An income tax tribunal has barred auditors from issuing valuation certificates to the companies they are auditing. This is set to impact several tax disputes around valuations in companies including angel tax disputes involving start-ups.

The Bangalore Income Tax Appellate Tribunal (ITAT) said that auditors of a company cannot double up as accountants especially in situations while dealing with “share valuation for the purpose of excess share-premium taxability.”

In several cases the income tax department has disputed valuations of companies around the time of investments.

The ITAT ruling came in a case where the tax department had challenged valuation of a company by its auditor.

In most cases, valuations of startups were challenged by the tax department, leading to “angel tax.” The angel tax controversy surrounds the valuations during various rounds of startup funding. In several cases, the revenues at startups kept reducing or remained stagnant, but their valuations increased. The taxman is questioning the premiums paid by the investors and wants to categorise them as income that would be taxable at 30%. In most cases, the investments made by angel investors, venture capital funds or any other investor have been challenged by the taxman.

Many accountants and valuers are already facing heat from the tax department. ET had, on December 25, reported that the tax department has started issuing show-cause notices to valuation experts, questioning the premiums several startups fetched during their investments rounds.

Valuation experts, however, say that they merely projected and calculated future growth, using the facts and figures provided by the startups. Many tax experts point out that the tax department’s approach to the fair value as a benchmark for calculating premiums may not be accurate in the context of startups.

Income tax officers claim that the scrutiny on startups is mainly due to concerns that black money may have changed hands.

The Tribunal, while considering an appeal filed by the assessee-Company, held that the auditors of a company cannot double up as accountants especially in situations while dealing with “share valuation for the purpose of excess share-premium taxability.”

The Assessing Officer, while completing assessment against the assessee, had noted that the person who is said to have valued the share of the assessee company as on 15.11.2013 and 02.05.2014 respectively is none other than the person who has signed the Audit report under section 44AB of the Income Tax Act.

He further ignored the valuation report submitted by the assessee because the same is not as per Rule 11UA and therefore, determined the fair market value on the basis of NAV.

The Tribunal noted that the purposes of sub-rule (2) of rule 11UA, the auditor cannot be an accountant for the purposes of Rule 11UA (2).

Dismissing the appeal, the Tribunal held that “the AO has worked out the fair market value of assessee company at Rs. 714.38/- on the basis of NAV in the absence of any valuation report of any valuer who can be accepted as an Accountant as per Rule 11U(a) and taxed the excess amount of premium received by assessee over and above the permissible amount at Rs. 714.38/- per share in respect of 36957 shares and taxed the excess amount received of Rs. 1,32,29,088/- u/s. 56(2)(viib) of IT Act.

In the facts of the present case, I find no reason to interfere in the order of CIT(A) on this issue in this year also.” Before concluding, the Tribunal also held that “when an auditor cannot be accepted as an accountant for the purposes of Rule 11UA (2) read with Rule 11U(a), there is no option available to the AO but to accept the earlier report in A. Y. 2014 – 15 valuing the shares at Rs.100/- per share instead of Rs. 400/- per share as per a certificate by the auditor who cannot be accepted as an accountant for the purposes of Rule 11UA (2) read with Rule 11U(a), and adopt NAV method in A. Y. 2015 – 16.

This is very important to note that when a Chartered Accountant who can be accepted as an Accountant as per Rule 11UA (2) read with Rule 11U(a) certifies the value, the value certified as on 02.02.2012 is Rs. 100/- per share and when the auditor certifies such value on 15.11.2013 (just after 21 months approx), the value certified rises four times to Rs. 400/- per share.

These facts also suggest that such restriction as per Rule 11U(a) on the auditor’s acceptance as Accountant for the purposes of Rule 11UA (2) is well founded.”

Earlier, there were reports that the tax department has started issuing show-cause notices to valuation experts, questioning the premiums several startups fetched during their investments rounds.

The income tax (I-T) has barred all Chartered Accountants (CAs) from valuing shares of closely-held companies.

Earlier, the fair market value of unlisted equity shares was calculated at the option of the company on either the book value on the valuation date or by the discounted cash flow method. Calculated by a merchant banker or a CA.

However, the Central Board of Direct Taxes has removed the CAs from the list of authorised professionals in this regard. From Thursday, only a merchant banker may do this. This change brings this provision at par with Rule 3 of the I-T Act, which says only a merchant banker may calculate the value of unlisted shares issued under Employee Stock Ownership schemes.

Interestingly valuation of shares may still be done by CAs under the Companies Act.

So, unlisted shares or unlisted companies may be sold or valued by a CA’s valuation but, for I-T purposes, it will require a merchant banker’s valuation report.

It is expected that the government is considering a qualifying course for valuation; only those who clear it may do valuation.

India-focused funds together raised about $3.1 billion in 2017, according to Preqin data.

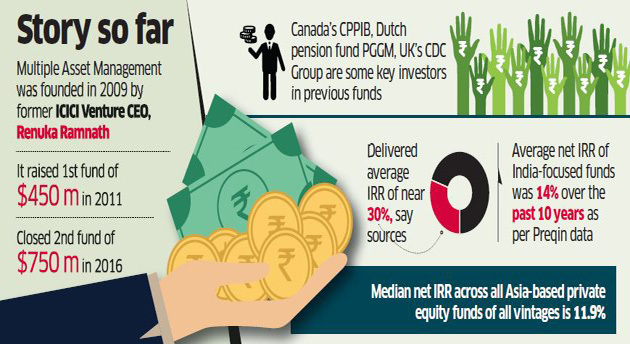

Multiples Alternate Asset Management, the private equity fund founded by former ICICI Venture CEO Renuka Ramnath, is set to raise as much as $1billion in what could be one of the largest capital-raising plans by a domestic asset manager.

The programme, which is expected to start in February, will target pension funds, sovereign wealth funds and university endowments in North America, Europe, the Middle East and South East Asia, two people with knowledge of the matter said.

The proposed fund will be equivalent to almost one-third of the capital raised by 29 India-focused private equity and venture capital funds in 2017.

The fund is being launched with appetite for long-term capital after a relative lull of almost a decade. Big-ticket asset owners such as pension and sovereign funds have started putting in money since last year, especially after Moody’s Investors Service upgraded India’s sovereign rating outlook, which lifted sentiment towards one of the fastest-growing economies.

Multiples raised its first fund of $400 million in 2011 and its second fund of $750 million in 2016. It has delivered an average internal rate of return (IRR) of 30% to investors, sources said.

The average net IRR of India-focused funds was 14% over the past 10 years, according to London-based data tracker Preqin, compared with the median net IRR of 11.9% across all Asia-based private equity funds of all vintages.

“Yes, we have already started discussions with our existing limited partners and are looking to start marketing roadshows from Febru-ary. We expect the first close by mid of this year and a final close by December,” said one of the two people.

Founded in 2009 by Ramnath, former managing director and CEO of ICICI Venture, the private equity arm of the country’s biggest private lender, ICICI Bank, Multiples manages close to $1billion assets, its website showed. It counts Canada Pension Plan Investment Board and other North American pension money managers and university endowments as its largest limited partners or investors.

These investors have already committed to the fresh fundraising. Some of the investments by Multiples include Arvind, Cholamandalam Investment & Finance, Indian Energy Exchange and RBL. Last January, the firm sold its 14% stake in India’s largest movie hall chain PVR to rival private equity fund Warburg Pincus for Rs 820 crore, making a return on more than three times on its four-year-old investment, in constant currency terms.

India-focused funds together raised about $3.1 billion in 2017, according to Preqin data. This is more than double the money raised by 18 asset managers in 2016. Last year, former Temasek India head Manish Kejriwal’s Kedaara Capital raised about $750 million for its second fund, while IDFC Alternatives raised $350 million.

PE fundraising slowed soon after the Lehman crisis with asset managers struggling to get out of their investments as valuations were rearranged, said the head of a large US fund in India. “The Moody’s upgrade and related strength seen in the economy and continued strong sentiment are expected to keep the India story intact,” he added.

In order to eliminate ambiguities and avoid litigation due to inaccurate or flawed valuation of goods and services, valuation methods have been provided by the law which act as guidelines to businesses while determining the accurate taxable value.

One of the sea changes brought about by the GST era is the way we determine the value of goods and services.

As a business, one needs to be aware of the changes in the valuation method and also how to go about valuation in some special cases, for e.g. additional charges / discounts, branch transfers (which are taxable under GST) and when a supply is made with money not being the consideration.

In order to eliminate ambiguities and avoid litigation due to inaccurate or flawed valuation of goods and services, valuation methods have been provided by the law which act as guidelines to businesses while determining the accurate taxable value.

Valuation of Taxable Supplies under GST

In the previous tax regime, different methods were adopted to determine the value of the supply, for e.g. –

a) Excise – Based on transaction value or quantity of goods or MRP

b) VAT – Based on sale value

c) Service Tax – Based on taxable value of taxable service rendered

However, in the GST regime, the value of goods and / or services supplied will solely be the transaction value, i.e. the price paid / payable at each point in the supply chain.

Additional Charges & Expenses

This may lead us to our next question – how do we account for additional charges and expenses, such as discount, packing charges etc. – under the GST regime? Should they be included or excluded from the transaction value?

Similarly, the following are some charges/expenses of supply, which are included in the transaction value –

a) Incidental expenses such as commission

b) Interest/late fee/penalty charged by supplier for delayed payment

c) Subsidies excluding those provided by the Central and State governments

d) Any tax other than GST

e) Any amount payable by supplier, but incurred by receiver

Thus, the transnational value is basis, for including or excluding the charges, in the valuation under GST.

Japanese investor SoftBank has pumped in about Rs 1,675 crore in fresh funding in Indian transportation startup Ola to give it more muscle to take American rival Uber head-on.

SoftBank subsidiary SIMI Pacific Pte picked 12,97,945 shares valued at Rs 10 at a premium of Rs 12,895 in ANI Technologies — which runs Ola — filings with the Registrar of Companies showed.

The allotment of shares was done in November last year, it added.

The latest funding, however, is believed to have come at a lower valuation.

According to sources, the move comes at a time when Softbank is working on selling Snapdeal, an e-commerce platform it invested heavily in India, to larger rival Flipkart.

The Bengaluru-based firm was aggressively looking at raising funds to compete with Uber, the world’s most valuable start-up. After selling its Chinese business to Didi last year, Uber has now set sights on India making it one of its top priorities.

Though Indian Internet companies have seen a boom in user base, their valuations have come down as investors are now focusing on path to profitability and building a sustainable business model. Flush with private equity and venture capitalist money, many start-ups continue to have high burn rate that has been a concern for investors.

Earlier this week, India’s largest e-commerce firm Flipkart raised $1.4 billion from Tencent, eBay and Microsoft in a round that saw its valuation fall from $15 billion to $11.6 billion now.

Fund raising through initial public offerings (IPOs) has crossed $2.9 billion in 2016 and another $2.9 billion is to be raised through these offerings this year, according to a research report by Baker & McKenzie.

Around 22 companies are waiting to tap the markets bringing the year-end estimated total deal value to $ 5.8 billion, more than double last year’s $2.18 billion from 71 listings, and also the highest since 2011, the report said.

The report further said that 16 companies are in the pipeline to be listed domestically in 2017, raising as much as $5.86 billion, including Vodafone’s highly anticipated $3 billion IPO, which could potentially surpass the state-run Coal India’s IPO in 2010 to become India’s biggest IPO.

The report said the momentum in India’s IPO market continues to build, boosted by the central government’s push to ease of doing business in India.

The report added that Goods & Services Tax (GST) Bill which will take effect on 1 April 2017 will have a positive effect on the market.

“The GST Bill will not only bring about the immediate benefit of widening the country’s tax base and improving the revenue productivity of domestic indirect taxes, but more importantly, it sends the message to the people of India and the rest of the world that the Indian government is committed to the country’s economic reform, further bolstering India’s attractiveness as an investment destination,” said Ashok Lalwani, head of Baker & McKenzie’s India Practice.

The report said dual listing on both the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE) of India accounted for 98.8% of Indian companies’ listings by value in 2016 year to date, raising a total of $ 2.9 billion from 19 IPOs, including ICICI Prudential Life Insurance’s $909 million IPO, which is the country’s biggest IPO this year.

A total of 33 companies are expected to dual list on both the BSE and the NSE by the end of 2016, raising a total of $4.62 billion. Improved business confidence is also driving Indian companies to look at growth and market expansion opportunities overseas by way of cross-border IPOs, the report said.

Among the 22 IPOs in the 2016 pipeline is Strand Life Sciences’ listing on NASDAQ, which if it goes ahead, will be India’s first cross-border IPO since early 2015 when Videocon d2h got listed, the report added.

In what showed a mindset shift among India’s policymakers, the government on Monday opened the floodgates for foreign direct investment (FDI) by easing the terms for nine sectors

In what showed a mindset shift among India’s policymakers, the government on Monday opened the floodgates for foreign direct investment (FDI) by easing the terms for nine sectors. Showing scant signs of legacy inhibitions, it virtually paved the way for even foreign airlines to acquire their Indian counterparts, removed the condition of domestic access to state-of-the-art technology for 100% FDI in the defence sector and put in abeyance the fractious 30% local sourcing norm for FDI in single-brand retail of advanced-technology products.

Despite the local pharma industry’s oft-expressed fear of being swamped by Big Pharma, foreign firms can now take majority (up to 74%) ownership in Indian drugmakers via the automatic route, which could again catalyse big-ticket M&A activity in the sector.

With the relaxations in the aviation sector, even a foreign airline could acquire 100% ownership in an India airline company by working in concert with a related party, according to some analysts. For example, a Qatar Airways could acquire a GoAir by directly picking up a 49% in the Indian firm and lapping up the balance equity through the West Asian nation’s sovereign wealth fund, Qatar Investment Authority.

Analysts, however, said the government seems to have tightened the sourcing rule in single-brand retailing, instead of giving a blanket exemption from such a rule for entities having “cutting-edge” technology, as was the case earlier. For instance, Apple will be exempted from the local sourcing rule for three years and have a relaxed sourcing regime for another five years if it wants to set up its own retail store, as its technology has already been described as “cutting edge” by a government panel. However, the company will still have to start local sourcing from the fourth year itself, thanks to the insistence of the finance ministry, which wanted that the Make in India programme get a boost. Similarly, Chinese company LeEco will be subjected to the same conditions if its claim of having “cutting edge” technology is endorsed by the panel headed by department of industrial policy and promotion secretary Ramesh Abhishek. However, another Chinese smartphone maker, Xiaomi, which recently withdrew its application for such a waiver, will have to comply with the mandatory 30% sourcing rule from the beginning should it wish to set up its own retail store.

Commenting on the new FDI policy for airlines, Amber Dubey, partner and India head of aerospace and defence at KPMG in India, said: “The avoidable controversies on settling ‘ownership and control’ issue is now over. Foreign airlines can now focus on the customers and competition rather than wasting time on legal and regulatory issues.”

“The likely increase in competition will bring down prices and enhance air penetration in India, both international and domestic. Indian carriers can now look for enhanced valuations in case they wish to raise funds or go for partial or complete divestment,” he added.

Calling the new norms a “bit tricky”, Amrit Pandurangi, senior director, Deloitte Touche Tohmatsu India, said, “Foreign airline investment is restricted to 49% and FDI investment in this sector has been opened up to 100%, so if the beyond the portion of the equity is by a related entity, then that needs to be tested.”

Among domestic airlines, the Rahul Bhatia-controlled Interglobe Enterprises holds close to 43% in IndiGo, Ajay Singh has a 60% stake in SpiceJet and Naresh Goyal holds 51% in Jet Airways. While Tata Sons holds 51% in both Vistara Airlines and AirAsia India, GoAir is wholly owned by the Wadia Group.

In defence, the decision to scrap the condition of access to “state-of-the-art technology” for FDI beyond 49% (through government route) will make it easier for foreign investors to invest in India. Already, Russian firm Kalashnikov is reportedly looking for local partners for manufacturing in India. Similarly, Swedish defence major Saab is learnt to be looking at more than 49% FDI in defence in its joint venture with a local partner to make the Gripen aircraft in India.

The government’s move to allow 100% FDI through the automatic route (earlier it was up to just 49%) in the broadcast carriage industry, comprising teleports, cable, direct-to-home (DTH) players, HITS (head-end-in-the sky) and mobile TV operators will provide a breather to the cable industry which has been struggling with the process of digitalisation of cable TV. The government has also allowed 74% FDI (49% under automatic route and through government approval beyond this ceiling) in private security agencies. Earlier, only 49% of FDI through government route was allowed.

Also allowed now is 100% FDI in animal husbandry (including breeding of dogs), pisciculture, aquaculture and apiculture under the automatic route under controlled conditions. It has been decided to do away with this requirement of ‘controlled conditions’ for FDI in these activities.

“For establishment of branch office, liaison office or project office or any other place of business in India if the principal business of the applicant is Defence, Telecom, Private Security or Information and Broadcasting, it has been decided that approval of Reserve Bank of India or separate security clearance would not be required in cases where FIPB approval or license/permission by the concerned Ministry/Regulator has already been granted,” a PMO statement said..

Monday’s is the second largest FDI liberalisation initiative by the Modi government, after the steps taken in November 2015. Prime Minister Narendra Modi tweeted: “In two years, Govt brings major FDI policy reforms in several key sectors… India now the most open economy in the world for FDI; most sectors under automatic approval route.” He added: “Today’s FDI reforms will give a boost to employment, job creation & benefit the economy.”

In what seemed to indicate that the government’s intention was indeed to let foreign airlines acquire Indian firms and thereby augment their capital and fleet strength for the benefit of air travellers, economic affairs secretary Shaktikanta Das said that Monday’s reforms in the sector were a “game changer”.

India’s FDI inflows increased to $55.5 billion in FY16 from $36 billion in FY14. Net FDI inflows stood at $36 billion in FY16 compared with $32.6 billion in FY15.

Commerce and industry minister Nirmala Sitharaman, however, rejected assumptions that the government decided to announce so many FDI policy reforms in one go to divert public attention from RBI governor Raghuram Rajan’s decision to not continue at the central bank after his current tenure ends on September 4. The reforms are a result of months of deliberations among various departments and are not announced in a hurry to divert attention, she affirmed.

An income tax tribunal has barred auditors from issuing valuation certificates to the companies they are auditing. This is set to impact several tax disputes around valuations in companies including angel tax disputes involving start-ups.

An income tax tribunal has barred auditors from issuing valuation certificates to the companies they are auditing. This is set to impact several tax disputes around valuations in companies including angel tax disputes involving start-ups.