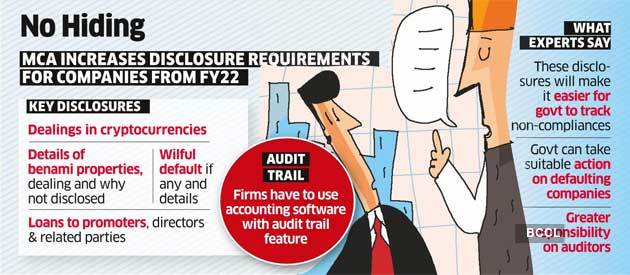

Starting April 1, companies must state if they have been declared wilful defaulters by banks, financial institutions or other lenders. The ministry also mandated companies to record audit trails of their accounts. Firms using accounting software to maintain their books need to use features that can record the audit trail of each transaction and create an edit log, including the date of such changes.

India Inc will have to declare investments in cryptocurrencies, relationships with dissolved companies and loans extended to related parties, among a host of other disclosures mandated by the government to improve transparency.

Starting April 1, companies must state if they have been declared wilful defaulters by banks, financial institutions or other lenders.

The ministry of corporate affairs announced a new set of disclosures rules under the Companies Act on Wednesday, significantly enhancing financial and general reporting requirements for companies.

The ministry also mandated companies to record audit trails of their accounts. Firms using accounting software to maintain their books need to use features that can record the audit trail of each transaction and create an edit log, including the date of such changes.

Amending the Companies (Accounts) Rules, the ministry said firms must ensure the audit trail feature on the accounting software cannot be disabled. The move is aimed at curbing backdated entries and will affect mainly smaller companies as the bigger ones already use such software, according to Shalu Kedia, a partner at Nangia & Co.

Additional disclosures to be made under schedule III of the Companies Act, 2013, relate to matters such as corporate social responsibility spending, cryptocurrency dealings, benami property, relationship with struck-off, or dissolved, companies, and ageing of payables & receivables with vendors.

These disclosures will make it easier for the government to track non-compliance and take action against defaulting companies, experts said.

“Earlier, the companies were only required to disclose trade payables and receivables, but there was no requirement to provide ageing details. This disclosure will mandate the company to disclose the ageing payment cycle for MSMEs and non-MSME vendors,” said Nischal Arora, a partner at Nangia Andersen LLP.

Dealings in cryptocurrencies must be disclosed with details of the profit or loss on such transactions, amounts of such currency held and deposits or advances from any person for trading or investing in these currencies.

“While the government is already working on a bill on cryptocurrency, the disclosure for such currency has made it clear that the government wants to gather data on cryptocurrency,” said Arora.

Another important change was related to the disclosure of any benami property holdings.

“This disclosure is another step to improve transparency for the stakeholders as they will have to disclose any proceeding that has been initiated or pending against the company for holding any benami property and also provide a reasoning and view on the same,” said Amit Maheshwari, a partner at AKM Global.

The additional disclosures will make it mandatory for companies to provide details of shortfall in CSR spending for the previous years, including reasons for not meeting targets.

Loans granted to promoters, directors and related parties that are repayable on demand or without specific repayment terms from companies must be declared in terms of amount and percentage to total loans granted.

While this will push firms to regularly service their loans, it “will be helpful for the investor and other lenders to be aware about these types of companies before making any investment or lending the money,” Maheshwari said.

Use of analytics and AI augment India’s vision for #aatmanirbharta & development Plan to come up with a machine learning driven MCA-21 Version 3.0 is in process: Budget 2021

In the Budget 2021, it was mentioned that govt. will be establishing technology based on data analytics, artificial intelligence, machine learning tools in the areas of finance, taxation and online compliance monitoring among others.

Accordingly, MCA has now established a Central Scrutiny Centre (CSC) for carrying out scrutiny of Straight Through Processes (STP) e-forms filed by the companies under the Company Law made thereunder.

The Ministry of Corporate Affairs established a Central Scrutiny Centre (CSC) for carrying out scrutiny of Straight Through Processes (STP) e-forms filed by the companies under the Act and the rules.

The notification said that the CSC shall function under the administrative control of the e-governance Cell of the Ministry of Corporate Affairs.

The CSC shall carry out scrutiny of the aforesaid forms and forward findings thereon, wherever required, to the concerned jurisdictional Registrar of Companies for further necessary action under the provisions of the Act and the rules made thereunder.

“The CSC shall be located at the Indian Institute of Corporate Affairs (IICA), Plot No. 6, 7, 8, Sector 5, IMT Manesar, District Gurgaon (Haryana), Pin Code- 122050,” the MCA notified.

The notification shall come into force from the 23rd March, 2021.

The Ministry for Corporate Affairs Ministry has hinted that the suspension of the Insolvency and Bankruptcy Code (IBC) is likely to be revoked after March 24.

he Ministry for Corporate Affairs Ministry has hinted that the suspension of the Insolvency and Bankruptcy Code (IBC) is likely to be revoked after March 24.

This has been conveyed in a written submission by the Ministry to the Standing Committee on Finance headed by Jayant Sinha. This submission came along with the note on allocation and utilisation of funds for the Insolvency and Bankruptcy Board of India (IBBI), which is the insolvency regulator.

“It is expected that the suspension of the Insolvency and Bankruptcy Code will likely be revoked after March 24 and activities of IBBI will be increased manifold in the next financial year,” the MCA submission said.

Given that the economy is now in recovery mode, it is widely expected that the Centre will revoke the suspension after March 24. Also, any extension of the suspension this date would require Parliament approval, legal experts said.

6-month suspension

A six-month suspension was first introduced in June 5 for debt defaults arising post March 25, 2020, when the Covid-induced lockdown was announced. The suspension was to end on September 25, but was extended up to December 25. In mid-December, the suspension was further extended by three months, up to March 25.

In effect, the government had ensured that any corporate debt default during Covid, between March 25, 2020 and March 25, 2021, will remain outside the IBC purview. However, for defaults before March 25, 2020, there will be no protection, said experts.

While the law protects the corporate debtor from insolvency proceedings for the one-year period till March 25, it does not disallow such action against the personal guarantors of a corporate debtor.

‘Go digital’

In a separate development, the Standing Committee on Finance has, in its latest report tabled in the Lok Sabha on Tuesday, directed the MCA to move towards full digitisation of its functions, particularly of its statutory bodies. It sees the quasi judicial bodies facing a deluge of cases post withdrawal of the moratorium and underscored stressed the need to enhance their digital and infrastructural capacities to handle the increase in caseload.

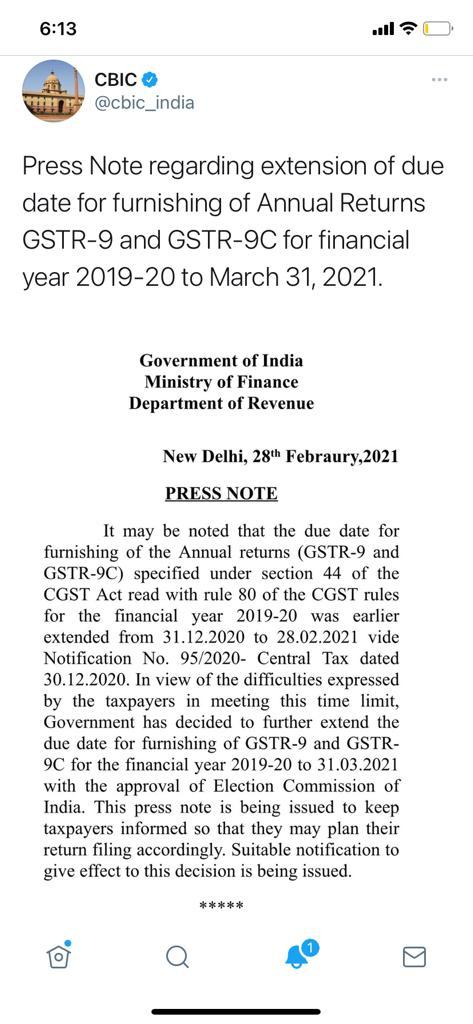

CBIC had extended, vide Press Note regarding extension of due date for furnishing of Annual Returns GSTR-9 and GSTR-9C for financial year 2019-20 to March 31, 2021.

This is the second extension given by the government. The deadline was earlier extended from December 31,2020 to February 28.

MCA relaxes levy of additional fees in filing of e-forms AOC-4, AOC-4 (CFS), AOC-4 XBRL and AOC-4 Non-XBRL for the financial year ended on 31.03.2020 under the Companies Act, 2013

Keeping in view of various requests received from stakeholders regarding relaxation on levy of additional fees for annual financial statement filings required to be done for the financial year ended on 31.03.2020, it has been decided that no additional fees shall be levied upto 15.02.2021 for the filing of e-forms AOC-4, AOC-4 (CFS), AOC-4 XBRL and AQC-4 Non-XBRL in respect of the financial year ended on 31.03.2020.

During the said period, only normal fees shall be payable for the filing of the aforementioned e-forms.

Earlier, the Annual General Meeting for adoption of the Audited Financial Statements, Directors Report and Auditors’ Report was extended by 3 months from September 30 to December 30, 2020.

Accordingly, the companies were required file Audited Financial Statements before January 31st, 2021.

This has now been further relaxed for another 15 days up to February 15, 2021, for filing of the eForms with Ministry of Corporate affairs (MCA).

The RBI notified Rotation Policy instead of Cooling Period for Bank Branch Audit for CAs.

The Reserve Bank of India (RBI) notified the change in norms on eligibility, empanelment, the appointment of Statutory Branch Auditors in Public Sector Banks from years 2020-21 onwards.

The RBI notified Rotation Policy instead of Cooling Period for Bank Branch Audit for CAs. In other words, the concept of compulsory rest for two years for audit firms located in the specified centres, after completion of four years of continuous branch audit, followed till Financial Year 2019-20 has been done away with.

Instead, the branch auditors across all the centres of the country, on completion of four years of continuous branch audit, will be subjected to the policy of rotation i.e. they may be considered for appointment as SBAs of any other PSB.

However, the audit firms will not be eligible to be re-appointed as SBAs, in the same bank where they completed their audit assignment prior to rest/rotation, at least for one cycle of four years.

The RBI further notified the change on norms for selection of branches of Public Sector Banks (PSBs) for Statutory Audit.

Firstly, statutory branch audit of PSBs should be carried out so as to cover 90% of all funded and 90% of all non-funded credit exposures of a bank.

The selection of branches for statutory audit shall include a representative cross section of rural/semi-urban/urban and metropolitan branches, predominantly including branches which are not subjected to concurrent audit.

CPUs/LPUs/and other centralised hubs, by whatever nomenclature called, would be included for branch audit every year.

The selection of branches shall be finalised by each PSB with the consent of their Statutory Central Auditor/s. Secondly, in respect of those branches, which are subject to concurrent audit by chartered accountants and not selected for branch audit, LFARs and other certifications done by concurrent auditors will be submitted to the Managing Director & CEO of the bank.

The banks in turn will consolidate/compile all such LFARs and other certifications submitted by the Concurrent Auditors and submit to Statutory Central Auditor/s as an internal document of the bank.

The RBI notified the change in the procedure for appointment of Statutory Branch Auditors.

Firstly, the list of eligible auditors/audit firms will be prepared by the Institute of Chartered Accountants of India (ICAI) as per the norms prescribed by RBI.

Secondly, the list will be subjected to scrutiny by RBI for identifying the continuing and rested firms and excluding audit firms who have been denied audit.

Thirdly, RBI will, thereafter, forward the final list of all eligible auditors/audit firms to PSBs for selection of the required number of branch auditors/audit firms.

Banks will be required to clearly advise the selected audit firms that each audit firm can take up audit assignments (branch audit) in one PSB only. The audit firm should give its consent in writing for consideration of appointment in the bank concerned for the particular year and the subsequent continuing years.

Fourthly, the consent given by an audit firm is irrevocable and no request from audit firms for changing the bank, after giving its consent will be entertained.

Fifthly, after the selection of branch auditors, PSBs will be required to recommend the names of both continuing and selected branch auditors to RBI for seeking its prior approval before their actual appointment, as per statutory requirement.

The RBI while elaboration on the change in general guidelines applicable to appointment of Statutory Branch Auditors stated that SBAs will have a maximum tenure of four years in a particular bank.

The appointment of SBAs will be made on an annual basis, subject to their fulfilling the eligibility norms prescribed by RBI from time to time, and also subject to their suitability.

“While allotting branches, banks are required to select auditors/audit firms which are in close proximity to their offices/branches. Banks are also required to have a suitable mix of various categories of auditors / audit firms while selecting the branch auditors keeping in view the size of the branches to be audited.

Banks are advised to allot branches, to the extent possible, to the audit firms taking into consideration their category and audit experience in such a way that specialised and larger branches are audited by bigger/experienced audit firms,” the RBI said.

The audit firms retiring as Statutory Central Auditors from a PSB shall not be eligible to be appointed as SBAs of the same PSB during the prescribed cooling period for SCAs from that particular PSB.

The RBI notified change in the eligibility norms for the empanelment of audit firms to be appointed as Statutory Branch Auditors in PSBs.

The Double Tax Avoidance Agreement (DTAA) is essentially a bilateral agreement entered into between two countries. The basic objective is to promote and foster economic trade and investment between two Countries by avoiding double taxation.

WHAT IS DOUBLE TAXATION OF INCOME?

When the same income is taxed more than once, due to levying of tax by two or more jurisdictions, on the same income asset or financial transaction, this results in double taxation. This may happen, when an assessee – an Individual or a company, is taxed more than once for the same income in India, either on the basis of place of residence or on the basis of source of accrual, which leads to double taxation.

Countries have started entering into Double Taxation Avoidance Agreements (DTAA) with other countries to resolve double taxation issue so as to ease out the tax burden of their taxpayers. This relief for taxes paid in foreign country is given to taxpayer while taxing the same income in the India, which is termed as Foreign Tax Credit (FTC).

B. HOW DOUBLE TAXATION AVOIDANCE AGREEMENT (DTAA) WORKS?

In any country, the tax is levied based on 1) Source Rule and 2) the Residence Rule.

The source rule holds that income is to be taxed in the country in which it originates irrespective of whether the income accrues to a resident or a non-resident whereas the residence rule stipulates that the power to tax should rest with the country in which the taxpayer resides.

If both rules apply simultaneously to a business entity and it were to suffer tax at both ends, the cost of operating on an international business would become prohibitive and would deter the process of globalization. It is from this point of view that Double Taxation Avoidance Agreements (DTAA) have become significant.

Where the Central Government has entered into an agreement with the Government of any country outside India or specified territory outside India, for granting relief of tax, or as the case may be, avoidance of double taxation, then, in relation to the assessee to whom such agreement applies, the provisions of this Act shall apply to the extent they are more beneficial to that assessee.

Impact of Double Taxation Avoidance Agreement:

1. WHERE DTAA EXISTS (SECTION 90):

There are two methods of granting relief under Double Taxation Avoidance Agreement.

Exemption method – A particular income is taxed in one of the both countries and exempted in the other

Example- For the Income from Dividend, Interest, royalty and fees for technical services Source Rule is applicable in treaty with Greece, Libyan and United Arab Republic. So for citizen of these 3 countries if the dividend, interest, royalty or fees for technical services is arising in India, then it will be solely taxable in India only and for a resident if such income is arising in any of these 3 countries then the income will solely be taxed in these 3 countries and it will not at all be taxable in India.

Tax Credit method- The income is taxed in both the countries as per the treaty and the country of residence will allow the tax credit / reduction for the tax charged in the country of Origin.

Example- Mr. A (an Indian resident) has received salary from a US company for job in US. Since Mr. A is a resident so his global Income will be taxable in India. In this case, source country is US (since the service has been rendered in US) and resident country is India. So at the time of computation of tax liability of Mr. A, the tax paid in US will be allowed as set off against his total tax liability but limited to the tax payable on such foreign income at Indian tax rates.

Therefore DTAA determines which method to be used first and, if the income is taxable only in one country then exemption method shall be used, but if the same is taxable in both countries then tax credit method comes into play.

In case where Bilateral agreement has been entered under section 90 of the Income Tax Act, 1961 with a foreign country then the assessee has an option either to be taxed as per the Double Taxation Avoidance Agreement (hereinafter referred as “DTAA”) or as per the normal provisions of Income Tax Act 1961, whichever is more beneficial to assessee.

Example- As per DTAA between India and Germany, tax on Interest is specified @ 10% whereas under Income Tax Act 1961, it depends on slab rates for individuals & HUF and flat rates (generally 30%) for other kind of assessees (like firm, company etc). Hence, one can follow DTAA and pay tax @ 10% only.

2. WHERE DTAA DOES NOT EXIST (SECTION 91):

i. If any person who is resident in India in any previous year, in respect of income which arose outside India (and which is not deemed to accrue or arise in India), and paid in any country with which there is no agreement under section 90 for the relief or avoidance of double taxation, then he shall be entitled to the deduction from the tax payable in India,

ii. Deduction shall be lower of:

Tax calculated on such double taxed income at the Indian rates.

Tax calculated on such double taxed income at the rate of tax of the said country

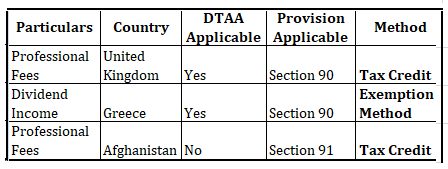

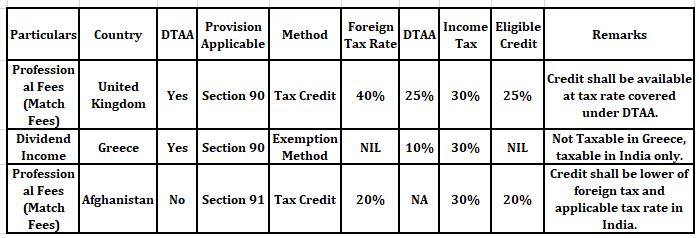

Example :Suppose Indian Sportsman, resident of India who earns foreign income in form of match fees being professional and dividend income as his other foreign income from the below mentioned countries, then in such case following provisions and method shall govern his taxability:

Therefore, both Tax Credit method u/s 90 and Section 91 deals with Foreign Tax Credit, but still having DTAA is beneficial because assessee is taxed at rate beneficial to him, which is not so in case of NO DTAA.

C. HOW CREDIT OF FOREIGN TAX IS AVAILED IN INDIA?

Rule 128 governs the credit of taxes paid on income earned in foreign country. An assessee shall be eligible to claim credit of foreign tax paid if he complies with provisions stated under Rule 128 of the Income Tax Rules which are discussed as follows:

1. Analysis of Rule 128 introduced under Indian Income Tax Rules

Applicability of the rules

The rules came into force with effect from 1.4.2017 applicable only for resident assessee for the amount of foreign taxes paid by him in a foreign country. The credit is available only if income corresponding to the taxes is offered for tax or assessed to tax in India during the year in which the credit is claimed.

In the cases where the income for which the foreign taxes paid or deducted is offered to taxes for more than one year, the credit will be given across the years in the same proportion to which the income is offered to tax in India during the year in which credit is claimed.

2. Foreign Tax Credit Defined under sub-rule 2:

i. FTC in case of DTAA countries: Taxes that are covered under the said agreement.

ii. FTC in case of other countries (No DTAA): Tax payable under the law in force in that country in the nature of income-tax referred in Section 91.

The LOWER OF tax payable under the act on such income or the foreign tax paid is eligible as FTC. However, while considering the foreign tax paid, it cannot exceed the amount arrived as per DTAA with that country.

3. Utilization of Foreign Tax Credit:

FTC is eligible for adjustment against the tax, surcharge and cess payable under the IT Act. FTC cannot be adjusted against interest, fee or penalty payable under the IT Act. FTC is not available in case foreign tax or part thereof is disputed by the assessee in any manner.

4. Exception & Conditions relating to Foreign Tax Credits:

Credit is allowed in the year in which the income is offered/assessed in India upon the assessee within six months from the end of the month in which dispute is finally settled and assessee furnishes:

Evidence of settlement of dispute

Evidence that the liability for payment of such foreign tax has been discharged and

Undertaking that no refund in respect of such amount is directly or indirectly been claimed. Further, credit for each source of income shall be calculated separately for a specific country and then aggregated. The rate of exchange to be taken for this purpose is TT buying rate on the last day of the month immediately preceding month in which the tax is paid or deducted.

5. Documents required under Foreign Tax Credit:

Furnish FORM 67 duly verified and certified by a Chartered Accountant on or before furnishing return of income u/s 139(1)

Furnishing following certificates or statement specifying:

Nature of income and,

Amount of Tax paid of which statement given by:

Tax authority of that country, or

Person responsible for deduction of such tax, or

Signed by the assessee:

In this case, it should be accompanied with – an acknowledgment of online payment or receipt or bank counterfoil for proof of payment of tax, if tax is paid by the assessee

In case of tax deduction, proof of such Tax deducted at source

D. JUDICIAL PRECEDENTS UNDER FOREIGN TAX CREDIT

1. WIPRO LIMITED F TS – 565 – HC – 2015 (KAR)

The judgment of WIPRO provides that merely because the taxpayer’s income is exempt from tax due to a limited tax holiday provided under the ITA, does not mean that foreign tax credit can be simply denied.

2. TATA SONS [2011] 43 SOT 27 (MUM AT)

Though DTAA with USA provides credit only the tax paid with the Federal Government, credit was extended to the Taxes paid to State taxes as well. It has considered the relief u/s 91 which was beneficial to the assessee than that of the DTAA.

3. VIJAY ELECTRICALS [2015] 54 COM 19 (HYD AT)

Tax credit is available even if the same is not deposited with the overseas Government in the year in which the income is taxable.