The ministry further said it has also taken a note of difficulties and concerns expressed by the taxpayers regarding filing of GSTR-3B and other returns.

The Finance Ministry has announced the three due dates for filing GSTR-3B for different categories of Taxpayers.

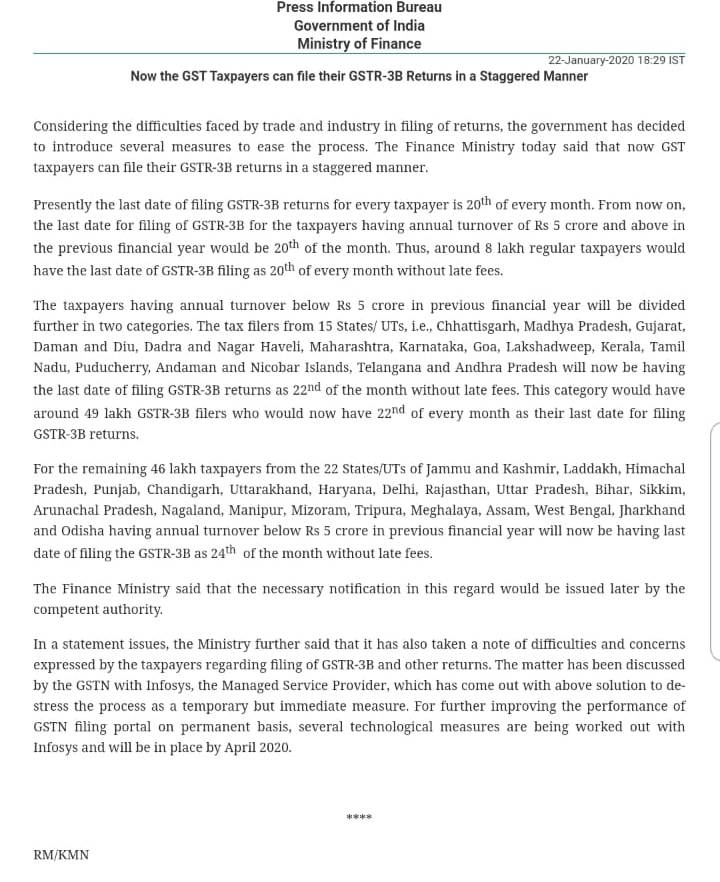

The Finance Ministry today said that now GST taxpayers can file their GSTR-3B returns in a staggered manner. Considering the difficulties faced by trade and industry in the filing of returns, the government has decided to introduce several measures to ease the process.

Presently the last date of filing GSTR-3B returns for every taxpayer is 20th of every month. From now on, the last date for filing of GSTR-3B for the taxpayers having annual turnover of Rs 5 crore and above in the previous financial year would be 20th of the month. Thus, around 8 lakh regular taxpayers would have the last date of GSTR-3B filing as 20th of every month without late fees.

The taxpayers having annual turnover below Rs 5 crore in the previous financial year will be divided further into two categories. The tax filers from 15 States/ UTs, i.e., Chhattisgarh, Madhya Pradesh, Gujarat, Daman and Diu, Dadra and Nagar Haveli, Maharashtra, Karnataka, Goa, Lakshadweep, Kerala, Tamil Nadu, Puducherry, Andaman and Nicobar Islands, Telangana and Andhra Pradesh will now be having the last date of filing GSTR-3B returns as 22nd of the month without late fees. This category would have around 49 lakh GSTR-3B filers who would now have 22nd of every month as their last date for filing GSTR-3B returns.

For the remaining 46 lakh taxpayers from the 22 States/UTs of Jammu and Kashmir, Laddakh, Himachal Pradesh, Punjab, Chandigarh, Uttarakhand, Haryana, Delhi, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand and Odisha having annual turnover below Rs 5 crore in previous financial year will now be having last date of filing the GSTR-3B as 24th of the month without late fees.

The Finance Ministry said that the necessary notification in this regard would be issued later by the competent authority.

In a statement issued, the Ministry further said that it has also taken note of difficulties and concerns expressed by the taxpayers regarding the filing of GSTR-3B and other returns. The matter has been discussed by the GSTN with Infosys, the Managed Service Provider, which has come out with the above solution to de-stress the process as a temporary but immediate measure. For further improving the performance of GSTN filing portal on a permanent basis, several technological measures are being worked out with Infosys and will be in place by April 2020.

The changes in this year’s ITR forms are significant because it is seeking more disclosures.

More disclosures are aimed at improving income tax compliances & e-assessments.

In AY 2018-19, 58.7 million returns were filed, out of which about 23.7 million people filed returns with no tax liability

While it may be commonplace in Uncle Sam’s country, India is slowly getting used to the idea of disclosing more information to the taxman. In the last five years, income tax return (ITR) forms have started asking for more details to ensure that your spending patterns match your tax return profile.

However, the department seeking details of a valid passport or foreign travel with spends of over ₹2 lakh has left many with a feeling of discomfort as it further complicates the filing process. Many experts also worry about the privacy and security issues. “Data protection law for individuals in our country is not like that in developed countries such as the US. Also, given that the Personal Data Protection Bill 2019 is under consideration, many people are worried and skeptical when it comes to divulging so much information,” said Divya Baweja, partner, Deloitte Haskins and Sells LLP, an accounting firm.

Whether asking for more information will bear fruit and result in better tax compliance continues to be a question mark. The fact remains that you need to provide additional details, for which you have to be on top of many things, including your spending patterns. Now, if you have spent more than ₹2 lakh on foreign travel or ₹1 lakh on electric bills in the current financial year (FY), you will need to furnish these details. The new ITR forms notified by Central Board of Direct Taxes (CBDT), for the upcoming assessment year (AY) 2020-21, require you to disclose such information. If your spending patterns don’t line up with your tax declarations, it may land you in hot water.

The objective is to gather more and more information and make the process of selecting cases for scrutiny easier.

New ITR Forms: ITR-1 & ITR4

ITR-1 which is also known as “Sahaj” can be used by an individual whose incomes primarily include salary income and whose total income does not exceed Rs.50 lakh during the FY. On the other hand ITR-4 can be used to file returns by resident individuals, Hindu Undivided Family (HUFs) and firms (other than LLP) having a total income of up to Rs.50 lakh from business and profession and filing return under presumptive taxation scheme.

There are two major changes in the ITR Forms – first, an individual taxpayer cannot file return either in ITR-1 or ITR4 if he is a joint-owner in house property, second, ITR-1 form is not valid for those individuals who have deposited more than Rs.1 crore in bank account or has incurred Rs2 lakh or Rs1 lakh on foreign travel or electricity respectively.

Additional info

So far, the government has notified ITR-1 and ITR-4 forms for tax filing for FY 2019-20 or AY 2020-21. However, you will have to wait to file returns as online utilities are not yet updated. The new ITR forms ask you to provide a valid passport number, if you have one; and details of your employer like name, nature of business, address and TAN.

The objective is to gather more and more information about an individual, which will help the tax department carry out specific enquries and make the process of selecting cases for scrutiny easier. “These alterations may be happening because the government is slowly moving towards e-assessments and is thus seeking greater clarification from taxpayers in the return itself to save time and costs,” said Shailesh Kumar, director, Nangia Andersen Consulting Pvt. Ltd, a business tax advisory firm.

Other experts echo the thought. “The changes reflects the continuing journey of the government towards simplification and automation. It has already started providing pre-filled return forms. These disclosures will help capture the complete details of taxpayers and the validation of their financial information, wherever such information is available from more than one source,” said Kuldip Kumar, partner and leader, personal tax, PwC, an accountancy firm.

Data is the new oil

In a computerised environment, tax returns are now filed online and data is something that the government wants to be best friends with to tackle the problem of tax evasion. At the front-end, it is seen as asking for more information from you, the tax payer. However, this isn’t the first time the ITR forms have been amended. Every year, CBDT notifies the forms carrying amendments in accordance with the Finance Act. The aim is to increase the tax base as only a tiny percentage of the population files returns. Also, among the people who file returns, about 40% show that they have no tax liability.

At the back-end, the government is taking steps to strengthen the compliance ecosystem. For instance, in 2004, as a measure to widen the tax base, the concept of Annual Information Return (AIR) filing was introduced. AIR is a statutory requirement where mutual funds, institutions issuing bonds and registrars or sub-registrars, and so on are required to record and report high-value financial transactions of individuals to the tax department.

In 2006, a project for enabling e-filing of ITR was launched. Further, in 2007, the government launched integrated taxpayer data management system (ITDMS). Under this system, data from multiple sources is collected in a complex process for drawing a complete profile of the taxpayer. A non-filers monitoring system (NMS), focusing mainly on non-filers with potential tax liabilities, was also initiated by the department. The system assimilates and analyses in-house information as well as transactional data received from various sources like ITR and AIR filed by third parties and other departments to identify people who had undertaken high value financial transactions but did not file their returns.

Taking it further, in the year 2017, the tax department initiated “project insight” to strengthen the non-intrusive information-driven approach for improving tax compliance and effectively utilizing information in tax administration. Under this project, an integrated data warehousing and business intelligence platform, which includes Income Tax Transaction Analysis Centre (INTRAC) and Compliance Management Centralized Processing Centre (CMCPC), has been set up. According to the department’s website, INTRAC leverages data analytics in tax administration and performs tasks related to data integration, compliance management, enterprise reporting and research support. CMCPC uses campaign management approach (consisting of emails, SMS, reminders, outbound calls and letters) to support voluntary compliance.

Will disclosures help?

The government wants you to divulge more information for better scrutiny. However, some experts feel that this will only increase the burden on the tax payers, who are already struggling with a very complicated system of tax filing. “This is overreach and intrusion, and it’s a wasteful exercise. For instance, many people from India go to gulf countries for labour work; if such people get notices, they won’t know how to respond. There is a lot of duplication. The department has already acquired most of this information through AIR filed by different entities,” said Himanshu Sinha, partner, Trilegal, a law firm.

While giving out more information makes things more difficult, such information will be able to trace non-filers and is intended to bring more compliances.

Changes under the GST applicable for New Year 2020

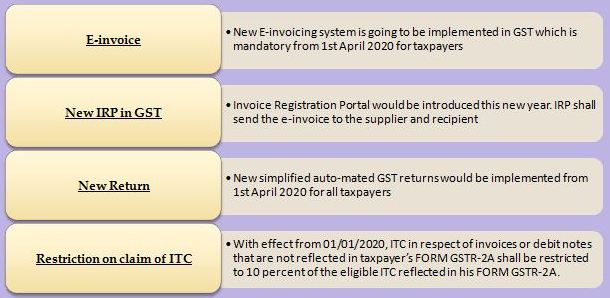

E-invoice : New E-invoicing system is going to be implemented in GST which is mandatory from 1st April 2020 for taxpayers having an annual turnover exceeding Rs. 100 crore and then gradually to all B2B suppliers in the future. A mechanism for the continuous upload of revenue invoices on a real-time basis. This is the most remarkable change coming in Indian Book Keeping.

New IRP in GST: Invoice Registration Portal would be introduced this new year. IRP shall make an e-invoice of the invoices uploaded by the supplier. IRP shall send the e-invoice to the supplier and recipient. IRP shall send e-invoices data to GSTN portal

New Return: New simplified auto-mated GST returns would be implemented from 1st April 2020 for all taxpayers. This new returns system will increase compliance and reduce tax evasion to a larger extent.

Annexure 1 and Annexure 2: Anx-1 of Outward Supplies and Anx-2 of Inward Supplies will be the future base for filing of all GST Returns, thus these 2 reports will be the key for future reports of GST which will replace GSTR 1 and GSTR-2A.

Restriction on claim of ITC: With effect from 01/01/2020, ITC in respect of invoices or debit notes that are not reflected in taxpayer’s FORM GSTR-2A shall be restricted to 10 percent of the eligible ITC reflected in his FORM GSTR-2A. Earlier the restriction was 20%. A major change in ITC availment.

E-way Bill and GSTR-1: From 11th January, 2020 non-filing of GSTR-1 for two consecutive periods would block generation of E-way Bill. Thus, regular filing of GSTR-1 and GSTR-3B in year 2020 should go hand in hand.

Waiver of late fees for Non-filing of GSTR-1: If the taxpayer has failed to file GSTR-1 from July 2017 to November 2019, then the taxpayers can file such returns till 10 January, 2020 and the late fees for the same has been waived of. This will also affect GSTR-2A of the recipient to claim ITC.

GST Audit and Annual Return: The due date for filing GST Annual Return and Audit Report for F.Y. 2017-18 has been further extended to 31st January, 2020.The due date for filing GST Annual Return and Audit Report for F.Y 2018-19 has been extended to 31st March, 2020. For F.Y 2019-20 new format may be brought in because of inherent limitations in current forms.

DIN notices and E-scrutiny: Due to decline in collection of revenue from GST, large scale e-scrutiny and e-assessment notices with DIN for the returns from July 2017 may be taken up. It would be done in order to check significant deviations in returns.

GSTN Network is proposed to be reengineered for more taxpayer-centric services like reminder of return filing, status of refund, ITC matches and mismatches, etc.

Taxpayers get one more chance to clear their tax dues.

The CBDT has extended till January 31 the last date for taxpayers to avail a “one-time” facility to apply for compounding of income tax offences, an order issued on Friday said.

The earlier deadline was December 31, 2019.

In I-T parlance, compounding means that the taxman does not file a prosecution case against the offender or tax evader in court in lieu of payment of due taxes and surcharges.

The decision to extend the last date was taken “in view of references received from field formations, including requests made by ICAI (Institute of Chartered Accountants of India) chapters wherein it has been brought to the notice of the CBDT that the taxpayers could not avail the benefit of the one-time relaxation window due to genuine hardships,” the order issued by the Central Board of Direct Taxation (CBDT) said.

The order was accessed by PTI.

Final opportunity

Hence, the order stated, the date has been extended to give a final opportunity to such taxpayers and reduce the pendency of existing prosecution cases before the courts.

Applications, as per the procedure of the scheme, are to be filed before the appropriate competent authority that is either a principal chief commissioner or a chief commissioner or a principal director general or director general of the Income-Tax Department “on or before” January 31, 2020.

The CBDT, while launching the scheme in September last year, had said that this “one-time measure” is being undertaken to mitigate unintended hardship to taxpayers in deserving cases and to reduce the pendency of existing prosecution cases before the courts.

“Cases have been brought to the notice of CBDT where the taxpayers could not apply for compounding of the offence as the compounding application was filed beyond 12 months,” it had said.

The riders

The relaxation, however, shall not be available in respect of an offence which is generally or normally not compoundable, indicating instances of serious tax evasion, financial crime, terror financing, money laundering, possession of illegal foreign assets, benami properties or conviction by a court in the past.

The CBDT circular added that application for compounding of an income tax offence can be filed in cases where: Prosecution proceedings are pending before any court of law for more than 12 months or any compounding application for an offence filed previously was withdrawn by the applicant solely for the reason that such application was filed beyond 12 months or any compounding application for an offence had been rejected previously solely for technical reasons.

The CBDT, which frames policy for the tax department, had earlier said that compounding of offences is “not a matter of right” and the department can extend such a relief only in certain cases.

This will be done keeping in view factors like “conduct of the person, the nature and magnitude of the offence on the context of the facts and circumstances of each case,” it had said.

Late fee to be waived on GSTR-1 if filed by Jan 10, 2020

The Goods and Services Tax (GST) council has decided to waive off late fees for all taxpayers who have filed GSTR 1, if all refunds are filed by 10 January 2020.

In the 38th meeting of the GST Council on December 18, authorities had also waived of a late fee to be given all taxpayers in respect of all pending Form GSTR-1 from July 2017 to November 2019, if the same is filed by January 10th, 2020.

According to CBIC, the late fee waiver will be applicable only till 10 January 2020, beyond which a late fee of at least Rs 50 per day will be charged for non-filing of GSTR-1.

The late fine can also go up to a maximum of Rs 10,000 per statement as per existing provisions. The CBIC has also said that the government has planned to take a number of steps if the pending GSTR-1 is not filed by the 10th of next month, which may include steps such as blocking of the E-way bill, etc.

GSTR-1 is a monthly return that summarizes all sales (outward supplies) of a taxpayer. The due dates for GSTR-1 are based on turnover. Businesses with sales of up to Rs. 1.5 crore will file quarterly returns. Other taxpayers with sales above Rs. 1.5 crores have to file monthly return.

Large unlisted companies may have to make quarterly or half-yearly filings, like their listed counterparts, as the government is considering amendments to the Companies Act to mandate more frequent disclosures in the aftermath of the IL&FS collapse.

The ministry of corporate affairs (MCA) is expected to prescribe a threshold for the disclosure requirement as it does not want to burden all companies, as a bulk of them are small companies, sources told TOI. The idea is to track the systemically important companies, which pose a risk to the entire system. “It will be an enabling amendment and MCA will decide on timing and extent of disclosures later,” said a source.

The assessment in the government is that there is a massive lag, often up to 18 months related to annual filings by companies, many of which have been non-compliant in the past. An entity like the beleaguered IL&FS was not on the radar till it collapsed and MCA is hoping that periodic disclosures would reduce the chances of such failures going undetected. Currently, companies are required to annually file the consolidated financial statement, balance sheet, profit & loss account, annual returns, directors’ report and certified true copy of board resolution with the designated RoC.

The proposal to increase disclosures is expected to be part of a set of amendments to be taken up by a group of ministers chaired by home minister Amit Shah, with defence minister Rajnath Singh, finance & corporate affairs minister Nirmala Sitharaman, commerce & industry minister Piyush Goyal and law & justice minister Ravi Shankar Prasad among the nine members of the committee, sources told TOI.

The ministerial panel, referred to as alternate mechanism by the Narendra Modi administration, will largely look at the recommendations of the company law panel, which submitted its report. While MCA was pushing for the introduction of the Bill during the recently concluded Winter Session, the legislation will now be placed before the Parliament as soon as it is cleared by ministers. The ministry is hoping to introduce the Bill during the budget session.

CBIC issues Standard Operation Procedure to deal with non-filers

Non-filing of GST (Goods & Services Tax) returns may lead to attachment of bank accounts and even cancellation of registrations. This is part of the Standard Operating Procedure (SOP) issued by the Finance Ministry to be followed in case of non-filing of returns.

The GST law makes it mandatory for a registered person to file returns either monthly (normal supplier) or on a quarterly basis (supplier opting for composition scheme). An ISD (Input Service Distributor) will have to file monthly returns showing details of credit distributed during the particular month.

Persons required to deduct tax (TDS) and persons required to collect tax (TCS or Tax Collected at Source) also have to file monthly returns showing the amount deducted/collected and other specified details. A non-resident taxable person also has to file returns for the period of activity.

Revenue hit

It is estimated that up to 20 per cent assessees do not file returns. This affects revenue collection. Since there is lack of clarity on how to proceed with non-filers and lack of uniformity in procedures, the Central Board of Indirect Taxes and Custom (CBIC), has come out with an SOP. Under the SOP, after the due date of return, a system-generated message or mail will be immediately shared with GST defaulters. Five days later a notice will be issued asking the GST payer to file the return or make payment within 15 days This notice is to be issued in Form GSTR 3A.

If the defaulter does not file the return within 15 days of the issue of the notice, the proper officer may proceed to assess the tax liability of the person to the best of his judgment taking into account all the material available or which he has gathered and would issue order under Rule 100 of the CGST Rules in Form GST ASMT-13.

If the defaulter files the GST return, then Form GST ASMT 13 will be deemed as withdrawn. If not, the officer may initiate recovery.

Though the above guidelines are to be followed in most cases, the SOP also prescribes that in some cases, based on facts, the Commissioner may resort to provisional attachment to protect revenue, under Section 83 of the CGST Act before issuance of Form GST ASMT-13.

If the return is not filed within the time prescribed under Section 29 of the CGST Act, then the process of cancellation may be initiated. The relevant Section prescribes conditions for cancellation of registration, and fulfilment of any of these will invite action.

These include a composition scheme assessee not filing returns for three consecutive tax periods, a non-composition assessee not furnishing returns for a continuous period of six months, not commencing business within six months of the voluntary registration, obtaining registration by fraud, and wilful misstatement or suppression of facts.

The Act clearly states that registration will not be cancelled without giving the person an opportunity of being heard.

After blocking of e-way bill generation for non-filers, issuing Standard Operating Procedure for non-filers is the next step by CBIC to ensure proper collection.