GST Network (GSTN), the company handling IT infrastructure for the indirect tax regime, has from October 10 started issuing refunds to exporters for Integrated GST (IGST).

Exporters can soon start claiming refunds for GST paid in August and September as GSTN will this week launch an online application for processing of refund, its Chief Executive Officer Prakash Kumar said today.

GST Network (GSTN), the company handling IT infrastructure for the indirect tax regime, has from October 10 started issuing refunds to exporters for Integrated GST (IGST) they paid for the month of July, after matching GSTR-3B and GSTR-1.

For August and September, while the initial return GSTR- 3B has already been filed, the final return GSTR-1 has not yet been filed.

“A separate online app for claiming Integrated GST (IGST) refunds for August and September would be made available on GSTN portal this week,” Kumar told .

GSTN has developed the app wherein exporters can save and upload their sales data which are part of GSTR-1 after filling up export details in Table 6A.

The table will be then extracted separately and after exporters digitally sign it, it would automatically go to the customs department.

The customs department will then validate the information provided in the table with the shipping bill data and also the taxes paid in GSTR-3B. The refund amount would be either credited to exporter’s bank account through ECS or a cheque would be issued.

As per data, 55.87 lakh GSTR-3B returns were filed for July, 51.37 lakh for August and over 42 lakh for September. Preliminary returns GSTR-3B for a month is filed on the 20th day of the next month after paying due taxes.

Thereafter, final returns in form GSTR-1, 2, 3 are filed by businesses giving invoice wise details of sales. The final return filing for August and September has not started yet.

Over July-August, an estimated Rs 67,000 crore has accumulated as the Integrated GST (IGST), of which only about Rs 5,000-10,000 crore will be due as refunds to exporters.

The Goods and Services Tax (GST), the amalgamation of over a dozen indirect taxes like excise duty and VAT, does not provide for any exemption, and so exporters are required to first pay Integrated-GST (IGST) on manufactured goods and claim refunds after exporting them. This had put severe liquidity crunch, particularly on aggregators or merchant exporters.

To ease their problems, the GST Council earlier this month decided a package for them that includes extending the Advance Authorisation / Export Promotion Capital Goods (EPCG) / 100 per cent EOU (Export Oriented Unit) schemes to sourcing inputs from abroad as well as domestic suppliers till March 31, thus not requiring to pay IGST.

The government is aiming to clear pending GST refunds of exporters by November-end. The first cheque after processing of July refunds was issued on October 10.

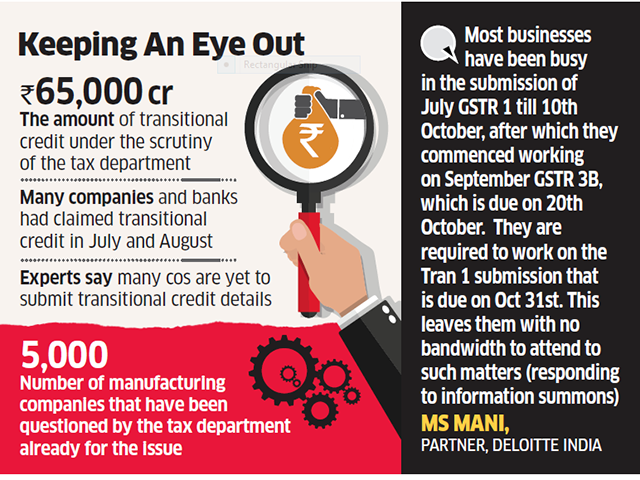

Of the total Rs 95,000 crore GST collected in July, about Rs 65,000 crore was claimed in refunds or transitional credit.

The tax department has sought explanations from banks and financial institutions, including multinationals, on transitional credit claimed by them in July under the goods and services tax (GST) regime, two people with direct knowledge of the matter said. Deputy commissioners and assistant commissioners (central tax) have issued ‘information summons’ in the last seven days seeking data in five specific areas “by e-mail/hard copy”.

These include past sales tax records; summary of closing balance of tax (as of June); description of the nature of credits; details of vendor invoices prior to July 1; and details of payments made to vendors and service providers after July 1. Transitional credit refers to tax credits on sales tax, excise and valued-added tax accumulated before July 1 on pre-GST stock.

Such credit can be set off against liabilities of the July-started GST.

Taxmen suspect some companies are misusing the provision and have filed fake returns to claim high transitional credits. Of the total Rs 95,000 crore GST collected in July, about Rs 65,000 crore was claimed in refunds or transitional credit. The move comes about two weeks after tax officers questioned manufacturing companies on transitional credit claimed by them.

ET was the first to report on September 21that about 5,000 such companies had been questioned by the taxman over transitional credit claims. For now, tax officers are only scrutinising transition credit for sales tax and excise. The data obtained from the banks and financial institutions will be examined for any discrepancies.

The firms said they haven’t been given much time to provide the information. “We had received the notice few days back and haven’t been able to submit it due to the enormity of information sought,” said the finance head of a major multinational bank. “A tax officer called me today (on Friday) and asked me to submit the required documents by Saturday.”

The finance head cited the tax officer as saying the transitional credit claimed by the bank was high. “I tried to explain that transitional credit has to be viewed in the context of our monthly tax outgo. But we will be submitting the required information nevertheless by Saturday,” he said. Experts said many companies are yet to submit transitional credit details, which has to be done through the Transform.

“Since the date for filing the Tran-1 form has been extended to October 31, it would be prudent to commence any enquiries thereafter,” said MS Mani, partner, Deloitte India. “It is advisable to consider the data submitted in the Tran-1 form and then enquire into those cases where any anomalies are detected instead of subjecting the entire data submitted by erstwhile service tax payers to any form of scrutiny.”

The pressure on tax officials increased after a letter by a senior member of the Central Board of Excise and Customs (CBEC) was sent on Wednesday to all tax commissioners. ET has seen the letter. “In view of the urgency of the matter kindly have the verification of transitional credit completed on priority (in respect of list of taxpayers forwarded on 11/9/2017) and a report on the same to be sent on this office not later than 15/10/2017,” the letter read. The letter also asked tax officers to submit a detailed analysis of transitional credit claims. This is expected to be submitted by November 3.

The Central Board of Excise and Customs had in September sent a list to all commissioners and joint commissioners that included state-wise details of companies, the GST number and transition credit amount. Tax officers had started calling all the companies whose transitional credit numbers seemed high to them.

GST Council has considered the implementation experience of the last 3 months and gave relief to small traders, says Arun jaitley.

More than three months after the Goods and Services (GST) was introduced, the GST Council made a number of big changes today, to give some relief to small and medium businesses (SMEs) on filing and payment of taxes. The panel also eased rules for exporters and cut tax rates on some items. Those businesses with annual turnover of up to Rs 1.5 crore and which constitute 90 percent of the taxpayer base but pay only 5-6 percent of overall tax, have been permitted to file quarterly income returns. “GST Council has considered the implementation experience of the last 3 months and gave relief to small traders… Compliance burden of medium and small taxpayers in GST has been reduced,” Finance Minister Arun Jaitley said. The SMEs had earlier complained of tedious compliance burden under the new regime. Below is the full text of the recommends made by GST today:

The GST Council, in its 22nd Meeting which was held today in the national capital under Chairmanship of the Union Minister of Finance and Corporate Affairs, Shri Arun Jaitley has recommended the following facilitative changes to ease the burden of compliance on small and medium businesses:

Composition Scheme

1. The composition scheme shall be made available to taxpayers having annual aggregate turnover of up to Rs. 1 crore as compared to the current turnover threshold of Rs. 75 lacs. This threshold of turnover for special category States, except Jammu & Kashmir and Uttarakhand, shall be increased to Rs. 75 lacs from Rs. 50 lacs. The turnover threshold for Jammu & Kashmir and Uttarakhand shall be Rs. 1 crore. The facility of availing composition under the increased threshold shall be available to both migrated and new taxpayers up to 31.03.2018. The option once exercised shall become operational from the first day of the month immediately succeeding the month in which the option to avail the composition scheme is exercised. New entrants to this scheme shall have to file the return in FORM GSTR-4 only for that portion of the quarter from when the scheme becomes operational and shall file returns as a normal taxpayer for the preceding tax period. The increase in the turnover threshold will make it possible for greater number of taxpayers to avail the benefit of easier compliance under the composition scheme and is expected to greatly benefit the MSME sector.

2. Persons who are otherwise eligible for composition scheme but are providing any exempt service (such as extending deposits to banks for which interest is being received) were being considered ineligible for the said scheme. It has been decided that such persons who are otherwise eligible for availing the composition scheme and are providing any exempt service, shall be eligible for the composition scheme.

3. A Group of Ministers (GoM) shall be constituted to examine measures to make the composition scheme more attractive.

Relief for Small and Medium Enterprises

4. Presently, anyone making inter-state taxable supplies, except inter-State job worker, is compulsorily required to register, irrespective of turnover. It has now been decided to exempt those service providers whose annual aggregate turnover is less than Rs. 20 lacs (Rs. 10 lacs in special category states except J & K) from obtaining registration even if they are making inter-State taxable supplies of services. This measure is expected to significantly reduce the compliance cost of small service providers.

5. To facilitate the ease of payment and return filing for small and medium businesses with annual aggregate turnover up to Rs. 1.5 crores, it has been decided that such taxpayers shall be required to file quarterly returns in FORM GSTR-1,2 & 3 and pay taxes only on a quarterly basis, starting from the Third Quarter of this Financial Year i.e. October-December, 2017. The registered buyers from such small taxpayers would be eligible to avail ITC on a monthly basis. The due dates for filing the quarterly returns for such taxpayers shall be announced in due course. Meanwhile, all taxpayers will be required to file FORM GSTR-3B on a monthly basis till December, 2017. All taxpayers are also required to file FORM GSTR-1, 2 & 3 for the months of July, August and September, 2017. Due dates for filing the returns for the month of July, 2017 have already been announced. The due dates for the months of August and September, 2017 will be announced in due course.

6. The reverse charge mechanism under sub-section (4) of section 9 of the CGST Act, 2017 and under sub-section (4) of section 5 of the IGST Act, 2017 shall be suspended till 31.03.2018 and will be reviewed by a committee of experts. This will benefit small businesses and substantially reduce compliance costs.

7. The requirement to pay GST on advances received is also proving to be burdensome for small dealers and manufacturers. In order to mitigate their inconvenience on this account, it has been decided that taxpayers having annual aggregate turnover up to Rs. 1.5 crores shall not be required to pay GST at the time of receipt of advances on account of supply of goods. The GST on such supplies shall be payable only when the supply of goods is made.

8. It has come to light that Goods Transport Agencies (GTAs) are not willing to provide services to unregistered persons. In order to remove the hardship being faced by small unregistered businesses on this account, the services provided by a GTA to an unregistered person shall be exempted from GST.

Other Facilitation Measures

9. After assessing the readiness of the trade, industry and Government departments, it has been decided that registration and operationalization of TDS/TCS provisions shall be postponed till 31.03.2018.

10. The e-way bill system shall be introduced in a staggered manner with effect from 01.01.2018 and shall be rolled out nationwide with effect from 01.04.2018. This is in order to give trade and industry more time to acclimatize itself with the GST regime.

11. The last date for filing the return in FORM GSTR-4 by a taxpayer under composition scheme for the quarter July-September, 2017 shall be extended to 15.11.2017. Also, the last date for filing the return in FORM GSTR-6 by an input service distributor for the months of July, August and September, 2017 shall be extended to 15.11.2017.

12. Invoice Rules are being modified to provide relief to certain classes of registered persons.

The goods and services tax (GST) might find use in national accounts beyond the routine application of indirect taxes in converting gross value added (GVA) into gross domestic product (GDP).

“We have started an exercise to look into this. A group comprising officials of the national accounts division is examining this issue,” TC A Anant, the government’s chief statistician, told Business Standard.

The GST, he noted, was more than a tax, since assessees file returns and describe activities on which the tax is levied, besides a whole bunch of other information. “In B2B (business-to-business) transactions, we can track the value chain. The national accounts committee is looking at it. It is at least worth probing,” Anant said. The group will check if there are legal or technical hurdles in the way. In the old taxation system as well, such filings were done in the case of value-added tax, central excise duty and service tax, but those were in separate databases. So, the system’s ability to use the data was somewhat limited.

“We had in the past conducted discussions to see if we could get more mileage from these databases. However, these remained at discussion level and not converted into outcomes,” Anant said.

There were many reasons for this. First, the process of computerisation of tax filings started around 2005-06, the service tax bit earlier and central excise a bit later. It got standardised around 2010-11.

“We started looking at it when we were doing preparatory work for base revision. Partly because of that fragmented nature, we were unable to get any mileage from it. By 2015, it became clearer that these indirect taxes would be taken over by the GST. Now, we have greater advantage as the GST covers both goods and services.”

So far as the usual use of the GST for converting GVA into GDP is concerned, Anant said it was simply a question of getting the data on the GST collection and verify how much of it is attributable to the Centre and how much to state collection. With the latter, there will be an additional bit of information, on how much was collected by specific states and the share they got from the Centre.

“This you may call a routine part of the GST database. For us, numbers are important because we use these — overall tax collections in national accounts and, similarly, specific state figures for its GSDP,” he said. Much of indirect taxes, net of subsidies, are used for converting GVA into GDP, both at current prices and at constant prices. Earlier, a panel headed by former NITI Aayog vice-chairman Arvind Panagariya had suggested using the data on the GST Network (GSTN), the levy’s information technology backbone, to assess the job market. It recommended using registration and enrolment on the GSTN as a sample for enterprise survey, to be conducted annually. So far, a little over nine million assessees have registered on the GSTN. High-frequency data, monthly or quarterly, might be conducted on the subset of the GSTN. The panel also suggested making the GSTN the universal establishment number and the income taxbased permanent account number embedded with the GSTN the universal enterprise number.

“IN B2B TRANSACTIONS, WE CAN TRACK THE VALUE CHAIN. THE NATIONAL ACCOUNTS COMMITTEE IS LOOKING AT IT. IT IS AT LEAST WORTH PROBING” TC A Anant Chief statistician

The Global Competitiveness Index (GCI) is prepared on the basis of country-level data covering 12 categories or pillars of competitiveness.

India has been ranked as the 40th most competitive economy — slipping one place from last year’s ranking — on the World Economic Forum’s global competitiveness index, which is topped by Switzerland.

On the list of 137 economies, Switzerland is followed by the US and Singapore in second and third places, respectively.

In the latest Global Competitiveness Report released today, India has slipped from the 39th position to 40th while neighbouring China is ranked at 27th.

“India stabilises this year after its big leap forward of the previous two years,” the report said, adding that the score has improved across most pillars of competitiveness. These include infrastructure (66th rank), higher education and training (75) and technological readiness (107), reflecting recent public investments in these areas, it added.

According to the report, India’s performance also improved in ICT (information and communications technologies) indicators, particularly Internet bandwidth per user, mobile phone and broadband subscriptions, and Internet access in schools.

However, the WEF said the private sector still considers corruption to be the most problematic factor for doing business in India.

“A big concern for India is the disconnect between its innovative strength (29) and its technological readiness (up 3 to 107): as long as this gap remains large, India will not be able to fully leverage its technological strengths across the wider economy,” it noted.

Among the BRICS, China and Russia (38) are placed above India.South Africa and Brazil are placed at 61st and 80th spots, respectively.

In South Asia, India has garnered the highest ranking, followed by Bhutan (85th rank), Sri Lanka (85), Nepal (88), Bangladesh (99) and Pakistan (115).

“Improving ICT infrastructure and use remain among the biggest challenges for the region: in the past decade, technological readiness stagnated the most in South Asia,” WEF said.

Other countries in the top 10 are the Netherlands (4th rank), Germany (5), Hong Kong SAR (6), Sweden (7), United Kingdom (8), Japan (9) and Finland (10).

The Global Competitiveness Index (GCI) is prepared on the basis of country-level data covering 12 categories or pillars of competitiveness.

Institutions, infrastructure, macroeconomic environment, health and primary education, higher education and training, goods market efficiency, labour market efficiency, financial market development, technological readiness, market size, business sophistication and innovation are the 12 pillars.

According to WEF’s Executive Opinion Survey 2017, corruption is the most problematic factor for doing business in India.

The second biggest bottleneck is ‘access to financing’, followed by ‘tax rates’, ‘inadequate supply of infrastructure’, ‘poor work ethics in national labour force’ and ‘inadequately educated work force’, among others.

The survey findings are mentioned in the report.

“Countries preparing for the Fourth Industrial Revolution and simultaneously strengthening their political, economic and social systems will be the winners in the competitive race of the future,” WEF founder and Executive Chairman Klaus Schwab said.

GST regime allows tax credit on stock purchased during the previous tax regime

The government on Friday said only Rs 12,000 crore of the Rs 65,000 crore of input tax credit claimed by assessees for the pre-GST stocks were valid.

The governments, both the Centre and states, had got Rs 95,000 crore of revenues from the goods and services tax (GST) for July, the first month of the indirect taxation system. But after claims of Rs 65,000 crore were made for refunds of taxes paid on stocks lying with businesses as of June 30, the government was startled, as that would have meant just Rs 30,000 crore of revenues from GST, which would be shared between the Centre and the states. The finance ministry said Rs 95,000 crore was the amount actually paid in cash, other than availing credit.

The Press Trust of India reported the government has estimated valid transitional credit claims of taxpayers in July were just Rs 12,000 crore and not Rs 65,000 crore, as previously claimed. This would give the government a short in the arm in its efforts to mop-up additional resources to perk up a subdued economy.

The GST regime allows tax credit on stock purchased during the previous tax regime. This facility is available only up to six months from the date of the GST roll-out. Even these claims could be adjusted in future months, a statement by the finance ministry suggested.

An expert explained that some of the credit available in earlier taxes would be blocked in the new regime. For instance, he said, the credit for taxes paid on purchasing vehicles were not available for businesses under the new tax unless it was a dealership or business of carrying passengers. Also, credits claimed might be under litigation and, therefore, it might not be available to the assessee to carry forward or for utilisation.

Earlier in the day, the finance ministry had issued a statement to allay concerns about high transitional credit claims, saying the Centre’s revenue kitty would not go down because of these claims. It said claims worth Rs 65,000 crore does not mean that businesses would have used all of this for payment of their output tax liability for July. In other words, the credit, which now stands reduced to Rs 12,000 crore could be utilised for future tax liability.

On how the government would stagger the adjustment, Abhishek Rastogi of Khaitan & Co cited the example of banking services. In the earlier regime, banks had to pay a centralised service tax. Under GST, they will pay state-wise tax as well. So adjusting credit for pre-GST stocks may take some time as tax liability in one centre, which used to pay earlier taxes, might not be as huge this time.

The ministry also said Rs 65,000-crore transition credit claimed was “not incredibly high” as Rs 1.27 lakh crore of credit of central excise and service tax was lying as closing balance as of June 30, 2017.

The statement said some assessees would have committed a mistake in filing the form TRAN-1 and hence, the government will allow facility of revision of TRAN-1 by the middle of October.

The GST Council has already extended by a month the date for filing TRAN-1 form till October 31.

Archit Gupta, CEO of ClearTax said while the move to extend the deadline is a good step, there would be confusion to reconcile the credit available in the old regime with the one in the GST system.

The identities of the taxpayer and his assessing officer will be hidden in a bid to check corruption and harassment assessees face at the hands of over-zealous officers.

To check corruption and harassment, the tax department will soon launch a pilot of “jurisdiction-free assessment” where a tax officer will not get to know identity of the assessee as allotment of cases will be done randomly by computers rather than on the basis of area.

The success of the pilot, to be first carried out in New Delhi and Mumbai, will determine if the plan has to be expanded all over the country, a senior revenue department official said.

The country is divided into 18 tax zones. Taxpayers are assessed by the officers of the region they are based in.

Under the new system, the assessment zones will be demolished and a special computer software will allocate a taxpayer to any officer anywhere in the country, he said.

The identities of the taxpayer and his assessing officer will be hidden in a bid to check corruption and harassment assessees face at the hands of over-zealous officers.

The tax department is working on a major reform initiative to make compliance taxpayer friendly and a 13- member committee of tax officers has been formed to look into implementation issues, the official said.

But before the country-wide launch, the pilot is being run to spot implementation issues.

“After you initiate jurisdiction-free assessment, a taxpayer might say he wants to meet the tax officer face to face and explain his case. What do we do in that case? Can we deny the taxpayer an option to meet his assessment officer (AO)? Say, we allow them to have video conferencing, then we will have to set up the facility in tax offices. These are issues we need to address,” he explained.

Among draft recommendations of a technical committee submitted to the CBDT, the apex policy-making body on income tax matters, the tax department wants to move to the jurisdiction-free I-T assessment where the taxpayer will not have to meet his assessing officer face to face.

The official also said the proposals were broadly reflected in the Prime Minister’s speech in Rajaswa Gyan Sangam earlier this month when he had said the relation between the tax department and an assessee should be that of an examiner and an examinee where either party does not know each other.

Modi, the official said, had also called for redrafting of the archaic income tax laws so that these become simpler. The humongous Income Tax Act has been in place since 1961 and the UPA government had proposed a Direct Tax Code to replace the Act.

However, since the government changed in 2014, the DTC could not be taken up.