Finance minister Nirmala Sitharaman announced a slew of measures for extension of statutory and regulatory compliances in view of the corona virus pandemic spreading its wings and impacting the economy.

Allaying fears that there is no economic emergency in the country, FM said that the Economic Task Force will soon announce an economic relief package to deal with the impact of the corona virus pandemic on the economy.

These are largely in the area of ease of doing business, by providing reliefs in extension of due dates for compliances and reliefs from late fee and penalties, in view of the lock downs announced in several states and districts.

Income Tax

- The last date for filing income tax returns for Financial Year 2018-19, extended from 31st March, 2020 to 30th June, 2020.

- Aadhaar-PAN linking date extended from 31st March, 2020 to 30th June, 2020.

- Vivad se Vishwas scheme – no additional 10% amount, if payment made by June 30, 2020.

- Due dates for issue of notice, intimation, notification, approval order, sanction order, filing of appeal, furnishing of return, statements, applications, reports, any other documents and time limit for completion of proceedings by the authority and any compliance by the taxpayer including investment in saving instruments or investments for roll over benefit of capital gains under Income Tax Act, Wealth Tax Act, Prohibition of Benami Property Transaction Act, Black Money Act, STT law, CTT Law, Equalization Levy law, Vivad Se Vishwas law where the time limit is expiring between 20th March 2020 to 29th June 2020 extended to 30th June 2020.

- For delayed payments of advanced tax, self-assessment tax, regular tax, TDS, TCS, equalization levy, STT, CTT made between 20th March 2020 and 30th June 2020, reduced interest rate at 9% instead of 12 %/18 % per annum ( i.e. 0.75% per month instead of 1/1.5 percent per month) will be charged for this period. No late fee/penalty shall be charged for delay relating to this period.

- Necessary legal circulars and legislative amendments for giving effect to the aforesaid relief shall be issued in due course.

GST/Indirect Tax

- Last date for filing GSTR-3B in March, April and May 2020 extended till the last week of 30th June, 2020 for those having aggregate annual turnover less than Rs. 5 Crore. No interest, late fee, and penalty to be charged.

- For any delayed payment made between 20th March 2020 and 30th June 2020 reduced rate of interest @9 % per annum ( current interest rate is 18 % per annum) will be charged. No late fee and penalty to be charged, if complied before till 30th June 2020.

- Date for opting for composition scheme is extended till the last week of June, 2020. Further, the last date for making payments for the quarter ending 31st March, 2020 and filing of return for 2019-20 by the composition dealers will be extended till the last week of June, 2020.

- Date for filing GST annual returns of FY 18-19, which is due on 31st March, 2020 is extended till the last week of June 2020.

- Due date for issue of notice, notification, approval order, sanction order, filing of appeal, furnishing of return, statements, applications, reports, any other documents, time limit for any compliance under the GST laws where the time limit is expiring between 20th March 2020 to 29th June 2020 extended to 30th June 2020.

- Necessary legal circulars and legislative amendments to give effect to the aforesaid GST relief shall follow with the approval of GST Council.

- Payment date under Sabka Vishwas Scheme extended to 30th June, 2020. No interest for this period shall be charged if paid by 30th June, 2020.

Customs

- Custom clearance will operate 24X7 till June 30, 2020.

- Due date for issue of notice, notification, approval order, sanction order, filing of appeal, furnishing applications, reports, any other documents etc., time limit for any compliance under the Customs Act and other allied Laws where the time limit is expiring between 20th March 2020 to 29th June 2020 shall be extended to 30th June 2020.

Financial Services

Relaxations for 3 months

- Debit cardholders to withdraw cash for free from any other banks’ ATM for 3 months

- Waiver of minimum balance fee

- Reduced bank charges for digital trade transactions for all trade finance consumers

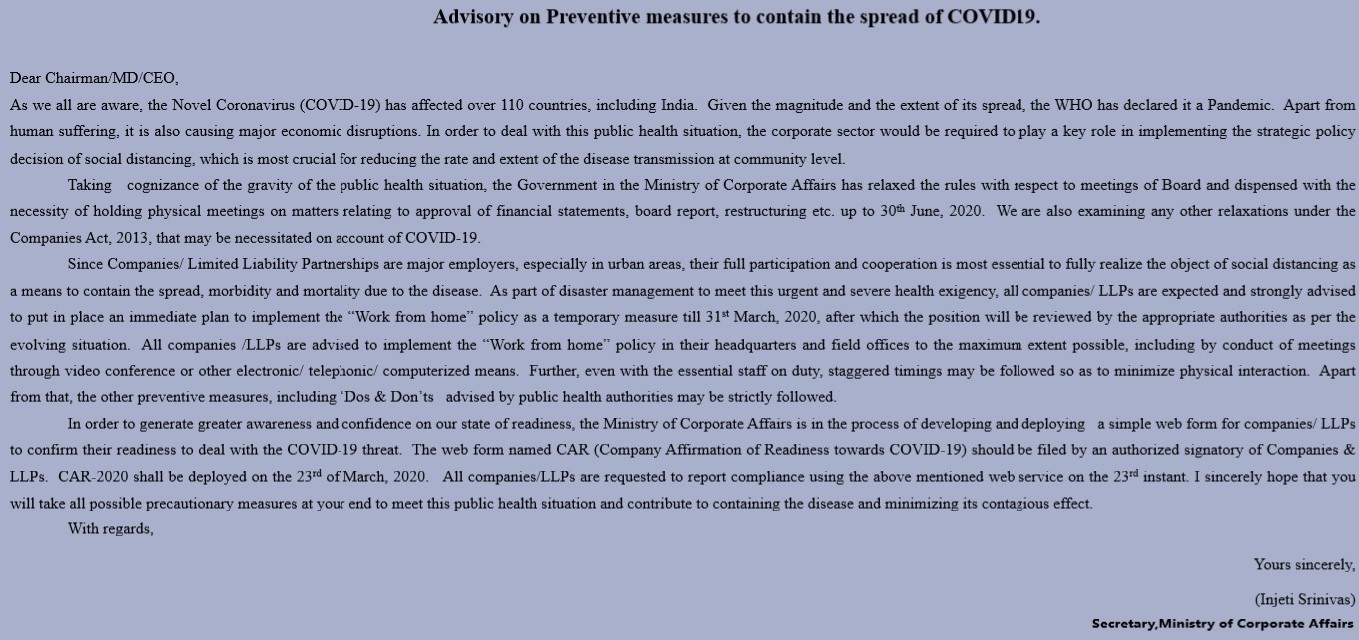

Corporate Affairs

- No additional fees shall be charged for late filing during a moratorium period from 01st April to 30th September 2020, in respect of any document, return, statement etc., required to be filed in the MCA-21 Registry, irrespective of its due date, which will not only reduce the compliance burden, including financial burden of companies/ LLPs at large, but also enable long-standing non-compliant companies/ LLPs to make a ‘fresh start’;

- The mandatory requirement of holding meetings of the Board of the companies within prescribed interval provided in the Companies Act (120 days), 2013, shall be extended by a period of 60 days till next two quarters i.e., till 30th September;

- Applicability of Companies (Auditor’s Report) Order, 2020 shall be made applicable from the financial year 2020-2021 instead of from 2019-2020 notified earlier. This will significantly ease the burden on companies & their auditors for the year 2019-20.

- As per Schedule 4 to the Companies Act, 2013, Independent Directors are required to hold at least one meeting without the attendance of Non-independent directors and members of management. For the year 2019-20, if the IDs of a company have not been able to hold even one meeting, the same shall not be viewed as a violation.

- Requirement to create a Deposit reserve of 20% of deposits maturing during the financial year 2020-21 before 30th April 2020 shall be allowed to be complied with till 30th June 2020.

- Requirement to invest 15% of debentures maturing during a particular year in specified instruments before 30th April 2020, may be done so before 30th June 2020.

- Newly incorporated companies are required to submit commencement of Business certificate within 6 months of incorporation. This is now extended to 12 months.

- Non-compliance of minimum residency in India for a period of at least 182 days by at least one director of every company, under Section 149 of the Companies Act, shall not be treated as a violation.

- Due to the emerging financial distress faced by most companies on account of the large-scale economic distress caused by COVID 19, it has been decided to raise the threshold of default under section 4 of the IBC 2016 to Rs 1 crore (from the existing threshold of Rs 1 lakh). This will by and large prevent triggering of insolvency proceedings against MSMEs. If the current situation continues beyond 30th of April 2020, we may consider suspending section 7, 9 and 10 of the IBC 2016 for a period of 6 months so as to stop companies at large from being forced into insolvency proceedings in such force majeure causes of default.

- Detailed notifications/circulars in this regard shall be issued by the Ministry of Corporate Affairs separately.

Department of Commerce

- Extension of timelines for various compliance and procedures will be given. Detailed notifications will be issued by Ministry of Commerce.

First 15 features (1-15 points) as PART-I:-

First 15 features (1-15 points) as PART-I:- As part of Government of India’s Ease of Doing Business (EODB) initiatives, the Ministry of Corporate Affairs would be shortly notifying & deploying a new Web Form christened ‘SPICe+’ (pronounced ‘SPICe Plus’) replacing the existing SPICe form.

As part of Government of India’s Ease of Doing Business (EODB) initiatives, the Ministry of Corporate Affairs would be shortly notifying & deploying a new Web Form christened ‘SPICe+’ (pronounced ‘SPICe Plus’) replacing the existing SPICe form.