Considering the difficulties faced by taxpayers in electronic filing of various audit reports under the Income Tax Act, the deadline is being extended from September 30 to October 7.

CBDT has extended the specified date of furnishing of Tax Audit Report under any provision of the Act for the Financial Year 2023-24, which was 30th September, 2024 to 07th October, 2024.

The reason behind the extension is because of difficulties faced by the taxpayers and other stakeholders in the electronic filing of various reports.

In its latest report, CBDT said, “On consideration of difficulties faced by the taxpayers and other stakeholders in electronic filing of various reports of audit under the provisions of the Income-tax Act,1961 (Act), the Central Board of Direct Taxes (CBDT), in the exercise of its powers under Section 119 of the Act, extends the specified date of furnishing of report of audit under any provision of the Act for the Previous Year 2023-24, which was 30th September, 2024 in the case of assessees referred in clause (a) of Explanation 2 to sub-section (1) of section 139 of the Act, to 071h October, 2024.”

Tax Audit involves an expression of the tax auditor’s opinion on the truth and correctness of certain factual details, furnished by the assessee to the Income Tax Authorities to enable correct assessment of total income considering all allowances, deductions, losses, adjustments, exemptions etc. and determination of tax thereon.

It is conducted to ensure proper maintenance and correctness of books of accounts by the taxpayer and certification of same by the CA. This is to discourage tax avoidance and evasion, the requirement of a tax audit that was introduced by inserting a new section 44AB in the Income Tax Act.

There are two types of forms for filing income tax audit reports namely 3CA-3CD and 3CB-3CD.

Form 3CA-3CD is applicable in case of a person who is required by or under any law to get their accounts audited; while Form 3CB-3CD is applicable in case of a person not being a person referred above i.e. where accounts are not required to be audited under any other law.

Meanwhile, rule 6G prescribes the manner of reporting and furnishing of Report of Audit of accounts to be furnished under section 44AB, which is meant for the audit of accounts of certain persons carrying on business or profession.

The GSTN has introduced a transformative feature called the IMS on the GST portal aimed at simplifying the process of correcting invoices

Through an advisory issued on September 3, 2024, the IMS is set to go live for taxpayers starting October 1, 2024, marking a significant milestone in the evolution of GST compliance procedures.

Key Features of the GST Invoice Management System (IMS)

The GST Invoice Management System (IMS) offers businesses a streamlined approach to managing their GST invoices, particularly in cases where discrepancies or amendments are necessary.

According to the GSTN advisory, “To enable taxpayers to efficiently address invoice corrections/amendments with their suppliers through the portal, a new communication process called the Invoice Management System (IMS) is being brought up at the GST portal.”

This system is designed to help businesses reconcile their GST records with those issued by their suppliers, ensuring ITC claims are compliant and accurate.

One of the standout features of IMS is that it allows taxpayers to accept, reject, or keep invoices pending before including them in their GST ITC claims.

This ensures that businesses can review the accuracy of each GST invoice and avoid potential issues during audits. The flexibility offered by the system allows businesses to defer action on GST invoices and address them in future tax periods, if necessary.

Taxpayers can update their GST invoice records anytime before filing their GSTR-3B return, a critical component in the GST compliance process.

Impact of the GST Invoice Management System on the ITC Ecosystem

The IMS is expected to significantly enhance the efficiency of ITC claims under the GST regime by providing a more structured mechanism for matching invoices between recipients and suppliers.

Since mismatches in GST invoices have been a primary source of discrepancies in ITC claims, the new system is a welcome addition.

The GSTN has long sought to introduce this level of control to minimize incorrect or fraudulent ITC claims.

Under this system, only accepted GST invoices will form part of the taxpayer’s GSTR-2B, which is the auto-populated form used to claim ITC under the GST framework.

By ensuring that only verified invoices are included in this form, businesses can significantly reduce errors in their GST returns, thus reducing the risk of disputes or penalties during audits.

Moreover, the IMS integrates seamlessly with the Quarterly Return Monthly Payment (QRMP) scheme, which allows smaller taxpayers to file GST returns quarterly while making monthly GST payments. For those enrolled in the QRMP scheme, the IMS will generate GSTR-2B on a quarterly basis, making it easier to manage GST invoices and ITC claims. This feature is particularly beneficial for small and medium-sized enterprises (SMEs), which often struggle with the administrative burden of GST compliance.

“The IMS is expected to facilitate transparency between GST recipients and suppliers and streamline the reconciliation of ITC, which has been a challenging process since the introduction of GST.”

While the full benefits of the system will become evident after its implementation, the IMS is expected to address several long-standing issues in GST compliance.

The budget features higher spending, job creation efforts, and tax relief for the middle class. Key tax changes include an increase in the Securities Transaction Tax (STT), cuts in short-term and long-term capital gains taxes, and the elimination of the angel tax. It also adjusts personal income tax slabs under the New Tax Regime.

The Union Budget for FY 2024-25, presented by Finance Minister Nirmala Sitharaman, brings several significant changes aimed at boosting the economy, simplifying tax structures, and promoting sustainable growth.

Here are the key highlights:

=====================

1. Revised Income Tax Slabs:

➤Finance Minister Nirmala Sitharaman announced a thorough review of the Income Tax Act of 1961 to benefit the middle class, expected to be completed in six months.

➤ The new tax regime includes revised tax slabs:

No tax up to Rs 3 lakh income

Rs 3 -7 lakh 5 per cent

Rs 7-10 lakh 10 per cent

Rs 10-12 lakh 15 per cent

Rs 12-15 lakh 20 per cent

Above Rs 15 lakh 30 per cent

➤ The Standard Deduction under the New Tax Regime increased from Rs 30,000 to Rs 75,000, saving Rs 17,500. The family pension deduction for pensioners rose from Rs 15,000 to Rs 25,000.

Announcements for STT, Short-term and long term capital gains:

➤ Capital gains taxation has been streamlined with short-term gains reduced to 20% and long-term gains to 12.5% for specific assets. Capital gains tax will now also apply to unlisted bonds and debentures.

➤ The Securities Transaction Tax (STT) on option sales has increased from 0.0625% to 0.1%. The STT on futures and options (securities has been raised by 0.02% and 0.1%, respectively.

➤ The indexation benefit for immovable assets, like real estate, has been removed, meaning property sellers can no longer adjust their purchase price for capital gains tax. Although the long-term capital gains (LTCG) tax on immovable properties has been reduced from 20% to 12.5%, indexation benefits are no longer available.

➤ The TDS on e-commerce transactions has been reduced from 1% to 0.1%.

➤ The angel tax has been abolished for all investors…

➤ Employer NPS deduction increased from 10% to 14%.

➤ A new solution for NPS (Central Government employees) will be developed based on a review committee’s recommendations.

➤ Assessment Rules: Reopening and reassessment rules have been relaxed. Assessments can now be reopened beyond three years only if undisclosed income exceeds Rs 50 lakh, with a maximum reopening period of five years from the end of the assessment year.

➤ Indian Professionals: Indian professionals working for multinational companies will no longer face penalties for not reporting movable foreign assets, such as ESOPs, if their value is up to Rs 20 lakh.

2. GST Updates

The budget introduces several changes to the Goods and Services Tax (GST) framework. These include waivers of interest and penalties for non-fraudulent demands from FY 2017-18 to 2019-20, provided certain conditions are met. This move aims to ease compliance and reduce the burden on businesses.

3. Fiscal Deficit and Economic Growth

The fiscal deficit is projected to reduce to 4.9% of GDP, with a commitment to further decrease it to 4.5% in the coming years. This disciplined approach is expected to enhance investor confidence and ensure sustainable economic growth.

4. Support for MSMEs and Startups

The budget allocates substantial funds to support Micro, Small, and Medium Enterprises (MSMEs) and startups. New loan schemes and financial support initiatives are introduced to foster innovation and entrepreneurship, which are crucial for job creation and economic diversification

5. Infrastructure Development

Significant investments are planned for infrastructure projects, including transportation, energy, and digital infrastructure. These projects aim to improve connectivity, reduce logistics costs, and enhance the overall business environment.

6. Agricultural Sector Boost

The agricultural sector receives a major boost with increased funding for various schemes aimed at improving productivity, ensuring fair prices for farmers, and promoting sustainable farming practices

7. Customs Duties and Capital Gains Tax

The budget also includes changes in customs duties to promote domestic manufacturing and reduce dependency on imports. Rationalization of the capital gains tax structure to simplify the tax system and encourage investments.

8. Corporate Tax:

➤ Reduction of the corporate income tax rate on foreign companies from 40 % to 35%. ➤ Introduction of measures to streamline transfer pricing assessment procedures.

9. Angel Tax and Equalization Levy:

➤ Abolition of the angel tax to support innovation and startups. ➤ Repeal of the equalization levy to simplify the tax landscape.

10. Reassessment Provisions:

➤ Simplification of reassessment provisions, allowing assessments to be reopened beyond three years, up to five years from the end of the year of assessment, only if the escaped income is more than ₹50 lakh. ➤ In search cases, the time limit for reassessment has been reduced from ten years to six years.

11. Indirect Tax Procedures:

➤ Simplification of indirect tax procedures to reduce compliance burdens and improve efficiency.

12. Vivad Se Vishwas Scheme:

➤ Introduction of the new Vivad Se Vishwas Scheme, 2024, for the settlement of pending direct tax disputes.

Conclusion

The Union Budget for FY 2024-25 reflects the government’s commitment to fostering economic growth, simplifying tax structures, and supporting key sectors. These measures are expected to create a more resilient and inclusive economy, benefiting all sections of society.

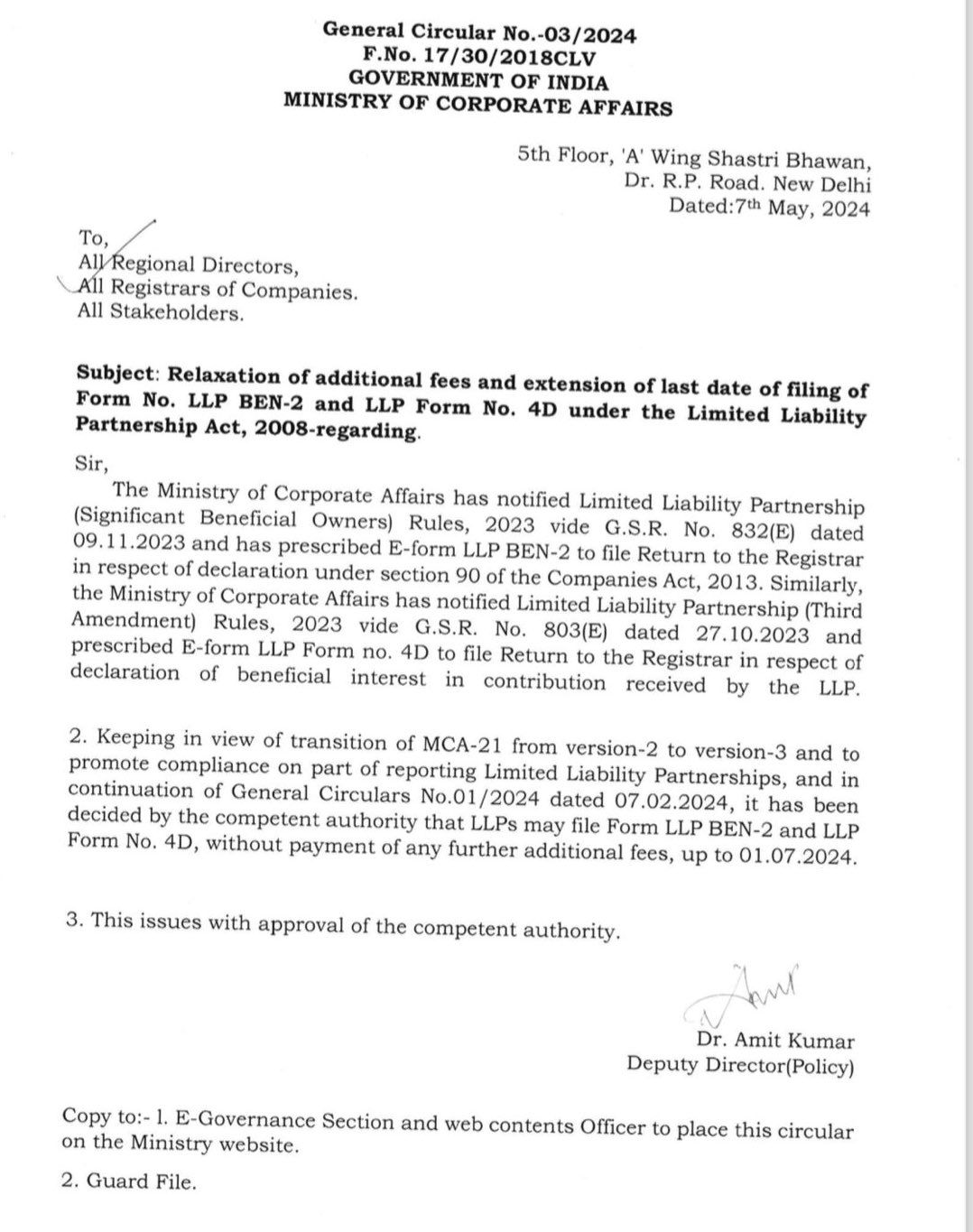

The Ministry of Corporate Affairs (MCA) has recently extended the deadline for filing Form LLP BEN-2 and LLP Form No. 4D for Limited Liability Partnerships (LLPs). Here are the details:

Background:

The MCA introduced LLP BEN-2 and LLP Form No. 4D as crucial forms for declarations under the Companies Act, 2013.

These forms relate to significant beneficial owners and beneficial interest in contributions received by the LLP.

Extension and Waiver of Additional Fees:

To facilitate compliance during the transition from MCA-21 version-2 to version-3, the MCA has extended the deadline.

LLPs now have until 1st July 2024 to submit these forms without incurring any additional fees.

This extension aims to ease the financial burden on LLPs and promote adherence to legal obligations.

Conclusion:

General Circular No.-03/2024 demonstrates the government’s commitment to supporting businesses, especially LLPs, during transitional phases.

By prioritizing ease of doing business and encouraging compliance, the MCA promotes transparency and efficiency within the corporate sector.

CBDT extends due date for filing Form 10A/10AB upto 30th June, 2024. The CBDT), has issued Circular No. 07/2024 dated 25.04.2024 further extending the due date for filing Form 10A/ Form 10AB under the Income-tax Act, 1961 (the ‘Act’) upto 30 th June, 2024.

Considering the representations received by CBDT requesting for further extension of the due date for filing such Forms, the CBDT has extended the due date of filing Form 10A/ Form 10AB until 30th June, 2024

Form 10 A – Form 10 AB –

The Central Board of Direct Taxes ( CBDT ), has issued Circular No. 07/2024 dated 25.04.2024 further extending the due date for filing Form 10A/ Form 10AB under the Income-tax Act, 1961 ( the ‘Act’ ) upto 30th June, 2024.

CBDT had earlier extended the due date for filing Form 10A/ Form 10AB by trusts, institutions and funds multiple times to mitigate genuine hardships of the taxpayers.

The last such extension was made by Circular No. 06/2023 extending the date to 30.09.2023.

Considering the representations received by CBDT requesting for further extension of due date for filing of such Forms beyond the last extended date of 30.09.2023, and to avoid genuine hardships to taxpayers,

CBDT has extended the due date of filing Form 10A/ Form 10AB up to 30th June, 2024, in respect of certain provisions of section 10(23C)/ section 12A/ section 80G/ and section 35 of the Act.

Form 10B enables a taxpayer to file an audit report if the taxpayer has applied for or is already registered as charitable or religious trust/institution by filing Form 10A. Form 10B is accessed by the CA added by the taxpayer under the My CA service and is assigned the relevant form.

It was further clarified by CBDT that, if any such existing trust, institution or fund had failed to file Form 10A for AY 2022-23 within the extended due date, and subsequently, applied for provisional registration as a new entity and received Form 10AC, can also now avail this opportunity to surrender the said Form 10AC and apply for registration for AY 2022-23 as an existing trust, institution or fund, in Form 10A till 30th June 2024.

It was also clarified that those trusts, institutions or funds whose applications for re-registration were rejected solely on the grounds of late filing or filing under the wrong section code, may also submit fresh applications in Form 10AB within the aforesaid extended deadline of 30th June 2024.

The applications as per Form 10A/ Form 10AB shall be filed electronically through the e-filing portal of the Income Tax Department.

Only 85% of the eligible donations made by a trust or institution registered under Section 12AB to another trust or institution registered under Section 12AB or approved under Section 10(23C) shall be treated as the application.

The amendment introduced in the Finance Act, 2023 has significant implications for eligible Trusts and institutions. Let’s delve into the key points:

Eligible Donations Treatment:

When an eligible Trust or institution donates to another eligible Trust or institution, the donation is considered an application for charitable or religious purposes.

However, this treatment applies only to 85% of the donated amount. The remaining 15% is not considered an application.

For example, if a Trust donates INR 100, it is treated as having applied INR 85 for charitable or religious activities.

Investment Exemption:

The 15% portion of the donation that is not considered an application does not need to be invested in specified modes under section 11(5) of the Income-tax Act (ITA).

This exemption applies because the entire INR 100 donation has been made to another Trust or institution.

Corpus Donations:

The amendment emphasizes that donations should not be towards corpus.

Corpus donations are not eligible for the 85% application treatment.

Clarity from CBDT:

The Central Board of Direct Taxes (CBDT) has clarified the computation of exemption for such donations.

The clarification reiterates the 85% application rule and provides guidance on how to handle eligible donations.

In summary, this amendment encourages donations between eligible Trusts and institutions while ensuring that the funds are primarily used for charitable or religious purposes. It streamlines the treatment of donations and exempts the 15% portion from investment requirements.

Summary of Direct and Indirect Tax Proposals: Budget 2024-25

Summary of the direct and indirect tax proposals made in the Budget 2024-25 (Finance Bill 2024) presented by Smt Nirmala Sitharaman, Union Minister of Finance and Corporate Affairs:

Highlights of the Direct Tax Proposals of Finance Bill, 2024

No changes in Tax Rates

No changes have been proposed to the existing rates of direct and indirect taxes. The existing rates of income tax, gst, import duties, etc. have been retained.

To provide continuity, some tax benefits and exemptions have been extended by 1 year until 31st March 2025. These include:

Tax benefits for startups;

Tax exemptions on certain income for International Financial Services Centers (IFSCs); and

Tax exemptions on investments made by sovereign wealth funds and pension funds.

The Interim Budget 2024 maintains the status quo on tax rates and extends certain tax breaks by a year to provide stability and continuity in taxation. No new changes or reforms have been introduced to the tax structure or rates.

Withdrawal of Outstanding direct tax demands

The FM has announced to withdraw the outstanding demands of income tax. Here is a summary of the key points regarding the withdrawal of outstanding direct tax demands announced in the Interim Budget 2024:

i) In line with the government’s vision to improve ease of living and doing business, outstanding petty direct tax demands up to Rs 25,000 dating back to 1962 will be withdrawn for the period up to FY 2009.

ii) Similarly, outstanding demands up to Rs 10,000 will be withdrawn for the FY 2010-11 to 2014-15.

iii) These are non-verified, non-reconciled or disputed demands that continue to remain on the books, causing anxiety for taxpayers.

Withdrawing these demands will help provide relief to honest taxpayers and enable refunds for subsequent years.

This is expected to benefit about 1 crore taxpayers who have such outstanding demands.

The move aims to improve tax payer services and reduce harassment of taxpayers over small disputed sums dating back decades.

In short, the Interim Budget 2024 has announced the withdrawal of old, petty direct tax demands up to Rs 25,000 till FY 2009-10 and Rs 10,000 between FY 2010-11 to 2014-15 to provide relief to taxpayers.

Highlights of the Indirect Tax Proposals of Finance Bill 2024

The FM has proposed in Budget 2024 to retain the same tax rates in respect of GST, import duty, etc.indirect taxes as are applicable at present, i.e. existing GST and import duty rates shall continue in FY 2024-25 as well.