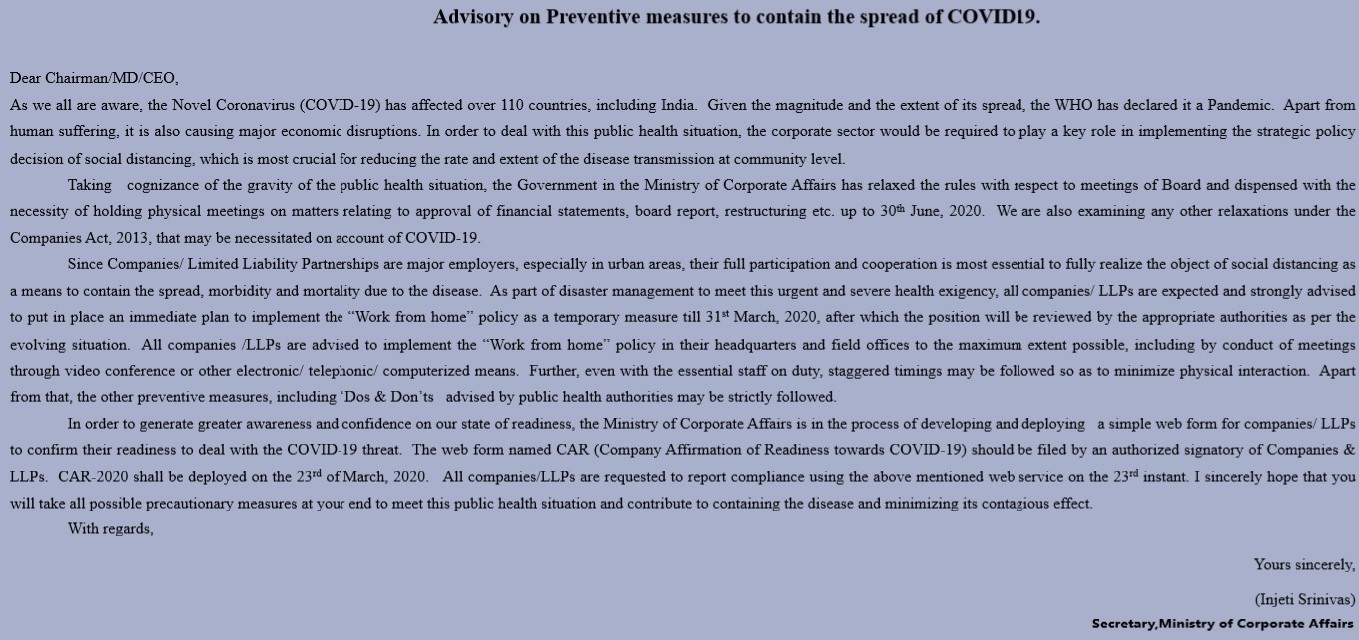

Advisory on Preventive measures to contain the spread of COVID19

The Ministry of Corporate Affairs ( MCA ) is in the process of developing and deploying a simple web form named CAR (Company Affirmation of Readiness towards COVID-19) for companies/LLPs to confirm their readiness to deal with the COVID-19 threat.

Since the wake of the Novel Coronavirus(COVID-19) affecting over 110 countries including India, the WHO had declared it a Pandemic. Apart from human suffering, it is also causing major economic disruptions. In order to contain the spreading of the virus, the corporate sector is required to play a key role in implementing the strategic policy decision of social distancing, which is most crucial in reducing the rate and extent of disease transmission at the community level.

Taking cognizance of the gravity of the public health situation, the Government in the Ministry of Corporate Affairs has relaxed the rules with respect of Board and dispensed with the necessity of holding physical meetings on matters relating to approval of financial statements, board report, restructuring etc., up to 30th June, 2020. They are also examining any other relaxation under the Companies Act, 2013 that may be necessitated on account of COVID-19.

As part of disaster management to meet this urgent and severe health exigency, all companies/LLPs are strongly advised to put in place an immediate plan to implement the “Work from Home” in the Headquarters and field offices to the maximum extent possible, including by conduct of meeting through video conference or other electronic/telephonic/computerized means. They further instructed that even with the essential staff on duty, staggered timings may be followed so as to minimize physical interaction. Apart from that, the preventive measures including the Do’s and Don’t’s advised by the public health authorities are to be strictly followed.

The Webform named CAR will be deployed on 23rd March 2020. All companies/LLPs are requested to using compliance with the web form named CAR on the 23rd of March instant while following all possible preventive measures to contain the disease and its contagious effect.

Frequently Asked Questions on (CAR) – 2020

1. To whom is this form applicable?

To All Companies / LLP including small companies, private companies, One Person Company (OPC) .All Companies/LLP include the companies, whether incorporated in India or not, but having operations in India.

2. When will the form be deployed?

The form is expected to be deployed on 23rd March, 2020 and is required to be submitted by 30th March, 2020 (extended by a week).

3. Is there any fees for filing the form?

No.

4. Who can file the form on behalf of Companies / LLP?

CS, CFO, Managing Director, Director, Designated Partners or Authorized person who has been authorised for such purposes.

5. Whose Mobile number has to be entered in the form?

In case of Director / Designated Partner signing the form their mobile number will be automatically prefilled from database. In all other case, the Mobile Number shall be editable should be that of the person who is authenticating the form as it has to be verified by a One Time Password (OTP).

6. What if my organization does not have a whole time / permanent employee?

The form still has to be filed, but the Company / LLP will be eased of future compliance burden, if any.

7. Till when does such policy needs to be in place?

The policy needs to be in place till 31st March, 2020 as per present scenario but may be extended based on the review made by appropriate Govt. Authorities.

8. What if I do not adhere to filing of such web form?

There has not been any information on the same but going by the intent of the form, non – filing of it may not lead to any penal outcome.

9. On what basis can I prepare “Work from Home” policy?

This shall be prepared based on the guidelines and advisory issued by the Government from time to time to check the spread of COVID – 19.

10. How to track the filing of form?

Once the form is filed, a system based acknowledgement will be sent to:

- Email id of the Company / LLP

- Email Id of the person affirming the form

- Email id of FO user submitting the affirmation.

First 15 features (1-15 points) as PART-I:-

First 15 features (1-15 points) as PART-I:- As part of Government of India’s Ease of Doing Business (EODB) initiatives, the Ministry of Corporate Affairs would be shortly notifying & deploying a new Web Form christened ‘SPICe+’ (pronounced ‘SPICe Plus’) replacing the existing SPICe form.

As part of Government of India’s Ease of Doing Business (EODB) initiatives, the Ministry of Corporate Affairs would be shortly notifying & deploying a new Web Form christened ‘SPICe+’ (pronounced ‘SPICe Plus’) replacing the existing SPICe form. In the union budget 2020, the following section

In the union budget 2020, the following section