India’s GDP amounted to $2.597 trillion at the end of last year, against $2.582 trillion for France

India has become the world’s sixth-biggest economy, pushing France into seventh place, according to updated World Bank figures for 2017. India’s gross domestic product (GDP) amounted to $2.597 trillion at the end of last year, against $2.582 trillion for France. India’s economy rebounded strongly from July 2017, after several quarters of slowdown blamed on economic policies pursued by Prime Minister Narendra Modi’s government.

India, with around 1.34 billion inhabitants, is poised to become the world’s most populous nation, whereas the French population stands at 67 million. This means that India’s per capita GDP continues to amount to just a fraction of that of France which is still roughly 20 times higher, according to World Bank figures.

Manufacturing and consumer spending were the main drivers of the Indian economy last year, after a slowdown blamed on the demonetisation of large banknotes that Modi imposed at the end of 2016, as well as a chaotic implementation of a new harmonised goods and service tax regime.

India has doubled its GDP within a decade and is expected to power ahead as a key economic engine in Asia, even as China slows down.

According to the International Monetary Fund, India is projected to generate growth of 7.4% this year and 7.8% in 2019, boosted by household spending and a tax reform. This compares to the world’s expected average growth of 3.9%.

The London-based Centre for Economics and Business Research, a consultancy, said at the end of last year that India would overtake both Britain and France this year in terms of GDP, and had a good chance to become the world’s third-biggest economy by 2032.

At the end of 2017, Britain was still the world’s fifth-biggest economy with a GDP of $2.622 trillion. The US is the world’s top economy, followed by China, Japan and Germany.

The World Bank’s biannual publication, India Development Update: India’s Growth Story, expects the economy to clock a growth rate of 6.7 per cent in the current fiscal ending March 31.

The World Bank today projected India’s GDP growth at 7.3 per cent for the next financial year and accelerate further to 7.5 per cent in 2019-20.

The World Bank’s biannual publication, India Development Update: India’s Growth Story, expects the economy to clock a growth rate of 6.7 per cent in the current fiscal ending March 31.

The report, however, observed that a growth of over 8 per cent will require “continued reform and a widening of their scope” aimed at resolving issues related to credit and investment, and enhancing competitiveness of exports.

“The Indian economy is likely to recover from the impact of demonetisation and the GST, and growth should revert slowly to a level consistent with its proximate factors — that is, to about 7.5 per cent a year,” the report said.

In November 2016, the government had scrapped high value currency notes of Rs 500 and Rs 1,000 in a bid to check black money, among others.

Later, India implemented its biggest indirect tax reform — Goods and Services Tax (GST).

Both of these initiatives had impacted the economic activities in the country in short run.

India’s economic growth had slipped to a three year low of 5.7 per cent in April-June quarter of the current fiscal, though it recovered in the subsequent quarters.

The economy is expected to grow at 6.6 per cent in the current fiscal ending March 31, as per the second advanced estimates of the Central Statistics Office (CSO), compared to 7.1 per cent in 2016-17. The earlier estimate was 6.5 per cent.

The Economic Survey tabled in Parliament has projected a growth rate of 7 to 7.5 per cent in the 2018-19 financial year.

The World Bank report further said that accelerating the growth rate will also require continued integration into global economy.

It pitches for making growth more inclusive and enhancing the effectiveness of the Indian public sector.

World Bank says India has huge potential, projects 7.3% growth

India’s growth rate in 2018 is projected to hit 7.3 per cent and 7.5 per cent in the next two years, according to the World Bank, which said the country has “enormous growth potential” compared to other emerging economies with the implementation of comprehensive reforms.

India is estimated to have grown at 6.7 per cent in 2017 despite initial setbacks from demonetisation and the Goods and Services Tax (GST), according to the 2018 Global Economics Prospect released by the World Bank here yesterday.

“In all likelihood India is going to register higher growth rate than other major emerging market economies in the next decade. So, I wouldn’t focus on the short-term numbers. I would look at the big picture for India and big picture is telling us that it has enormous potential,” Ayhan Kose, Director, Development Prospects Group at the World Bank, told PTI in an interview.

He said in comparison with China, which is slowing, the World Bank is expecting India to gradually accelerate.

“The growth numbers of the past three years were very healthy,” Kose, author of the report, said.

India’s economy is likely to grow 7.3 per cent in 2018 and then accelerate to 7.5 per cent in the next two years, the bank said.

China grew at 6.8 per cent in 2017, 0.1 per cent more than that of India, while in 2018, its growth rate is projected at 6.4 per cent. And in the next two years, the country’s growth rate will drop marginally to 6.3 and 6.2 per cent, respectively.

To materialise its potential, India, Kose said, needs to take steps to boost investment prospects.

There are measures underway to do in terms of non- performing loans and productivity, he said.

“On the productivity side, India has enormous potential with respect to secondary education completion rate. All in all, improved labour market reforms, education and health reforms as well as relaxing investment bottleneck will help improve India’s prospects,” Kose said.

India has a favourable demographic profile which is rarely seen in other economies, he said.

“In that context, improving female labour force participation rate is going to be important. Female labour force participation still remains low relative to other emerging market economies,” he said.

Reducing youth unemployment is critical, and pushing for private investment, where problems are already well-known like bank assets quality issues…If these are done, India can reach its potential easily and exceed, Kose asserted.

“In fact, we expect India to do better than its potential in 2018 and move forward,” he said.

India’s growth potential, he said would be around 7 per cent for the next 10 years.

The Indian government is “very serious” with the GST being a major turning point and banking recapitalisation programme is really important, Kose said.

“The Indian government has already recognised some of these problems and undertaking measures and willing to see the outcomes of these measures,” he said.

“India is a very large economy. It has a huge potential. At the same time, it has its own challenges. This government is very much aware of these challenges and is showing just doing its best in terms of dealing with them,” the World Bank official said.

The latest World Bank growth estimate for 2017 is 0.5 per cent, less than the previous projection, and 0.2 per cent less in the next two years.

“It is slightly lower than its previous forecast, primarily because India is undertaking major reforms,” Kose said.

These reforms, of course, will bring certain policy uncertainty, he said, “but the big issue about India, when you look at India’s growth potential and our numbers down the road 2019 and 2020, is that it is going to be the fastest growing large emerging market.”

“India has an ambitious government undertaking comprehensive reforms. The GST is a major reform to have harmonised taxes, is one nation one market one tax concept. Then, of course, the late 2016 demonetisation reform was there. The government is well aware of these short-term implications,” Kose said.

He said there might have been some temporary disruptions but “all in all” the Indian economy has done well.

“The potential growth rate of the Indian economy is very healthy to 7 per cent. I think the growth is going to be at a high rate going forward,” the World Bank official said.

In a South Asia regional press release, the World Bank said India is estimated to grow 6.7 percent in fiscal year 2017-18, slightly down from the 7.1 percent of the previous fiscal year.

This is due in part to the effects of the introduction of the Goods and Services Tax, but also to protracted balance sheet weaknesses, including corporate debt burdens and non- performing loans in the banking sector, weighing down private investment, it said.

After taking a break from buying into Indian equities in August and September, FPIs bought equities in abundance in November.

Foreign investors pumped over Rs 19,700 crore into the country’s stock markets in November, the highest in eight months, mainly due to government’s plan to recapitalise PSU banks and surge in India’s ranking in the World Bank’s ease of doing business.

In addition, such investors put in Rs 530 crore in the debt markets during the period under review.

According to depositories data, foreign portfolio investors (FPIs) invested a net amount of Rs 19,728 crore in equities last month.

This is the highest net investment by FPIs since March, when they had poured in Rs 30,906 crore in the equity market.It has been a tremendous journey for the Indian equity markets in 2017. After taking a break from buying into Indian equities in August and September, FPIs bought equities in abundance in November.

The strong inflow could be largely attributed to the government’s decision to recapitalise public-sector banks, which is expected to enhance lending and propel economic growth, said Morningstar India’s senior analyst manager (research) Himanshu Srivastava.

“This is particularly seen as a positive step after the questions have been raised from various quarters on the government’s ability to effectively implement economic reforms. Further, the slow pace of economic growth was also believed to be due to rising non performing assets (NPAs) problem in public sector banks, hence this decision provided a much-needed impetus to FPIs to again look back at Indian equity space,” he added.

Finance Minister Arun Jaitley had announced the PSU bank recapitalisation plan of Rs 2.11 trillion, out of which Rs 1.35 trillion will come from recapitalisation bonds, and the rest from markets and budgetary support.

Additionally, the news about India faring well in the World Bank’s Ease of Business index and a jump in core sector growth also turned the tide in India’s favour, Srivastava said.

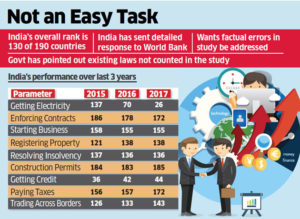

India gained 30 places in the World Bank’s ease of doing business index for 2018 to 100th among 190 nations.

“These (bank’s recapitalisation plan and world bank’s ranking) and positive developments in the recent times provided a much-needed breather to FPIs who were concerned about the short-term impact of demonetisation and goods and services tax (GST) on the domestic economy and sluggish pace of economic recovery,” he added.

Yet another positive piece of news has come from Moody’s Investor Services, which upgraded its India rating by a notch to ‘Baa2’ from ‘Baa3’ with a stable outlook, citing improved economic growth prospects driven by the government reforms.

Overall, FPIs have invested Rs 53,800 crore in equities so far in 2017 and another Rs 1.46 lakh crore in debt markets.

The World Bank’s ease of doing business report showed that eight reforms were key in helping businesses in 2016/17. India is also among the 10 economies to have improved the most, alongside El Salvador, Malawi, Nigeria and Thailand.

Doing business in India became much easier over the past one year because of a raft of policy reforms, an annual World Bank index showed on Tuesday, in what is possibly a shot in the arm for Prime Minister Narendra Modi’s efforts to win big-ticket investments.

For the first time, India jumped 30 places to break into the top 100 in the ease of doing business rankings for the year to June 2017. The 190-country index is an influential barometer of competitiveness among countries that likely also helps businesses make investment decisions.

India’s impressive performance was largely due to reforms in taxation, insolvency laws and access to credit, part of measures Prime Minister Modi’s government has pushed to boost investment and jobs that would help absorb a million people who join the workforce every month.

“India’s performance is not based on efforts of just one year but consistent efforts made over the last three years to continuously improve the regulatory environment of doing business,” Annette Dixon, vice president South Asia, told a press conference.

“It is the result of a number of reforms that the government has undertaken that India is becoming a preferred destination to do business.”

India saw improvements in six of 10 indicators, including on winning construction permits, enforcing contracts, paying taxes and resolving insolvency. It, however, slipped when it came to starting a business, getting an electricity connection, cross-border trade and registering property.

Underlining how reforms had helped India improve its overall ranking, the World Bank said the establishment of debt recovery tribunals reduced non-performing loans by 28% and lowered interest rates on larger loans, suggesting that faster processing of debt recovery cases cut the cost of credit.

India was also among the 10 economies to have improved the most, alongside El Salvador, Malawi, Nigeria and Thailand.

Jim Kim said Japan, Europe and the US along with India were growing and there was a levelling-out in developing countries.

India has been growing “pretty robustly”, World Bank President Jim Yong Kim has said as he predicted a strong global growth this year.

Speaking at the Bloomberg Global Business Forum meeting here on Wednesday, Kim also called for more cooperation among the multilateral system, private sector and the governments to take advantage of the current win-win situation.

“That dormant capital will earn a higher return, where developing countries will have access to much more capital for the infrastructure needs, even for investing in health and education, investing in resilience to climate change and other factors,” Kim said.

He said Japan, Europe and the US along with India were growing and there was a levelling-out in developing countries.

“A country like India is growing, has been growing pretty robustly. We think, Japan is growing. Europe is growing in a much more healthy way. The United States continues to grow. There is a levelling-out in developing countries,” he said, adding that the growth will be more robust this year.

In June, the World Bank predicted a 7.2 per cent growth rate for India this year against 6.8 per cent growth in 2016. India remains the fastest growing major economy in the world, the World Bank officials had said.

“It used to be that commodity importers were doing much better than commodity exporters. But that’s levelling out. So the growth is relatively more evenly distributed,” Kim said.

He said in terms of indebtedness, the bank was watching very carefully the debt-to-GDP ratios of every single country.

“In Africa, the debt-to-GDP ratios are still very manageable…We would not be moving toward providing more financing for countries if we thought there was a real problem with over indebtedness in the countries. Because we follow this very closely, along with the IMF,” he said.

“We think that there are tremendous opportunities for investment. But sometimes, purely based on perception, investors in sovereign wealth funds – I’ve heard them say, Africa is risky. Right, as if Africa was a single country.

Africa’s not a single country and the risk profiles from country to country have enormous differences,” he said.

The government expects a double-digit improvement in India’s rank in the global index on ease of doing business, likely to be announced by the World Bank next month.

A senior official told ET that the World Bank had shared its feedback, stating that it had accepted many of the reforms claimed by the government. Last year, India’s rank had improved by just one spot to 130 among 190 countries.

“The World Bank has acknowledged around 20 reforms among many more mentioned by us in response to their study … The overall ranking will depend on how other countries have performed, but we should come close to the 100 mark,” the official said.

The World Bank had recently finished gathering feedback from users for its Doing Business Report. The cut-off date for implementing reforms for the study was June 1. Reforms implemented thereafter will not be counted for this year’s ranking.

Reforms such as GST have not been taken into account as the impact is yet to be felt by users. But India is expecting these to reflect in next year’s report and significantly boost the country’s position.

India had showed one of its poorest performances on the parameter of ‘Paying Taxes’ last time, ranking 172 among the countries surveyed for the report. That, along with an equally lower position in ‘Enforcing Contracts’, landed India at the 130th spot, falling behind countries such as Mexico (38), Russia (51) and Pakistan (138). The ranking considers business environment in Delhi and Mumbai.

Over the past few months, the government has taken up concerns about not getting due credit for its reform drive with the World Bank. While responding to the survey this year, the government flagged such issues citing examples of reforms undertaken for enforcing contracts, starting business and issuing construction permits, among other things.

The government also cited provisions in the existing legal framework that deal effectively with the issue of enforcing contracts.

ET View: Push legal reforms

The way ahead is to push reforms. India fares poorly, for example, in enforcing contracts. We need judicial reforms to drastically reduce legal delays. So, even if states improve lower courts, disputes could end up in the higher judiciary and the reform lies with the Centre. The Department of Justice should drive the reforms. The need is also to enhance transparency in funding of political parties. It will weed out corruption that will automatically improve ease of doing business.