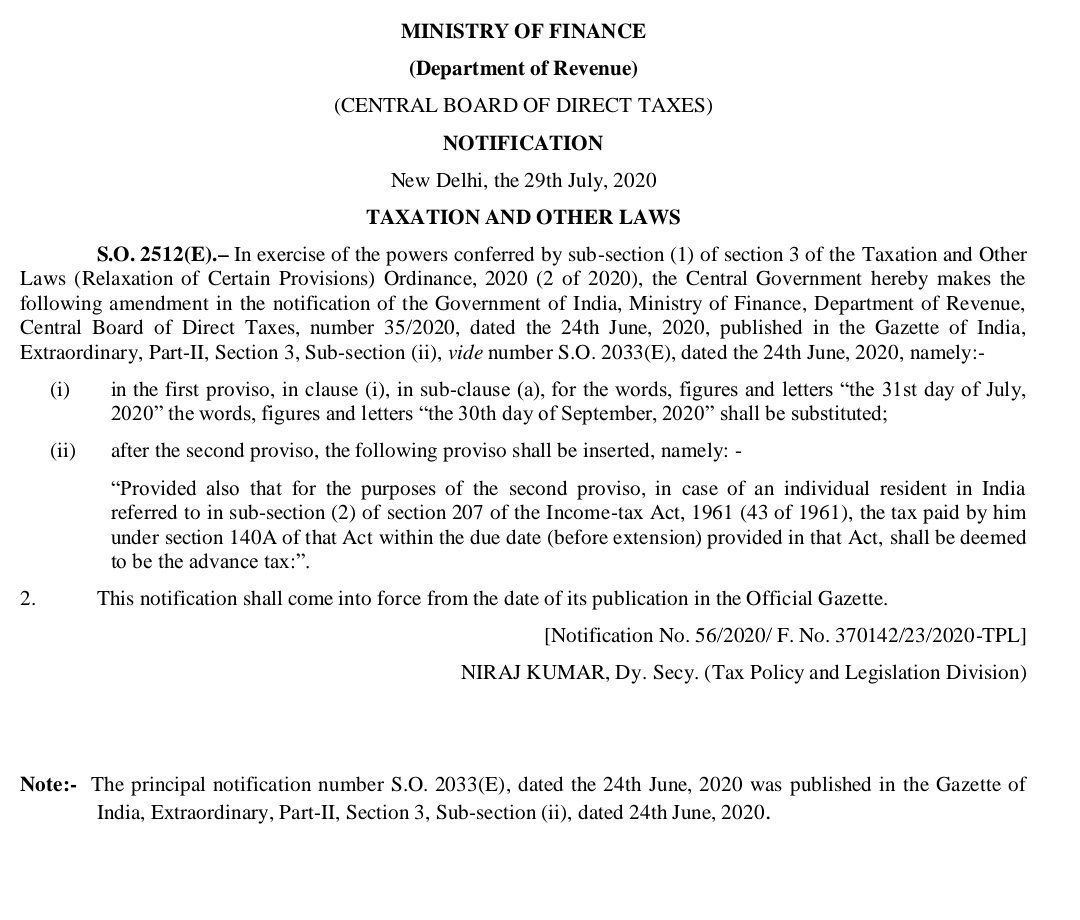

The Central Board of Direct Taxes (CBDT) on Wednesday (July 29) extended the deadline for filing income tax returns for 2018-19 fiscal till September 30 due to corona virus COVID-19 pandemic.

The Central Board of Direct Taxes (CBDT) on Wednesday (July 29) extended the deadline for filing income tax returns for 2018-19 fiscal till September 30 due to coronavirus COVID-19 pandemic.

“In view of the constraints due to the Covid pandemic & to further ease compliances for taxpayers, CBDT extends the due date for filing of Income Tax Returns for FY 2018-19 (AY 2019-20) from 31st July, 2020 to 30th September, 2020,” the Income Tax Department said in a tweet.

It is to be noted that this is the third extension given by the Centre to taxpayers to file both original and revised tax returns for 2018-19 fiscal.

In March, the Centre had extended the due date from March 31 to June 30 due to corona virus COVID-19 pandemic. Later in June, the date was again extended by a month till July 31.

If an individual fails to file the belated ITR, if due, by the deadline (i.e., September 30, 2020), then he/she will not be able to file the income tax return for the financial year 2018-19.

The CBDT has said that an individual can also file a revised ITR for FY2018-19 within this deadline.

The Income Tax department’s data analysis has identified certain taxpayers with high value transactions who have not filed ITR for AY 2019-20 (i.e. FY 2018-19). In addition to the non-filers, another set of return filers have also been identified wherein the high-value transactions do not appear to be in line with their Income Tax Return.

The Board said that the objective of the e-campaign is to facilitate taxpayers to validate their financial transaction information against information available with the IT department and promote voluntary compliance, especially for the assesses for the FY 2018-19 so that they do not need to get into notice and scrutiny process.

Under this e-campaign the Income Tax Department will send email/sms to identified taxpayers to verify their financial transactions related information received by the I-T department from various sources such as Statement of Financial Transactions (SFT), Tax Deduction at Source (TDS), Tax Collection at Source TCS), Foreign Remittances (Form 15CC) etc,” CBDT said.

It added that the department has collected information related to GST, exports, imports and transactions in securities, derivatives, commodities and mutual funds under information triangulation set up.

The campaign is scheduled for 11 days starting from July 20, 2020 and ending on July 31, 2020.

With the new e-campaign, the taxpayers will be able to access details of their high value transactions on the designated portal. They will also be able to submit online response by selecting among any of these options:

(i) Information is correct,

(ii) Information is not fully correct,

(iii) Information related to other person/year,

(iv) Information is duplicate/included in other displayed information, and

(v) Information is denied.

Also, department has clarified that there would be no need to visit any Income Tax office, as the response has to be submitted online.

This is a dual way move of the department, on one hand this will get more assessees under scrutiny and thus help in identifying defaulters. While on the other hand this will increase the speed of process and avoid unnecessary mental harassment of the assessees.

It may be noted that the last date for filing as well as revising the Income Tax Return for Assessment Year 2019-20 (relevant to FY 2018-19) is 31st July 2020.

The Central Board of Direct Taxes (CBDT) has issued refunds worth Rs 71,229 crore in more than 21.24 lakh cases upto 11th July, 2020, to help taxpayers with liquidity during COVID-19 pandemic, since the Government’s decision of 8th April, 2020 to issue pending income tax refunds at the earliest.

Income tax refunds amounting to Rs. 24,603 crore have been issued in 19.79 lakh cases to taxpayers and corporate tax refunds amounting to Rs. 46,626 crore in 1.45 lakh cases have been issued to taxpayers during COVID-19.

It is stated that the government has laid great emphasis on providing tax related services to the taxpayers without any hassles and is aware that during these difficult times of COVID-19 pandemic, many of the taxpayers are waiting to see that their tax demands and refunds reach finality as quickly as possible.

It is further emphasized that all the refund related cleaning up of the tax demands are being taken up on priority and is likely to be completed by 31st August, 2020.

Also, all applications for rectifications and for giving effect to appeal orders are to be uploaded on the ITBA.

It has been decided to do all the work of rectification and appeal effect on ITBA only.

It is reiterated that taxpayers, for quick processing of their refunds, should provide immediate response to the emails of I-T Department.

A quick response from the taxpayer in this regard would facilitate the I-T Department to process their refunds expeditiously.

Many taxpayers have submitted their responses electronically for rectification, appeal effects or tax credits. These are being attended to in a time bound manner.

All refunds have been issued online and directly into the bank accounts of the taxpayers.

-Through this one time relaxation scheme, ITR for FY 2014-15 to FY 2018-19 can be verified, on or before 30th September 2020. – All such verified ITRs shall be processed on or before 31st December 2020. – ITRs can be verified digitally through EVC or by sending duly signed a copy to CPC Bangalore.

The Central Board of Direct Taxes (CBDT) on Monday notified the one-time relaxation for verification of tax return for the Assessment Year 2015-16, 2016-17, 2017-18, 2018-19 and 2019-20, which are pending due to non-filing of ITR- V form and processing of such returns.

It has been brought to the notice of CBDT that a large number of electronically filed ITR still remains pending with the Income-Tax Department for want of receipt of a valid ITR-V Form at CPC, Bengaluru from the taxpayers concerned.

In law, consequences of non-filing the ITR-V within the time allowed is significant as such a return is/can be declared Non-est in law. Thereafter, all the consequences for non-filing a tax return, as specified in the Income-tax Act,1961 follow.

“The CBDT, in the exercise of powers under section 119 of the Act, in case of returns for Assessment Years 2015-16, 2016-17, 2017-18, 2018-19 and 2019-20 which were uploaded electronically by the taxpayer within the time allowed under section 139 of the Act and which have remained incomplete due to non-submission of ITR-V Form for verification, hereby permits verification of such returns either by sending a duly signed physical copy of ITR-V to CPC, Bengaluru through speed post or through EVC/OTP modes as listed in para 1 above.

Such verification process must be completed by 30.09.2020,” the circular said.

However, the circular clarified that this relaxation shall not apply in those cases, where during the intervening period, the Income Tax Department has already taken recourse to any other measure as specified in the Act for ensuring filing of a tax return by the taxpayer concerned after declaring the return as Non-est.

“CBDT also relaxes the time-frame for issuing the intimation as provided in the second proviso to sub-section (1) of Section 143 of the Act and directs that such returns shall be processed by 31.12.2020 and intimation of processing of such returns shall be sent to the taxpayer concerned as per the laid down procedure.

In refund cases, while determining the interest, provision of section 244A (2) of the Act would apply,” the circular said.

“There is a need to create a regulator or authority for data business, which provides centralized regulation for all non-personal data exchanges,” the government-appointed panel said in the report. Such a regulator would be armed with legal powers to request data, supervise data sharing requests and settle disputes“.

A formal Memorandum of Understanding (MoU) was signed today between the Central Board of Direct Taxes (CBDT) and the Securities and Exchange Board of India (SEBI) for data exchange between the two organizations.

The MoU was signed by Smt. Anu J. Singh, Pr. DGIT (Systems), CBDT, and Smt. MadhabiPuri Buch, Whole Time Member, SEBI in the presence of senior officers from both the organizations via video conference.

The MoU will facilitate the sharing of data and information between SEBI and CBDT on an automatic and regular basis.

In addition to regular exchange of data, CBDT and SEBI will also exchange with each other, on request and suo moto basis, any information available in their respective databases, for the purpose of carrying out scrutiny, inspection, investigation and prosecution,” SEBI said in a statement.

In addition to regular exchange of data, SEBI and CBDT will also exchange with each other, on request and Suo moto basis, any information available in their respective databases, for the purpose of carrying out their functions under various laws.

The MoU comes into force from the date it was signed and is an ongoing initiative of CBDT and SEBI, who are already collaborating through various existing mechanisms.

A Data Exchange Steering Group has also been constituted for the initiative, which will meet periodically to review the data exchange status and take steps to further improve the effectiveness of the data-sharing mechanism.

The MoU marks the beginning of a new era of cooperation and synergy between SEBI and CBDT.

In the past, SEBI has cracked on several entities who had manipulated the stock prices of listed companies. The regulator had observed in the penny stock scam that promoters and market operators were using the stock exchange platform to evade taxes and launder black money.

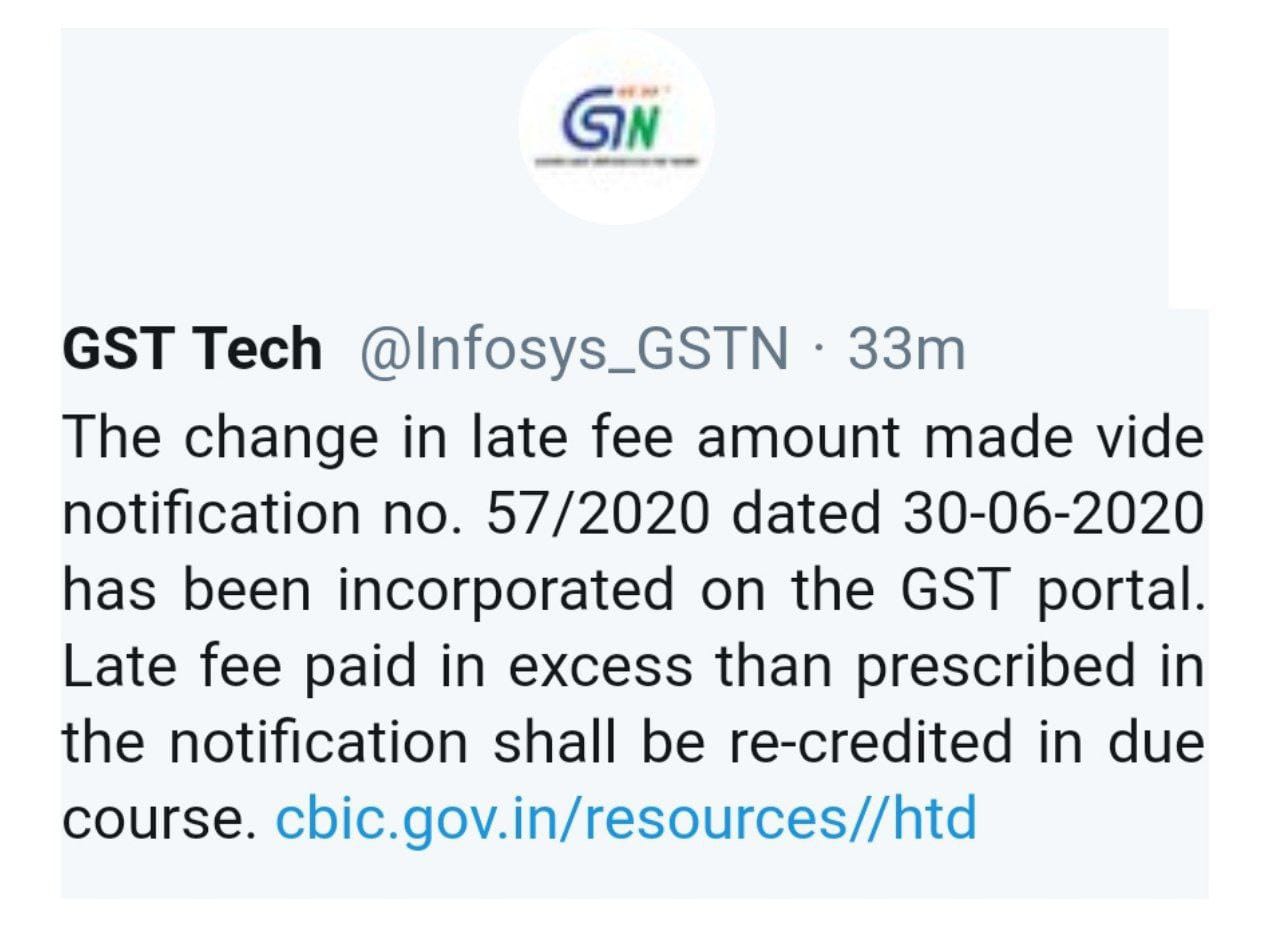

The change in late fee amount made vide notification no. 57/2020 dated 30-06-2020 has been incorporated on the portal. Late fee paid in excess than prescribed in the notification shall be re-credited in due course.

CBIC had vide Noti 57/2020 has stated that that maximum Late Fee for Form GSTR 3B has been capped at Rs. 500 for tax period July 2017 to July 2020 subject to returns being filed before 30th September 2020.

But portal was not updated and it has levied late fees as per old calculation. Hence, GSTN Tech twitter posted that “The change in late fee amount made vide notification no. 57/2020 dated 30-06-2020 has been incorporated on the GST portal.

Late fee paid in excess than prescribed in the notification shall be re-credited in due course.”

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs Notification No. 57/2020 – Central Tax

New Delhi, the 30th June, 2020

G.S.R…..(E).— In exercise of the powers conferred by section 128 of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereafter in this notification referred to as the said Act), read with section 148 of the said Act, the Government, on the recommendations of the Council, hereby makes the following further amendments in the notification of the Government of India in the Ministry of Finance (Department of Revenue), No. 76/2018– Central Tax, dated the 31st December, 2018, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub- section (i) vide number G.S.R. 1253(E), dated the 31st December, 2018, namely :–

In the said notification, after the third proviso, the following provisos shall be inserted, namely: –

“Provided also that for the class of registered persons mentioned in column (2) of the Table of the above proviso, who fail to furnish the returns for the tax period as specified in column (3) of the said Table, according to the condition mentioned in the corresponding entry in column (4) of the said Table, but furnishes the said return till the 30th day of September, 2020, the total amount of late fee payable under section 47 of the said Act, shall stand waived which is in excess of two hundred and fifty rupees and shall stand fully waived for those taxpayers where the total amount of central tax payable in the said return is nil:

Provided also that for the taxpayers having an aggregate turnover of more than rupees 5 crores in the preceding financial year, who fail to furnish the return in FORM GSTR-3B for the months of May, 2020 to July, 2020, by the due date but furnish the said return till the 30th day of September, 2020, the total amount of late fee under section 47 of the said Act, shall stand waived which is in excess of two hundred and fifty rupees and shall stand fully waived for those taxpayers where the total amount of central tax payable in the said return is nil.”.

2. This notification shall be deemed to have come into effect from the 25th day of June, 2020.

[F. No. CBEC-20/06/08/2020-GST]

(Pramod Kumar)

Director, Government of India

Note: The principal notification No. 76/2018-Central Tax, dated 31st December, 2018 was published in the Gazette of India, Extraordinary, vide number G.S.R. 1253(E), dated the 31st December, 2018 and was last amended vide notification number 52/2020 – Central Tax, dated the 24th June, 2020, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i) vide number G.S.R.405 (E), dated the 24th June, 2020.

The levy is applicable only for large cash withdrawals. The intent is to minimize cash transactions and expand digital payments to enlarge the ambit of organized transactions over time.

In order to tighten the noose on those who don’t file income tax returns (ITR) despite earning taxable income and discourage cash transactions, the Finance Act 2020 introduced higher TDS (Tax Deducted at Source) rates on cash withdrawals for those who do not file ITR. The rates are applicable from 1 July.

Those who haven’t filed ITR for the past three financial years will have to pay TDS at the rate of 2%, if the amount withdrawn from the bank is above ₹20 lakh but doesn’t exceed ₹1 crore in a financial year. If the amount withdrawn exceeds ₹1 crore, TDS will be deducted at the rate of 5% under Section 194N of the Income-tax Act, 1961, for those who do not file ITR.

However, if you withdraw cash above ₹1 crore in a FY, you will still have to pay TDS whether you file ITR or not. In July 2019, the government, through Section 194N, had first introduced TDS at the rate of 2% on cash withdrawals above ₹1 crore in a financial year. This continues to be applicable.

“It is important to note that TDS shall be required to be deducted only when the aggregate amount of cash withdrawal during the FY by an individual from one or more of his bank accounts exceeds ₹20 lakh or ₹1 crore, as the case may be,” said Parizad Sirwalla, partner and head, global mobility services, tax, KPMG in India.

Further, tax will be deducted only on the amount exceeding the said thresholds. “If the individual withdraws a sum of money on regular intervals, the bank or financial institution will have to deduct TDS from the amount once the total sum withdrawn exceeds the threshold in a FY,” said Sirwalla.

For example, if person A has filed his ITR and if he withdraws cash up to ₹1 crore, then no TDS will be applicable. In case person A withdraws cash, which is more than ₹1 crore, then only 2% TDS will be applicable. If person A has withdrawn ₹1.25 crore in two transaction of ₹75 lakh in and ₹50 lakh, the TDS liability will only be on the excess amount that is ₹25 lakh.

On the other hand, if person B has not filed his ITR for the last three financial years and if he withdraws cash between ₹20 lakh and ₹1 crore, then 2% TDS will be applicable. In case person B withdraws cash which is more than ₹1 crore, then 5% TDS will be applicable.

“In case, the individual does not furnish the PAN to the bank or financial institution, then a TDS at a higher rate of 20% will become applicable,” said Sirwalla.

TDS will be applicable on withdrawals from banks, co-operative banks and post offices. The limit will apply on all accounts in the same bank. So, if you have multiple accounts with the same bank, then TDS will be applicable once you breach the mandatory limit across all the accounts or in any one of the account with the same bank. But for accounts with different banks, the limit will apply separately.

Banks will need to keep track of cash withdrawals and once the limit is breached, they will need to deduct TDS.

“Banks are asking declaration from people to ensure they have filed a return in the past three years or in any one of the last three years. This is done by banks for easier tracking as they wouldn’t know if the person has filed ITR or not,” said Sandeep Sehgal, director, taxes and regulatory, AKM Global.

The purpose of slapping this TDS is to minimize cash transactions and push digital payments.

“The levy is applicable only for large cash withdrawals in excess of ₹20 lakh/100 lakh per annum, as the case may be. The intent is to minimize cash transactions and expand digital payments to enlarge the ambit of organized transactions over time. So if individuals need to avoid this TDS levy, they should ensure that their cash withdrawals are restricted to the bare minimum and that the bulk of their payments happen through banking or digital means,” said Divakar Vijayasarathy, founder and managing partner, DVS Advisors LLP.