The Ministry of Corporate Affairs (MCA) has again extended the due date of filing Annual Return and Financial Statement.

The MCA has again relaxed the levy of additional fees for filing of e-forms AOC-4, AOC-4 (CFS), AOC-4, AOC-4 XBRL AOC-4 Non-XBRL till 15.03.2022 and for filing of e-forms MGT-7/MGT-7A for the financial year ended on 31.03.2021 till 31.03.2022.

MGT-7 is an electronic form provided by the Ministry of Corporate affairs to all the corporates in order to fill their annual return details. This e-form is maintained by the Registrar of Companies via electronic mode and on the basis of the statement of correctness given by the company.

Form AOC 4 is used to file the financial statements for each financial year with the Registrar of Companies (ROC). In the case of consolidated financial statements, the company shall file the AOC 4.

Keeping in view the extension of timelines for audit/ tax audit and finalization of accounts under the Income Tax Act, 1961, this extension was very much required to synchronize with the inter-connected chain of events.

Accordingly, the ROC annual return due date for FY 2020-21 stands extended for companies, without payment of additional fee, as under:

MCA grants extension of time for filing Annual Financial Statements (AOC-4) and Annual Returns (MGT-7) without additional fees.

The Ministry of Corporate Affairs has recently granted the much-needed relief by extending the dates for filing of the 5 important e-forms with the removal of additional fees on the e-forms, namely Forms Annual Financial Statements -AOC-4, AOC-4 (CFS), AOC-4, AOC-4 XBRL AOC-4 Non-XBRL, and Annual Returns -MGT -7 / MGT -7A, filing to the Financial Year ended 31st March 2021 under the Companies Act 2013.

The extended due dates for filing of e-forms such as AOC-4, AOC-4 (CFS), AOC-4 XBRL, AOC-4 Non-XBRL are 15th February 2022 and for filing of e-forms such as MGT-7, and MGT-7A are 28th February 2022, for all stakeholders, without any additional fees.

The extension of due dates has been done as per the demand of the stakeholders for the filing of financial statements for the financial year ended 31.03.2021.

Extension of last date to file e-forms AOC-4, AOC-4 CFS, AOC-4 XBRL, AOC-4 Non-XBRL and MGT-7/7A for the FY 2020-21 to 31.12.2021

On October 29, 2021, the Ministry of Corporate Affairs (MCA) has announced the relaxation in levy of additional fees in filing of e-forms AOC-4, AOC-4 (CFS), AOC-4, AOC-4 XBRL AOC-4 Non-XBRL and MGT-7 / MGT-7A for the financial year ended on March 31, 2021 under the Companies Act, 2013.

It has been decided no additional fees shall be levied upto 31st December 2021 for the filing of e-forms in respect of the financial year ended on 31.03.2021.

During the said period, only normal fees shall be payable for the filing of the aforementioned e-forms.

Keeping in view of various requests received from stakeholders regarding relaxation on levy of additional fees for annual financial statement filings required to be done for the financial year ended on 31.03.2021, it has been decided that no additional fees shall be levied upto 31.12.2021 for the filing of e-forms AOC-4, AOC-4 (CFS), AOC-4 XBRL, AOC-4 Non-XBRL and MGT-7/MGT-7A in respect of the financial year ended on 31.03.2021. During the said period, only normal fees shall be payable for the filing of the aforementioned e-forms.

Further to the extension of time for holding of Annual General Meeting (AGM) for the financial year ended on 31/03/2021, granted by MCA on 23 rd September, 2021 by two months, this relaxation is now announced by MCA to facilitate the filing of Annual Financial Statements by the stake holders.

MCA has extended the Due Date for Holding of AGMs by the companies, by 2 months from the original due date in respect of the financial year 2020-21 ended on 31/03/2021. Accordingly, respective ROCs have issued extension Orders, which are available at the link below:

MCA Office Memorandum dt. 23/09/2021: Extension of time for holding of Annual General Meeting (AGM) for the Financial year ended on 31/03/2021

1. The Central Government has received representations seeking extension of time for holding Annual General Meeting (AGM) for the financial year 2020-21 ending on 31/03/2021 citing many difficulties faced due to second wave of Covid-19 and consequent lockdowns etc.

2. Accordingly, it has been decided to advise the Registrar of Companies (RoCs) to accord approval for extension of time for a period of two Months beyond the due date by which companies are required to conduct their AGMs for the financial year 2020-21 ended on 31/03/2021.

3. Kindly find enclosed a copy of the standard template for the order to be issued by RoCs under third proviso to sub-section (1) of section 96 of the Companies Act, 2013 ( the Act) for granting extension of time for conducting of AGM for the Financial Year 2020-21 ended on 31/03/2021.

4. Please take this action with utmost urgency and issue order before the close of the office today and forward the copy of the order to this office before for consolidation and uploading it on the MCA21 website. Also display this order on the Notice Board of your respective offices.

5. This issues with approval of the Competent Authority.

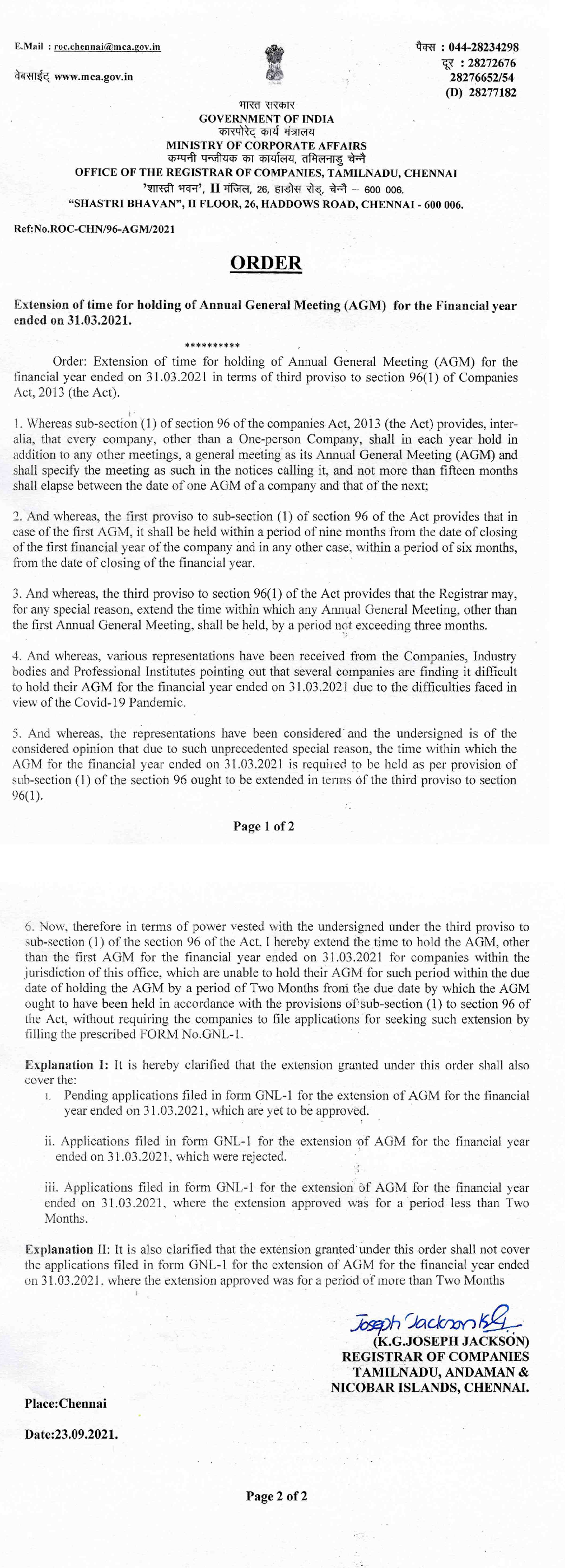

The extension of time by two months issued by ROC, Chennai is as below. The respective ROCs in the country have issued orders under third proviso to sub-section (1) of section 96 of the Companies Act, 2013 granting extension of time by 2 months for conducting of AGM for the Financial Year 2020-21 ended on 31/03/2021.

The extension of time by two months issued by ROC, Chennai is as below. The respective ROCs in the country have issued orders under third proviso to sub-section (1) of section 96 of the Companies Act, 2013 granting extension of time by 2 months for conducting of AGM for the Financial Year 2020-21 ended on 31/03/2021.

The Ministry of Corporate Affairs (MCA), considering requests to waive additional fee for late filing of statutory forms which fall due between 1 April and end of May owing to the COVID-19 restrictions and disruption, has granted extra time without additional fee for filing statutory forms till the end of July, 2021

The ministry of corporate affairs (MCA) has offered relaxation in certain compliance requirements for businesses, including a longer interval between two board meetings in view of the hardships during the second wave of the pandemic.

Companies are normally required to hold a minimum of four board meetings in a year with the interval between them not exceeding 120 days. This has now been relaxed by 60 days so that the interval could go up to 180 days, the ministry said in a notification issued on Monday.

The ministry also said in a separate notification that it has received several requests to waive the additional fee for late filing of statutory forms which fall due between 1 April and end of May in view of the covid-19 restrictions and disruption.

The ministry said these requests have been examined and taking into account the difficulties due to resurgence of coronavirus infections, extra time without additional fee has been granted till the end of July for filing statutory forms. In the case of filing forms to report creation or modification of a charge (lien or claim) on the assets of a company under various circumstances, the ministry has issued another notification granting relief. Accordingly, in cases where due date had expired before 1 April, extra time has been granted till end of May.

The finance ministry has already given relief for various compliance requirements related to income tax and goods and services tax (GST), besides exempting basic customs duty and agriculture cess on various medical supplies used in the prevention and treatment of coronavirus disease. The pandemic has taken a heavy toll on lives with over 222,000 deaths.

The central government has not favoured a lockdown of the country during the second wave, but several states had to impose curbs on movement and assembly of people to break the chain of infections. India has so far vaccinated over 15 crore people, or roughly 12% of the population. The second wave is expected to slow India’s economic recovery from an expected 7.7% contraction in FY21.

Clarification to be handy for India Inc as the government had recently allowed corporate India to vaccinate their employees at the companies’ premises.

In a significant boost to corporate India looking to undertake CSR around the COVID-19 pandemic, the corporate affairs ministry (MCA) has clarified spending of CSR funds for setting up “makeshift hospitals and temporary Covid care facilities” would be treated as an eligible CSR activity.

This would be permitted as an eligible Corporate Social Responsibility (CSR) activity under schedule VII of the companies Act regarding promotion of healthcare, including preventive healthcare and, disaster management respectively, the MCA said in a circular.

The MCA has said that companies may undertake the activities of setting up makeshift hospitals and temporary Covid care facilities in consultations with the State governments. This will be allowed so long as companies comply with the Companies ( CSR Policy) rules 2014 and the circulars related to CSR issued by the ministry from time to time, it added.

Handy for India Inc

This clarification from MCA may come in handy for India Inc as the government had recently allowed corporate India to vaccinate their employees at the companies’ premises without them having to go to vaccination Centres.

Recently there has been a lot of debate on whether India Inc can treat the inoculation expenses that they want to spend on behalf of their employees as an eligible CSR spend or not.

While the current thinking is that the Centre may not agree to such expenses undertaken solely for employees as being counted as CSR activity, however the latest move to allow corporates to set up makeshift hospitals and temporary Covid care facilities as an eligible CSR activity would certainly encourage India Inc to take up such activities.

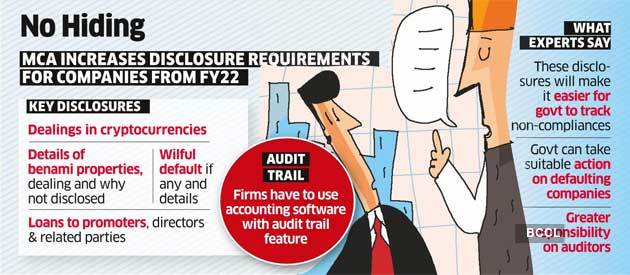

Starting April 1, companies must state if they have been declared wilful defaulters by banks, financial institutions or other lenders. The ministry also mandated companies to record audit trails of their accounts. Firms using accounting software to maintain their books need to use features that can record the audit trail of each transaction and create an edit log, including the date of such changes.

India Inc will have to declare investments in cryptocurrencies, relationships with dissolved companies and loans extended to related parties, among a host of other disclosures mandated by the government to improve transparency.

Starting April 1, companies must state if they have been declared wilful defaulters by banks, financial institutions or other lenders.

The ministry of corporate affairs announced a new set of disclosures rules under the Companies Act on Wednesday, significantly enhancing financial and general reporting requirements for companies.

The ministry also mandated companies to record audit trails of their accounts. Firms using accounting software to maintain their books need to use features that can record the audit trail of each transaction and create an edit log, including the date of such changes.

Amending the Companies (Accounts) Rules, the ministry said firms must ensure the audit trail feature on the accounting software cannot be disabled. The move is aimed at curbing backdated entries and will affect mainly smaller companies as the bigger ones already use such software, according to Shalu Kedia, a partner at Nangia & Co.

Additional disclosures to be made under schedule III of the Companies Act, 2013, relate to matters such as corporate social responsibility spending, cryptocurrency dealings, benami property, relationship with struck-off, or dissolved, companies, and ageing of payables & receivables with vendors.

These disclosures will make it easier for the government to track non-compliance and take action against defaulting companies, experts said.

“Earlier, the companies were only required to disclose trade payables and receivables, but there was no requirement to provide ageing details. This disclosure will mandate the company to disclose the ageing payment cycle for MSMEs and non-MSME vendors,” said Nischal Arora, a partner at Nangia Andersen LLP.

Dealings in cryptocurrencies must be disclosed with details of the profit or loss on such transactions, amounts of such currency held and deposits or advances from any person for trading or investing in these currencies.

“While the government is already working on a bill on cryptocurrency, the disclosure for such currency has made it clear that the government wants to gather data on cryptocurrency,” said Arora.

Another important change was related to the disclosure of any benami property holdings.

“This disclosure is another step to improve transparency for the stakeholders as they will have to disclose any proceeding that has been initiated or pending against the company for holding any benami property and also provide a reasoning and view on the same,” said Amit Maheshwari, a partner at AKM Global.

The additional disclosures will make it mandatory for companies to provide details of shortfall in CSR spending for the previous years, including reasons for not meeting targets.

Loans granted to promoters, directors and related parties that are repayable on demand or without specific repayment terms from companies must be declared in terms of amount and percentage to total loans granted.

While this will push firms to regularly service their loans, it “will be helpful for the investor and other lenders to be aware about these types of companies before making any investment or lending the money,” Maheshwari said.

The MCA has again relaxed the levy of additional fees for filing of e-forms AOC-4, AOC-4 (CFS), AOC-4, AOC-4 XBRL AOC-4 Non-XBRL till 15.03.2022 and for filing of e-forms MGT-7/MGT-7A for the financial year ended on 31.03.2021 till 31.03.2022.

The MCA has again relaxed the levy of additional fees for filing of e-forms AOC-4, AOC-4 (CFS), AOC-4, AOC-4 XBRL AOC-4 Non-XBRL till 15.03.2022 and for filing of e-forms MGT-7/MGT-7A for the financial year ended on 31.03.2021 till 31.03.2022.