Capital markets regulator Sebi on Wednesday said its actions against auditors for faulty audits are within its “Parliamentary mandate”, and there is no question of “turf wars” on this issue.

SEBI Chairman Ajay Tyagi said the watchdog is working only to protect the interests of investors and limiting its actions to auditors of publicly listed firms.

In 2018, the regulator banned Price Waterhouse for two years from auditing any listed firm for its role in the Satyam Computer Services scam. However, the audit firm had successfully challenged the same in the Securities Appellate Tribunal and got the order quashed.

“It is our parliamentary mandate I would say to see that it is done and there is no trouble there. It goes to the basic issue of investor protection being the parliamentary mandate of Sebi,” he noted.

In November, the Supreme Court stayed a SAT order which had held that Sebi does not have the power to bar auditors.

“Our position is very simple — if they’re auditing listed companies based on which investors are investing, and if we find that that work has not been done properly and in investors’ interest, some audit firms should not be allowed to audit for sometime of the listed companies,” Tyagi said at an event here.

According to Tyagi, audit firms are important gatekeepers who help companies put out results and financial performance to the stock exchanges, based on which investors take the call whether to invest or not.

“It is not our case that Sebi is the agency which registers or regulates the auditors. It is nothing like that… We are not de-registering auditors. We don’t have the authority and we don’t wish to have that authority,” he said.

He also made it clear that Sebi’s expectation is that faulty audits should not lead to inflated profits or dividends.

Regarding IPO market, Tyagi said there has been an improvement in activities lately and that nearly a dozen issues of over Rs 15,000 crore are in the pipeline.

The regulator has given its wish-list for the budget to the finance ministry, includes ways to increase the activities in the corporate bond market, he said.

Apart from decision to set up the NCLAT Bench in Chennai, five new Benches of the NCLT were set up during 2018-2019 in Jaipur, Cuttack, Kochi, Indore and Amaravati. Benches of the NCLT are set up in states depending on the case load and other relevant factors.

The Centre has decided to set up a Bench of the National Company Law Appellate Tribunal (NCLAT) in Chennai for clearing pending litigations.

Apart from decision to set up the NCLAT Bench in Chennai, five new Benches of the NCLT were set up during 2018-2019 in Jaipur, Cuttack, Kochi, Indore and Amaravati.

The government has recently appointed another 28 members in the NCLT and 4 more members in the NCLAT. For capacity building of members, regular colloquiums are being held, apart from e-Court project being implemented in a few Benches with heavy case load.

Anurag Singh Thakur, Union minister for state for finance & corporate affairs, in a written reply to a question in the Lok Sabha said the Chennai NCLAT Bench is being set up in pursuance of judgment of the Supreme Court.

Benches of the NCLT are set up in states depending on the case load and other relevant factors. Considering the heavy case load at some existing Benches, additional members have been appointed and additional courts have been operationalised from time to time.

Thakur also said the government is taking steps to strengthen the NCLT and NCLAT in terms of number of Benches, number of courts and number of members to reduce pendency.

Press Information Bureau Government of India Ministry of Corporate Affairs

02-December-2019 15:12 IST

Government to set up National Company Law Appellate Tribunal Bench in Chennai

In pursuance of judgement of Hon’ble Supreme Court, the Government has decided to set up a bench of National Company Law Appellate Tribunal (NCLAT) at Chennai.

This was stated by Shri Anurag Singh Thakur, Union Minister for State for Finance & Corporate Affairs, in a written reply to a question in Lok Sabha today.

Benches of National Company Law Tribunal (NCLT) are set up in various States depending on the case load and other relevant factors. Considering the heavy case load at some existing benches, additional members have been appointed and additional courts have been operationalised from time to time.

The Minister further stated that the Government is taking all steps to strengthen the NCLT and NCLAT in terms of number of benches, number of courts and number of members, to reduce the pendency.

Apart from decision to set up NCLAT bench at Chennai, five new benches of NCLT have been set up during 2018-2019 at Jaipur, Cuttack, Kochi, Indore and Amaravati. The Government has recently appointed 28 more members in NCLT and 4 more members in NCLAT. For capacity building of members, regular colloquiums are being held. e-Court project has also been implemented in a few benches with heavy case load.

On November 18, 2019 the Companies (Meetings of Board and its Powers) Second Amendment Rules, 2019 (“Amendment Rules“) amended certain threshold limits prescribed by the Rules.

The central government notified the Companies (Meetings of Board and its Powers) Second Amendment Rules, 2019 on 18 November 2019. The amendment rules amend sub-clause 3 of rule 15 of the Companies (Meetings of Board and its Powers) Rules, 2014. The amendment rules alter the various transaction thresholds within which the board may authorize a related party transaction without referring the matter to the shareholders pursuant to section 188(1) (Related party transactions) of the Companies Act, 2013.

Rule 15 provides for conditions applicable to the board taking up, discussing and approving a related party contract or arrangement. The first proviso to section 188(1) of the act provides that no contract or arrangement which exceeds certain monetary thresholds, in relation to the company’s paid-up share capital or otherwise, may be entered into without the prior approval of the shareholders by a resolution. The thresholds in relation to this proviso to section 188(1) of the act are prescribed by the rules and have been amended through the amendment rules as follows:

For a contract or arrangement in relation to a sale, purchase or supply of any goods, previously the threshold, was the lower of: (1) 10% or more of the turnover of the company; or (2)₹1 billion. The amendment rules have relaxed the threshold and fixed it at 10% or more of turnover of the company.

Similarly, for a contract or arrangement for selling or otherwise disposing of, or buying property of any kind, previously the threshold for requiring a shareholder resolution was the lower of: (1) 10% or more of the turnover of the company; or (2)₹1 billion. The amendment rules have relaxed the threshold and fixed it at 10% or more of turnover of the company.

The amendment rules has similarly amended the threshold for a contract or arrangement in relation to leasing of property any kind, and in relation to availing or rendering of any services (directly, or through the appointment of an agent). The amendment rules now fix the threshold at 10% or more of turnover of the company.

Accordingly, the ministry has relaxed the thresholds and made it simpler for companies to ensure ease of business, and the ease of entering into related party transactions.

Nature of Related Party Transactions

Earlier Threshold Limit*

Amended Threshold Limit*

Sale, purchase or supply

of any goods or material (directly or through an agent).

Amounting to ten percent (10%) or more of turnover or Rs. 100 Crore, whichever is lower.

Amounting to ten percent (10%) or more of the turnover of the company.

Selling or otherwise

disposing of, or buying, property of any kind (directly or through an agent).

Amounting to ten percent (10%) or more of net worth or Rs. 100 Crore, whichever is lower.

Amounting to ten percent (10%) or more of the turnover of the company.

Leasing of property of

any kind.

Amounting to ten percent (10%) or more of net worth or 10 percent (10%) or more of turnover Rs. 100 Crore, whichever is lower.

Amounting to ten percent (10%) or more of the turnover of the company.

Availing or rendering of any services (directly or through an agent)

Amounting to ten percent(10%)or more of turnover or Rs. 50 Crore, whichever is lower

Amounting to ten percent (10%) or more of the turnover of the company

*limits specified above shall apply for transaction or transactions to be entered into either individually or taken together with the previous transactions during a financial year.

Appointment to any

office or place of profit in the company, subsidiary company or associate company

Remuneration exceeding

Rs. 2,50,000 per month

No Change

Underwriting the

subscription of any securities or derivatives of the company

Remuneration exceeding

one percent (1%) of net worth

The provisions for resolution for individuals under the Insolvency and Bankruptcy Code (IBC) is being implemented in a phased manner. On Friday, the corporate affairs ministry said the provision pertaining to personal guarantors to corporate debtors will be in force from December 1 A case is taken up for resolution under the law only after approval from the National Company Law Tribunal.

The insolvency regime for individual guarantors to corporate debtors will be in force from December 1, according to the government.

The provisions for resolution for individuals under the Insolvency and Bankruptcy Code (IBC) is being implemented in a phased manner.

On Friday, the corporate affairs ministry said the provision pertaining to personal guarantors to corporate debtors would come into force from December 1.

The Code provides for a market-driven and time-bound resolution for stressed assets.

A case is taken up for resolution under the law only after approval from the National Company Law Tribunal (NCLT).

In October, Corporate Affairs Secretary Injeti Srinivas said personal insolvency regime would be fully operational in one year.

“In the first phase, personal guarantor to a corporate debtor is almost under commencement. The next would be the fresh start process, basically giving relief to very small borrowers who are not in a position to repay the debt. That may be in another four to six months. Then proprietorship and partnership and others,” he had said.

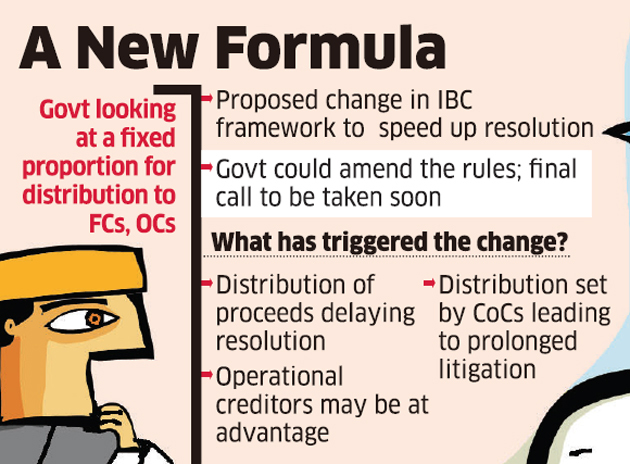

The Centre is looking at further changes to the IBC as it doesn’t want to leave any room for litigation on the distribution of proceeds.

The government is considering a formula for distributing the proceeds of insolvency resolution among financial and operational creditors in a fixed proportion, said people with knowledge of the matter. The goal is to protect the interests of operational creditors and reduce delays due to litigation, ensuring that the objective of the Insolvency and Bankruptcy Code (IBC) is preserved.

“This is one of the solutions that is being looked at,” an official said. The government will take a final call only after extensive deliberations, he added.

Distribution of resolution proceeds has emerged as one of the key factors behind the extended litigation, delaying major insolvency cases. Dissatisfied operational creditors have been the source of such cases in some instances.

The Supreme Court is currently deciding on the distribution of proceeds in the case of Essar Steel, which entered the National Company Law Tribunal (NCLT) system in August 2017. The process was thought to have ended when Arcelor Mittal’s Rs 42,000-crore bid for the debt-ridden steel manufacturer was approved in March 2019. But the original promoters, the Ruias, opposed approval of the plan, questioning Arcelor Mittal’s eligibility.

Operational creditors rejected the plan on the grounds of discriminatory treatment. Financial creditor Standard Chartered Bank has also gone to court against the resolution plan on the same grounds. Financial creditors moved the Supreme Court after the National Company Law Appellate Tribunal (NCLAT) ordered proportional recovery for both financial and operational creditors. Under the IBC, cases have to be decided within a 330-day window.

The decision to change the rules to grant greater protection to operational

creditors had come from the “highest levels of the government,” said one of the

persons.

The Centre is looking at further changes to the IBC as it doesn’t want to

leave any room for litigation on the distribution of proceeds, the person said.

The IBC is regarded as one of the signal reforms of the first Narendra Modi

government. The process got bogged down in litigation over some of the biggest

cases, blunting the IBC’s aspiration of speeding up bankruptcy resolution and

cleaning up banks’ books. The 2016 IBC has already been tweaked several times

toward this end.

Operational creditors had slightly higher recoveries than financial

creditors, according to data available with the government, said the person

cited above. The Insolvency and Bankruptcy Board of India has pegged the

average recovery for financial creditors in cases where there was successful

resolution at 41.5% at the end of the September quarter.

In the latest set of amendments to the IBC, carried out in the budget

session of parliament, the government had clarified that the CoC would have the

right to decide on the distribution of proceeds but that all creditors must

receive liquidation value or the amount they would receive if resolution

proceeds were distributed according to the ‘waterfall mechanism,’ whichever is

higher.

The waterfall mechanism under the IBC outlines the order of priority for

repayment to creditors in the event of liquidation.

Under this, secured creditors have to be paid fully before any payments can

be made to unsecured financial creditors who in turn have priority over

operational creditors.

Experts said the government will have to come up with a balanced

formulation. Setting a high fixed proportion for operational creditors could

prompt CoCs to opt for liquidation instead of resolution. “At present, in many

cases, operational creditors are not getting anything,” said Manoj Kumar, partner

at Corporate Professionals.

In a relief to taxpayers, the government on Thursday extended the due dates for filing GST annual returns for 2017-18 to December 31 and for the financial year 2018-19, to March 31 next year.

The dates for filing the reconciliation statement has also been extended accordingly.

In another relief, it has also decided to simplify the two GST forms by making various fields of these forms as optional, the Central Board of Indirect Taxes and Customs (CBIC) said in a statement.

“The government has decided today (Thursday) to extend the due dates of filing of Form GSTR-9 (Annual Return) and Form GSTR-9C (Reconciliation Statement) for 2017-18 to December 31, 2019 and for 2018-19 to March 2020,” it said.

The earlier deadline for filing of GSTR-9 and GSTR-9C for 2017-18 was November 30, 2019, while that for 2018-19 was December 31, 2019.

Notifications regarding the extension of the dates have been issued.

This is the fourth extension being given to businesses to comply with the return filing requirement for the July-April period of FY18 in view of the numerous changes in rules as well as the difficulties faced by them in shifting to the new technology reliant indirect tax regime.

GST return Form GSTR-9C is a statement of reconciliation between the GST annual return and the audited financial statement of the tax payer.

The CBIC in the revenue department has also notified the amendments regarding the simplification of the annual return and reconciliation statement forms.

A reconciliation statement allow taxpayers to not provide split of input tax credit availed on inputs, input services and capital goods for 2017-18 and 2018-19.

CBIC further said it is expected that with the simplifications in the two forms and the extension of deadlines, “all the GST taxpayers would be able to file their annual returns along with reconciliation statement in time”.

Various representations regarding challenges faced by taxpayers in filing of GSTR-9 and GSTR-9C were received on which by the government has “acted in a very responsive manner”, the CBIC statement added.

Deactivation of DIN for non-compliance of KYC by company Directors has since been marked as ‘Deactivated due to non-filing of DIR-3 KYC’.

The Ministry of Corporate Affairs website (“MCA”), MCA has stated that the DINs which have not complied with the requirement of filing DIR-3 KYC have been marked as ‘Deactivated due to non-filing of DIR-3 KYC’.

The last date for filing DIR-3 KYC for the financial year 2018-19 has expired on 14th October 2019.

The process of deactivating the non-compliant DINs was in progress and has since been completed by MCA. The form DIR-3 KYC and web service DIR-3 KYC were not available for filing during the pendency of this activity.

Filing of DIR-3 KYC and DIR-3 KYC WEB can be made after completion of the scheduled activity, as above when the form & service are re-deployed on the portal after payment of applicable fees.

The DINs which have not complied with the requirement of filing DIR-3 KYC has since been marked as ‘Deactivated due to non-filing of DIR-3 KYC’.

Such DINs are not allowed to be used for filing any e-forms on the MCA21 portal.

In case the present status of your DIN is ‘Deactivated due to non-filing of DIR-3 KYC’, you are required to file ‘KYC’ using e-form DIR-3 KYC or DIR-3-KYC-WEB service as applicable with prescribed fee of INR 5000 to re-activate your de-activated DIN.

The revised FAQs related to DIR-3 KYC have been updated, giving detailed guidelines as below:

Capital markets regulator Sebi on Wednesday said its actions against auditors for faulty audits are within its “Parliamentary mandate”, and there is no question of “turf wars” on this issue.

Capital markets regulator Sebi on Wednesday said its actions against auditors for faulty audits are within its “Parliamentary mandate”, and there is no question of “turf wars” on this issue.