• An employee can change the option of tax structure at the time of filing the ITR • TDS will get adjusted accordingly

The Central Board of Direct Tax (CBDT) recently came out with a circular, offering clarifications for tax-paying employees on how they can migrate to the new concessional tax regime, which was announced in this year’s Union Budget.

The lower income tax rates under the new regime came to effect from April 1, 2020. However, there were many concerns raised on how employees can choose to opt between the old and regime.

In an April 13 release, the CBDT said employees, who do not have any income from a business, can opt for the new concessional tax slabs or the old regime by intimating the deductor (employer) through a declaration form.

The declaration will also help employers determine whether to deduct TDS as per the old regime or the new concessional rates.

Employees have an option to choose between the new tax regime and the old one. Experts have already said that each employee/taxpayer may opt for any of the two, based on investments.

Coming to the new slabs under the concessional tax regime, those earning Rs 2.5 lakh will have to pay no tax while people earning Rs 2.5-5 lakh will have to pay 5 per cent tax.

Individuals in the income bracket of Rs 7.5-10 lakh will pay 15 per cent tax. People earning over Rs 10-12.5 lakh will be taxed at 20 per cent and those earning Rs 12.5-15 lakh will pay 25 per cent taxes. Finally, people earning above Rs 15 lakh will pay 30 per cent tax under the concessional tax regime.

To sum up the clarifications: 1) Employees, who do not have any income from a business, can choose to inform their employer through a declaration if they want to opt for the new tax regime for deducting tax at source on TDS from salaries.

However, employees who do not submit any declaration to the employer will continue to be charged under the old regime as earlier.

2) The IT department also clarified that an employee can change the tax structure at the time of filing income tax and that the amount of TDS will be adjusted accordingly.

“The deductor shall compute his total income, and make TDS thereon in accordance with the provisions of section IISBAC of the Act. If such intimation is not made by the employee, the employer shall make TDS without considering the provision of section 11SBAC of the Act,” the CBDT notification said.

3) Another important clarification by the tax department was related to TDS. Once employees make their intention clear to opt for the concessional rates, it will remain the same for TDS purpose for the year without any scope of modification.

“It is also clarified that the intimation so made to the deductor (employee) shall be only for the purposes of TDS during the previous year and cannot be modified during that year,” it said.

“However, the intimation would not amount to exercising an option in terms of sub-section (5) of section 115BAC of the Act and the person shall be required to do so along with the return to be furnished under sub-section (1) of section 139 of the Act for that previous year. Thus, option at the time of filing of return of income under sub-section (1) of Section 139 of the Act could be different from the intimation made by such employee to the employer for that previous year.”

The Ministry of Corporate Affairs has introduced the “Companies Fresh Start Scheme, 2020” and revised the “LLP Settlement Scheme, 2020” which is already in vogue to provide a first of its kind opportunity to both companies and LLPs to make good any filing related defaults, irrespective of the duration of default, and make a fresh start as a fully compliant entity.

The Fresh Start scheme and modified LLP Settlement Scheme provide relief to law abiding companies and the Limited Liability Partnerships (LLPs) amid COVID-19 pandemic.

One Time Opportunity

The USP of both the schemes is a one-time waiver of additional filing fees for delayed filings by the companies or LLPs with the Registrar of Companies during the currency of the Schemes, i.e. during the period starting from 1st April 2020 and ending on 30th September 2020.

Fee Payable for CFSS

Only normal fees for filing of documents in the MCA-21 registry will be payable in such case during the currency or CFSS-2020. There will not be any additional fee for any documents.

Every defaulting company shall be required to pay normal fees as prescribed under the Companies (Registration Offices and FCC) Rules, 2014 on the date of filing of each belated document and no additional fee shall be payable.

Dormant Company

The scheme gives an opportunity to inactive companies to get their companies declared as ‘dormant company’ under Section 455 of the Act by filing a simple application at a normal fee.

Details of CFSS 2020

The scheme shall come into force on the 01.04.2020 and shall remain in force till 30.09.2020

“Defaulting company” means company defined under the Companies Act, 2013, and which has made default in filing of any or the documents, statement, returns, etc including annual statutory documents on the MCA-21 registry

“Immunity certificate”‘ means the certificate referred to in subparagraph (viii) of paragraph 6 of the Scheme;

“Inactive Company” means a company as defined in Explanation (i) to sub-section (l) of section 455(1) of the Companies Act, 2013;

Applicability of CFSS 2020

Any ‘defaulting company’ is permitted to file belated documents which were due for filing on any given date in accordance with the provisions of this Scheme.

Immunity from the launch of prosecution or proceedings for imposing penalty shall be provided only to the extent such prosecution or the proceedings for imposing penalty under the Act pertain to any delay associated with the filings of belated documents.

The Ministry received much representation from the stakeholders to provide a one-time opportunity to file all the pending documents including the annual filing of the company without charging higher additional fees on any delay. The Scheme provides the above opportunity to the inactive company to convert into a dormant company under section 455 of Companies Act, 2013 by filing form MSC-1 with nominal fees & help the inactive companies to remain on ROCs register with minimum compliance requirements.

The defaulting company shall be required to file the belated documents including annual filing by paying nominal fees (without including Additional Fees) as per Companies (Registration Offices and Feel Rules, 2014) as prescribed under the Companies Act, on the date of filing of each belated document.

Both the Schemes also contain a provision for giving immunity from penal proceedings, including against imposition of penalties for late submissions and also provide additional time for filing appeals before the concerned Regional Directors against the imposition of penalties, if already imposed. However, the immunity is only against delayed filings in MCA 21 and not against any substantive violation of the law.

Application for issue of immunity under the CFSS

An application for seeking immunity in respect of belated documents can be filed under the Scheme in the Form CFSS-2020, after closure of the Scheme and after the document(s) are taken on file, or on record or approved by the Designated authority as the case may be but not after the expiry of six months from the date of closure of the Scheme. There is no fee payable on this Form.

Provided also that no immunity shall provide in case any court has ordered conviction in any matter, or an order imposing penalty has been passed by an adjudicating authority under the Act and no appeal has been preferred against such orders of the court or of the adjudicating authority.

Immunity certificate under CFSS-2020

Based on the declaration made in the Form CFS-S-2020, an immunity certificate in respect of documents filed under this Scheme shall be issued by the designated authority.

Effect of immunity

After granting the immunity, the ROC office shall withdraw the prosecution(s) and the proceedings of adjudication of penalties under section 454 of the Act, if any, in respect of defaults against which immunity has been so granted and shall be deemed to have been completed without any further action.

Any other consequential proceedings, including any proceedings involving interests of any shareholder or any other person of the company for its directors or key managerial personnel, would not be covered by such Immunity. If the company appeals against any order of prosecution for penalty passed by the competent court or adjudicating authority, then the company first needs to withdraw its application of appeal and furnish the proof of withdrawal to avail immunity in this CFSS 2020 scheme.

Scheme not to apply

This scheme shall not apply

to companies against which action for final notice for striking off the name u/s 248 of the Act (previously section 560 of Companies Act, 1956 has already been initiated by the ROC.

where any application has already been filed by the companies for action of striking off the name of the company from the register of companies;

to companies which have amalgamated under a scheme of arrangement or compromise under the Act;

where applications have already been filed for obtaining Dormant Status under section 455 of the Act before this Scheme;

to vanishing companies;

Where any increase in Authorized Capital is involved (Form SH7);

also Charge related documents (CHG-I, CHG-A. CHG-8 and CHG-9).

The defaulting inactive companies while filing documents under CFSS-2020 can simultaneously apply for the following actions :

Apply to get themselves declared as Dormant Company under section 455 of the Companies Act, 2013 by filing e-form MSC-I at a normal fee on said form; or

Apply for striking off the name of the company by filing e-Form STK-2 by paying the fee payable on form STK-2.

Infosys Nilekani gave GST Network presentation to Council.

Council ask Infosys to improve GST Network by July.

Filing to be mandatory for taxpayers over Rs 5cr of annual

turnover

Decides to extend deadline for filing of GSTR9 & GSTR9C

for FY18-19 till June 30, 2020,

GST Council to continue with 3B till September & defer the new return system.

Council defers the proposal on taxability of economic surplus of brand owners of alcohol for human consumption,

Reassures states towards payment of compensation dues,

Where Cancellation have been cancelled till March 14,

application for cancellation of revocation can be filed till March 31, 2020.

GSTR-1 to be made compulsory only for making B2B supplies,

exports & amendments

B2C & non-filers of GSTR-3B to be exempted from filing

GSTR-1

Before 10th for turnover greater than Rs 1.5 cr

Before 13th for turnover lesser than Rs 1.5 cr

GSTR-2A to be generated on 14th of every month

Council approves “Know your Supplier” Scheme

Major Reliefs:

Interest for delay in GST payment will now be charged on next cash liability under Section 50, to be applicable from July 2017

GST on mobile phones and specified parts was increased from 12% to 18%. This decision was taken to avoid difficulties due to the inverted duty structure.

All types of matches have been rationalised to a single GST rate of 12%. Till now, the handmade ones were taxed at 5% and the rest was taxed at 18%.

GST on Maintenance, Repair and Overhaul (MRO) service in respect to aircraft was reduced from 18% to 5% with full ITC.

All these rate changes will come into effect from 01 April 2020.

A new scheme called ‘Know your Supplier’ has been introduced so that the taxpayers are informed about the basic details of the suppliers with whom they transact or propose to conduct business.

Supplier can upload the Tax Invoices on real time basis in Anx-1.

Recipient can view his purchase Invoices on near real time basis.

Recipient can also view whether supplier has filed his return or not.

Supplier has to upload the Tax Invoices latest by 10th of Next Month.

However, recipient can claim ITC on missing invoices also subject to certain conditions.

In case, Invoice uploaded by the supplier in Anx-1, but RET-1 is not filed, uploading of invoices in Anx-1 will be treated as self-admitted liability and recovery proceedings will be initiated against the supplier, except in certain specified situations where recipient will be liable to pay.

Recipient has to pay the amount of ITC availed on missing invoices after specified period. (Missing invoices means, invoices not uploaded in Anx-1)

To find out missing invoices, Offline IT Tool will be provided for matching invoices in Anx-2 with invoices in the accounting system of recipient.

Payment of tax shall be discharged full at the time of filing of RET-1 or SAHAJ or SUGAM itself.

In case of Quarterly returns, tax shall be paid on monthly basis.

Recipient can do the following actions on the invoices appearing in Anx-2 (auto drafted Purchase Invoice):

Accept also called as locking

Reject (eg. Invoice not related to the recipient)

Pending

If no action is taken on a particular invoice, it will be deemed by the system as accepted and ITC will be available against these invoices.

Once invoice is accepted by the recipient, i.e., locked by the recipient, supplier cannot amend those invoices.

Locked Invoice should be unlocked by the recipient only, for making any amendment by the supplier.

Supplier will be able to issue Debit Note or Credit Note on locked invoices also. If credit/debit note is issued against any pending invoice, then system will club the credit/debit note with pending invoice.

Second set of 15 features (16-30 points) as PART-II:-

Missing invoices shall be reported in RET-1 of the current month.

System will calculate the interest automatically. Once the tax and interest is paid, the missing invoice will be clubbed with the monthly return to which it relates.

For amendments, separate Return Form is available.

Maximum 2 amendments return can be filed for any one month.

“NIL” Return can be filed by “SMS”.

Negative liability if any shall be carried forward to next month regular return.

Higher late fee for amendment return if change in liability is more than 10%

Shipping Bill details also should be entered in Anx-1 by the exporters.

If the shipping bill details are not available by the time of filing the return, the same can be entered later on also.

The export data then will be transmitted to ICEGATE portal for cross verification purposes.

Until the facility is ready to pull the data from ICEGATE portal, importers can avail ITC on imports and supplies from SEZ on self-declaration basis.

New concept of suspension of registration will be introduced. From the date of suspension till the date of cancellation, tax payer need not file returns and invoice uploading also will not be allowed.

HSN should be reported at 4 digit level in monthly return.

The tables in the return will be opened based on the profile of the tax payer.

For all return obligations offline utility tools are made available to make filing process as easy as possible.

On a day when the Economic Survey acknowledged the fact that both GST system is complex, taxpayers found it impossible to file their returns.

The Central Board of Indirect Taxes and Customs (CBIC) late on Friday night extended the due date for furnishing GST Annual Return and Reconciliation Statement (GSTR-9 / 9A and GSTR-9C) for FY 2017-18 in a staggered manner. The last date to file the Returns was January 31, 2020.

This came after thousands of taxpayers took to social media complaining about the GST portal not working. “Considering the difficulties being faced by taxpayers in filing GSTR-9 and GSTR-9C for FY 2017-18 it has been decided to extend the due dates in a staggered manner for different groups of States to 3rd, 5th and 7th February 2020 as under,” CBIC said in a Tweet.

Accordingly under Group 1, the states of Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Puducherry, Telangana, Andhra Pradesh, Other Territory has been placed and they will need to file their returns by 3rd February 2020.

Group 2 includes Jammu and Kashmir, Himachal Pradesh, Punjab, Chandigarh, Uttarakhand, Haryana, Delhi, Rajasthan and Gujarat that have to file by 5th February 2020.

Lastly group 3 includes the states of Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Andaman & Nicobar Islands, Jharkhand, Odisha, Chhattisgarh, Dadra and Nagar Haveli and Daman and Diu, Lakshadweep, Madhya Pradesh, and Uttar Pradesh, which now have to file by 7th February 2020.

On a day when the Economic Survey acknowledged the fact that both GST system is complex, taxpayers found it impossible to file their returns. By evening of January 31, #gstnfailed was the top trend on Twitter. At 10 30 pm CBIC tweeted the extension dates, but early reports suggest the portal is still not working.

The ministry further said it has also taken a note of difficulties and concerns expressed by the taxpayers regarding filing of GSTR-3B and other returns.

The Finance Ministry has announced the three due dates for filing GSTR-3B for different categories of Taxpayers.

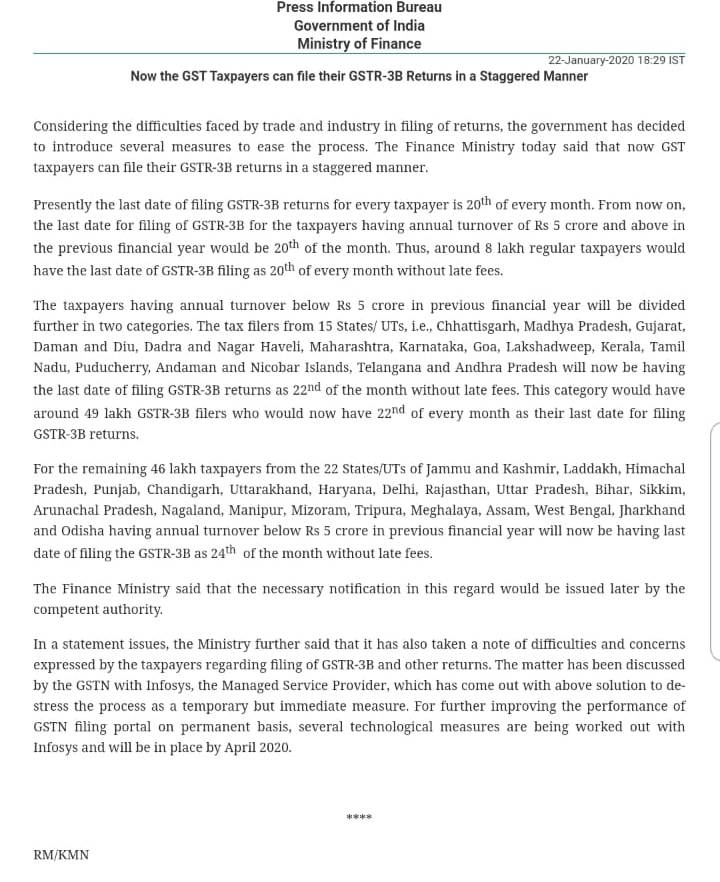

The Finance Ministry today said that now GST taxpayers can file their GSTR-3B returns in a staggered manner. Considering the difficulties faced by trade and industry in the filing of returns, the government has decided to introduce several measures to ease the process.

Presently the last date of filing GSTR-3B returns for every taxpayer is 20th of every month. From now on, the last date for filing of GSTR-3B for the taxpayers having annual turnover of Rs 5 crore and above in the previous financial year would be 20th of the month. Thus, around 8 lakh regular taxpayers would have the last date of GSTR-3B filing as 20th of every month without late fees.

The taxpayers having annual turnover below Rs 5 crore in the previous financial year will be divided further into two categories. The tax filers from 15 States/ UTs, i.e., Chhattisgarh, Madhya Pradesh, Gujarat, Daman and Diu, Dadra and Nagar Haveli, Maharashtra, Karnataka, Goa, Lakshadweep, Kerala, Tamil Nadu, Puducherry, Andaman and Nicobar Islands, Telangana and Andhra Pradesh will now be having the last date of filing GSTR-3B returns as 22nd of the month without late fees. This category would have around 49 lakh GSTR-3B filers who would now have 22nd of every month as their last date for filing GSTR-3B returns.

For the remaining 46 lakh taxpayers from the 22 States/UTs of Jammu and Kashmir, Laddakh, Himachal Pradesh, Punjab, Chandigarh, Uttarakhand, Haryana, Delhi, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand and Odisha having annual turnover below Rs 5 crore in previous financial year will now be having last date of filing the GSTR-3B as 24th of the month without late fees.

The Finance Ministry said that the necessary notification in this regard would be issued later by the competent authority.

In a statement issued, the Ministry further said that it has also taken note of difficulties and concerns expressed by the taxpayers regarding the filing of GSTR-3B and other returns. The matter has been discussed by the GSTN with Infosys, the Managed Service Provider, which has come out with the above solution to de-stress the process as a temporary but immediate measure. For further improving the performance of GSTN filing portal on a permanent basis, several technological measures are being worked out with Infosys and will be in place by April 2020.

The changes in this year’s ITR forms are significant because it is seeking more disclosures.

More disclosures are aimed at improving income tax compliances & e-assessments.

In AY 2018-19, 58.7 million returns were filed, out of which about 23.7 million people filed returns with no tax liability

While it may be commonplace in Uncle Sam’s country, India is slowly getting used to the idea of disclosing more information to the taxman. In the last five years, income tax return (ITR) forms have started asking for more details to ensure that your spending patterns match your tax return profile.

However, the department seeking details of a valid passport or foreign travel with spends of over ₹2 lakh has left many with a feeling of discomfort as it further complicates the filing process. Many experts also worry about the privacy and security issues. “Data protection law for individuals in our country is not like that in developed countries such as the US. Also, given that the Personal Data Protection Bill 2019 is under consideration, many people are worried and skeptical when it comes to divulging so much information,” said Divya Baweja, partner, Deloitte Haskins and Sells LLP, an accounting firm.

Whether asking for more information will bear fruit and result in better tax compliance continues to be a question mark. The fact remains that you need to provide additional details, for which you have to be on top of many things, including your spending patterns. Now, if you have spent more than ₹2 lakh on foreign travel or ₹1 lakh on electric bills in the current financial year (FY), you will need to furnish these details. The new ITR forms notified by Central Board of Direct Taxes (CBDT), for the upcoming assessment year (AY) 2020-21, require you to disclose such information. If your spending patterns don’t line up with your tax declarations, it may land you in hot water.

The objective is to gather more and more information and make the process of selecting cases for scrutiny easier.

New ITR Forms: ITR-1 & ITR4

ITR-1 which is also known as “Sahaj” can be used by an individual whose incomes primarily include salary income and whose total income does not exceed Rs.50 lakh during the FY. On the other hand ITR-4 can be used to file returns by resident individuals, Hindu Undivided Family (HUFs) and firms (other than LLP) having a total income of up to Rs.50 lakh from business and profession and filing return under presumptive taxation scheme.

There are two major changes in the ITR Forms – first, an individual taxpayer cannot file return either in ITR-1 or ITR4 if he is a joint-owner in house property, second, ITR-1 form is not valid for those individuals who have deposited more than Rs.1 crore in bank account or has incurred Rs2 lakh or Rs1 lakh on foreign travel or electricity respectively.

Additional info

So far, the government has notified ITR-1 and ITR-4 forms for tax filing for FY 2019-20 or AY 2020-21. However, you will have to wait to file returns as online utilities are not yet updated. The new ITR forms ask you to provide a valid passport number, if you have one; and details of your employer like name, nature of business, address and TAN.

The objective is to gather more and more information about an individual, which will help the tax department carry out specific enquries and make the process of selecting cases for scrutiny easier. “These alterations may be happening because the government is slowly moving towards e-assessments and is thus seeking greater clarification from taxpayers in the return itself to save time and costs,” said Shailesh Kumar, director, Nangia Andersen Consulting Pvt. Ltd, a business tax advisory firm.

Other experts echo the thought. “The changes reflects the continuing journey of the government towards simplification and automation. It has already started providing pre-filled return forms. These disclosures will help capture the complete details of taxpayers and the validation of their financial information, wherever such information is available from more than one source,” said Kuldip Kumar, partner and leader, personal tax, PwC, an accountancy firm.

Data is the new oil

In a computerised environment, tax returns are now filed online and data is something that the government wants to be best friends with to tackle the problem of tax evasion. At the front-end, it is seen as asking for more information from you, the tax payer. However, this isn’t the first time the ITR forms have been amended. Every year, CBDT notifies the forms carrying amendments in accordance with the Finance Act. The aim is to increase the tax base as only a tiny percentage of the population files returns. Also, among the people who file returns, about 40% show that they have no tax liability.

At the back-end, the government is taking steps to strengthen the compliance ecosystem. For instance, in 2004, as a measure to widen the tax base, the concept of Annual Information Return (AIR) filing was introduced. AIR is a statutory requirement where mutual funds, institutions issuing bonds and registrars or sub-registrars, and so on are required to record and report high-value financial transactions of individuals to the tax department.

In 2006, a project for enabling e-filing of ITR was launched. Further, in 2007, the government launched integrated taxpayer data management system (ITDMS). Under this system, data from multiple sources is collected in a complex process for drawing a complete profile of the taxpayer. A non-filers monitoring system (NMS), focusing mainly on non-filers with potential tax liabilities, was also initiated by the department. The system assimilates and analyses in-house information as well as transactional data received from various sources like ITR and AIR filed by third parties and other departments to identify people who had undertaken high value financial transactions but did not file their returns.

Taking it further, in the year 2017, the tax department initiated “project insight” to strengthen the non-intrusive information-driven approach for improving tax compliance and effectively utilizing information in tax administration. Under this project, an integrated data warehousing and business intelligence platform, which includes Income Tax Transaction Analysis Centre (INTRAC) and Compliance Management Centralized Processing Centre (CMCPC), has been set up. According to the department’s website, INTRAC leverages data analytics in tax administration and performs tasks related to data integration, compliance management, enterprise reporting and research support. CMCPC uses campaign management approach (consisting of emails, SMS, reminders, outbound calls and letters) to support voluntary compliance.

Will disclosures help?

The government wants you to divulge more information for better scrutiny. However, some experts feel that this will only increase the burden on the tax payers, who are already struggling with a very complicated system of tax filing. “This is overreach and intrusion, and it’s a wasteful exercise. For instance, many people from India go to gulf countries for labour work; if such people get notices, they won’t know how to respond. There is a lot of duplication. The department has already acquired most of this information through AIR filed by different entities,” said Himanshu Sinha, partner, Trilegal, a law firm.

While giving out more information makes things more difficult, such information will be able to trace non-filers and is intended to bring more compliances.

First 15 features (1-15 points) as PART-I:-

First 15 features (1-15 points) as PART-I:-