facilitate on-screen filing and real time data validation for seamless incorporation of companies.

Information once entered can be saved and modified. All Check form and Pre-scrutiny validations will happen on web form itself.

DSC validation and other validations will happen at Upload Level

Once the SPICe+ is filled completely with all relevant details, the same would then have to be converted into pdf format, with just a click of the mouse button, for affixing DSCs.

Digitally signed applications can then be uploaded along with the linked forms as per the existing process.

Changes/modifications to SPICe+ (even after generating pdf and affixing DSCs), can also be done by editing the same web form

Spice+ would have 2 parts:

a) Part A : for name reservation for new incorporation

b) Part B : Part B offering a bouquet of services i.e.

Incorporation

DIN allotment

Mandatory issue of PAN / TAN

Mandatory issue of EPFO / ESIC registration

Mandatory issue of Profession Tax registration (Maharashtra)

Mandatory Opening of Bank Account for the Company

Allotment of GSTIN (if so applied for)

Part A can be filed first for reserving name or Part A & B can be filed together at one go.

Re submission would be easy, if required.

Registration for EPFO and ESIC shall be mandatory for all new companies incorporated w.e.f 15 February 2020 and no EPFO & ESIC registration nos. shall be separately issued by the respective agencies.

Registration for Profession Tax shall also be mandatory for all new companies incorporated in the State of Maharashtra w.e.f 15th February 2020.

All new companies incorporated through SPICe+ (w.e.f 15th February 2020) would also be mandatorily required to apply for opening the company’s Bank account through the AGILE-PRO linked web form.

Declaration by all Subscribers and first Directors in INC-9 shall be auto-generated in pdf format and would have to be submitted only in Electronic form in all cases, except where:

Total number of subscribers and/or directors is greater than 20 and/or

Any such subscribers and/or directors has neither DIN nor PAN

– The Central government will provide required approvals to such companies for winding up instead of the tribunal – MCA notifies the Companies (Winding Up) Rules, 2020, vide Notification dt. 24 January 2020, comprising of Rules 1 to 191 and Forms WIN 1 to WIN 95, applicable for winding up under the Companies Act 2013 w.e.f. 1 April, 2020

The Ministry of Corporate Affairs (MCA) on Tuesday notified rules for winding up of companies, making it easier for smaller firms to wind up businesses without taking approval.

The rules have provided summary procedures for liquidation of companies with asset size of Rs 1 crore and which have not accepted deposits exceeding Rs 25 lakh and turnover less than Rs 50 crore and total loan under Rs 25 lakh.

The Central government will provide required approvals to such companies for winding up instead of the tribunal.

The rules said, “…wherever the word Tribunal is mentioned, it shall be read as Central Government and with further directions issued by the Central Government as may be necessary, from time to time.”

G.S.R. (E).- In exercise of the powers conferred by sub-sections (1) and (2) of section 468 and sub-sections (1) and (2) of section 469 of the Companies Act, 2013 (18 of 2013), the Central Government hereby makes the following rules, namely:-

Part 1: GENERAL

1. Short title, commencement and application.-

(1) These rules may be called the Companies (Winding Up) Rules, 2020.

(2) They shall come into force on the 1st day of April, 2020.

(3) These rules shall apply to winding up under of Companies Act 2013 (18 of 2013).

2. Definitions.-

In these rules, unless the context or subject matter otherwise requires, –

(a) “Act” means the Companies Act, 2013 (18 of 2013);

(b) “Form” means a Form annexed to these rules;

(c) “Registrar” means the Registrar of the National Company Law Tribunal or National Company Law Appellate Tribunal and includes such other officer of the Tribunal or Bench thereof to whom the powers and functions of the Registrar are assigned;

(d) “Registry” means the Registry of the Tribunal or any of its Benches or of the Appellate Tribunal, as the case may be, which keeps records of the applications and documents relating thereto;

(e) “Section” means section of the Act;

(f) words and expressions used and not defined in these rules but defined in the Act shall have the meanings respectively assigned to them in the Act.

Part II: WINDING UP BY TRIBUNAL

3. Petition for winding up.-

(1) For the purposes of sub-section (1) of section 272, a petition for winding up of a company shall be presented in Form WIN 1 or Form WIN 2, as the case may be, with such variations as the circumstances may require, and shall be presented in triplicate.

(2) Every petition shall be verified by an affidavit made by the petitioner or by the petitioners, where there are more than one petitioners, and in case the petition is presented by a body corporate, by the Director, Secretary or any other authorised person thereof, and such affidavit shall be in Form WIN 3.

4. Statement of affairs.- The statement of affairs, as required to be filed under sub-section (4) of section 272 or sub-section (1) of section 274, shall be in Form WIN 4 and shall contain information up to the date which shall not be more than thirty days prior to the date of filling the petition or filling the objection as applicable and the statement of affairs shall be made in duplicate, duly verified by an affidavit, and affidavit of concurrence of the statement of affairs shall be in Form WIN 5.

5. Admission of petition and directions as to advertisement.- Upon filing of the petition, it shall be posted before the Tribunal for admission of the petition and fixing a date for the hearing thereof and for appropriate directions as to the advertisements to be published and the persons, if any, upon whom copies of the petition are to be served, and where the petition has been filed by a person other than the company, the Tribunal may, if it thinks fit, direct notice to be given to the company and give an opportunity of being heard, before giving directions as to the advertisement of the petition, if any, and the petitioner shall bear all costs of the advertisement.

6. Copy of petition to be furnished.- Every contributory of the company shall be entitled to be furnished by the petitioner or by his authorised representative with a copy of the petition within twenty four hours of his requiring the same on payment of five rupees per page.

7. Advertisement of petition.- Subject to any directions of the Tribunal, notice of the petition shall be advertised not less than fourteen days before the date fixed for hearing in any daily newspaper in English and vernacular language widely circulated in the State or Union territory in which the registered office of the company is situated, and the advertisement shall be in Form WIN 6.

8. Application for leave to withdraw petition.-

(1) A petition for winding up shall not be withdrawn after presentation without the leave of the Tribunal subject to compliance with any order of the Tribunal, including as to costs.

(2) An application for leave to withdraw a petition for winding up which has been advertised in accordance with the provisions of rule 7 shall not be heard at any time before the date fixed in the advertisement for the hearing of the petition.

The provision is likely to require a change in the Act, according to experts.

The provision is likely to require a change in the Act, according to experts.

As part of Government of India’s Ease of Doing Business (EODB) initiatives, the Ministry of Corporate Affairs would be shortly notifying & deploying a new Web Form christened ‘SPICe+’ (pronounced ‘SPICe Plus’) replacing the existing SPICe form.

As part of Government of India’s Ease of Doing Business (EODB) initiatives, the Ministry of Corporate Affairs would be shortly notifying & deploying a new Web Form christened ‘SPICe+’ (pronounced ‘SPICe Plus’) replacing the existing SPICe form.