Taxpayers who have not filed GST returns for two months or quarters up to June 2021 will not be able to generate e-way bills from August 15.

The Goods and Service Tax network on 4th August 2021 has decided to resume the blocking of e-way bill generation facility on the EWB portal, for all the taxpayers in terms of Rule 138 E (a) and (b) of the CGST Rules, 2017, from 15th August onwards.

1. As you might be aware that the facility of blocking E way bill generation had been temporarily suspended due to pandemic, in terms of Rule 138 E (a) and (b) of the CGST Rules, 2017, the E Way Bill generation facility of a person is liable to be restricted, in case the person fails to file their return in Form GSTR-3B / statement in CMP-08, for a consecutive period of two months / Quarters or more.

2. The government has now decided to resume the blocking of EWB generation facility on the EWB portal, for all the taxpayers in terms of Rule 138 E (a) and (b) of the CGST Rules, 2017, from 15th August onwards.

3. Thus, after 15th August 2021, the System will check the status of returns filed in Form GSTR-3B or the statements filed in Form GST CMP-08, and restrict the generation of EWB in case of: Non filing of two or more returns in Form GSTR-3B for the months up to June, 2021 and Non filing of 02 or more statements in Form GST CMP-08 for the quarters up to April to June, 2021

4. To avail continuous EWB generation facility on EWB Portal, you are therefore advised to file your pending GSTR 3B returns/ CMP-08 Statement immediately.

5. For details of blocking and unblocking EWB click on below links :

The Ministry of Corporate Affairs (MCA), considering requests to waive additional fee for late filing of statutory forms which fall due between 1 April and end of May owing to the COVID-19 restrictions and disruption, has granted extra time without additional fee for filing statutory forms till the end of July, 2021

The ministry of corporate affairs (MCA) has offered relaxation in certain compliance requirements for businesses, including a longer interval between two board meetings in view of the hardships during the second wave of the pandemic.

Companies are normally required to hold a minimum of four board meetings in a year with the interval between them not exceeding 120 days. This has now been relaxed by 60 days so that the interval could go up to 180 days, the ministry said in a notification issued on Monday.

The ministry also said in a separate notification that it has received several requests to waive the additional fee for late filing of statutory forms which fall due between 1 April and end of May in view of the covid-19 restrictions and disruption.

The ministry said these requests have been examined and taking into account the difficulties due to resurgence of coronavirus infections, extra time without additional fee has been granted till the end of July for filing statutory forms. In the case of filing forms to report creation or modification of a charge (lien or claim) on the assets of a company under various circumstances, the ministry has issued another notification granting relief. Accordingly, in cases where due date had expired before 1 April, extra time has been granted till end of May.

The finance ministry has already given relief for various compliance requirements related to income tax and goods and services tax (GST), besides exempting basic customs duty and agriculture cess on various medical supplies used in the prevention and treatment of coronavirus disease. The pandemic has taken a heavy toll on lives with over 222,000 deaths.

The central government has not favoured a lockdown of the country during the second wave, but several states had to impose curbs on movement and assembly of people to break the chain of infections. India has so far vaccinated over 15 crore people, or roughly 12% of the population. The second wave is expected to slow India’s economic recovery from an expected 7.7% contraction in FY21.

The GST revenues during April 2021 are the highest since the introduction of GST even surpassing collections in the last month

The gross GST revenue collected in the month of April is at a record high of Rs. 1,41,384 crore of which CGST is Rs. 27,837 crore, SGST is Rs. 35,621, IGST is ₹68,481 crore (including Rs. 29,599 crore collected on import of goods) and Cess is Rs. 9,445 crore (including Rs. 981 crore collected on import of goods).

“Despite the second wave of COVID-19 pandemic affecting several parts of the country, Indian businesses have once again shown remarkable resilience by not only complying with the return filing requirements but also paying their GST dues in a timely manner during the month,” according to a statement by Ministry of Finance.

The GST revenues during April 2021 are the highest since the introduction of GST even surpassing collections in the last month (March’2021). In line with the trend of recovery in the GST revenues over past six months, the revenues for the month of April 2021 are 14% higher than the GST revenues in the last month of March’2021.

During the month, the revenues from domestic transaction (including import of services) are 21% higher than the revenues from these sources during the last month.

GST revenues have not only crossed the Rs. 1 lakh crore mark during successively for the last seven months but have also shown a steady increase. These are clear indicators of sustained economic recovery during this period.

Closer monitoring against fake-billing, deep data analytics using data from multiple sources including GST, Income-tax and Customs IT systems and effective tax administration have also contributed to the steady increase in tax revenue. Quarterly return and monthly payment scheme has been successfully implemented bringing relief to the small taxpayers as they now file only one return every three months.

Providing IT support to taxpayers in the form of pre-filled GSTR 2A and 3B returns and ramped up System capacity have also eased the return filing process.

During this month the government has settled Rs. 29,185 crore to CGST and Rs. 22,756 crore to SGST from IGST as regular settlement.

The total revenue of Centre and the States after regular and ad-hoc settlements in the month of April’ 2021 is Rs. 57,022 crore for CGST and Rs. 58,377 crore for the SGST.

SEBI made multiple relaxations for Indian firms, including market intermediaries and depositories, in terms of filing of financial details, disclosure on fund utilization and updating client records

The Securities and Exchange Board of India (SEBI), on Thursday, relaxed the deadline for listed Indian firms to announce their financial results in the wake of surging covid-19 cases in the so-called second wave of the pandemic in the country.

SEBI made multiple relaxations for Indian firms, including market intermediaries and depositories, in terms of filing of financial details, disclosure on fund utilization and updating client records.

In a circular, SEBI said listed Indian companies, which are currently required to announce their quarterly financial results within 45 days from the end of the quarter or by 15 May, 2021, are now allowed to file their March quarter results for fiscal 2021 by 30 June.

The deadline for filing annual audited financial results too has been extended by the markets regulator. Currently all companies are required to file their audited financials within 60 days from the end of the financial year, i.e. by 30 May. This deadline has been extended till 30 June, 2021 by SEBI.

“SEBI is in receipt of representations from listed entities, professional bodies, industry associations, market participants etc. requesting extension of timelines for various filings and relaxation from certain compliance obligations under the LODR (listing obligations and disclosure regulations) norms due to ongoing second wave of the CoVID-19 pandemic and restrictions imposed by various state governments,” said SEBI in its circular.

So far, 170-odd listed companies in India have announced their financial results for the March quarter and fiscal year 2021.

SEBI has also extended the deadline for companies to file their annual secretarial compliance report by a month till 30 June, 2021.

Also, the deadline for submitting the statement of deviation or variation in use of funds (along with the financial results) has been extended by a month till 30 June, 2021.

The Ministry for Corporate Affairs Ministry has hinted that the suspension of the Insolvency and Bankruptcy Code (IBC) is likely to be revoked after March 24.

he Ministry for Corporate Affairs Ministry has hinted that the suspension of the Insolvency and Bankruptcy Code (IBC) is likely to be revoked after March 24.

This has been conveyed in a written submission by the Ministry to the Standing Committee on Finance headed by Jayant Sinha. This submission came along with the note on allocation and utilisation of funds for the Insolvency and Bankruptcy Board of India (IBBI), which is the insolvency regulator.

“It is expected that the suspension of the Insolvency and Bankruptcy Code will likely be revoked after March 24 and activities of IBBI will be increased manifold in the next financial year,” the MCA submission said.

Given that the economy is now in recovery mode, it is widely expected that the Centre will revoke the suspension after March 24. Also, any extension of the suspension this date would require Parliament approval, legal experts said.

6-month suspension

A six-month suspension was first introduced in June 5 for debt defaults arising post March 25, 2020, when the Covid-induced lockdown was announced. The suspension was to end on September 25, but was extended up to December 25. In mid-December, the suspension was further extended by three months, up to March 25.

In effect, the government had ensured that any corporate debt default during Covid, between March 25, 2020 and March 25, 2021, will remain outside the IBC purview. However, for defaults before March 25, 2020, there will be no protection, said experts.

While the law protects the corporate debtor from insolvency proceedings for the one-year period till March 25, it does not disallow such action against the personal guarantors of a corporate debtor.

‘Go digital’

In a separate development, the Standing Committee on Finance has, in its latest report tabled in the Lok Sabha on Tuesday, directed the MCA to move towards full digitisation of its functions, particularly of its statutory bodies. It sees the quasi judicial bodies facing a deluge of cases post withdrawal of the moratorium and underscored stressed the need to enhance their digital and infrastructural capacities to handle the increase in caseload.

The Double Tax Avoidance Agreement (DTAA) is essentially a bilateral agreement entered into between two countries. The basic objective is to promote and foster economic trade and investment between two Countries by avoiding double taxation.

WHAT IS DOUBLE TAXATION OF INCOME?

When the same income is taxed more than once, due to levying of tax by two or more jurisdictions, on the same income asset or financial transaction, this results in double taxation. This may happen, when an assessee – an Individual or a company, is taxed more than once for the same income in India, either on the basis of place of residence or on the basis of source of accrual, which leads to double taxation.

Countries have started entering into Double Taxation Avoidance Agreements (DTAA) with other countries to resolve double taxation issue so as to ease out the tax burden of their taxpayers. This relief for taxes paid in foreign country is given to taxpayer while taxing the same income in India, which is termed as Foreign Tax Credit (FTC).

B. HOW DOUBLE TAXATION AVOIDANCE AGREEMENT (DTAA) WORKS?

In any country, the tax is levied based on 1) Source Rule and 2) the Residence Rule.

The source rule holds that income is to be taxed in the country in which it originates irrespective of whether the income accrues to a resident or a non-resident whereas the residence rule stipulates that the power to tax should rest with the country in which the taxpayer resides.

If both rules apply simultaneously to a business entity and it were to suffer tax at both ends, the cost of operating on an international business would become prohibitive and would deter the process of globalization. It is from this point of view that Double Taxation Avoidance Agreements (DTAA) have become significant.

Where the Central Government has entered into an agreement with the Government of any country outside India or specified territory outside India, for granting relief of tax, or as the case may be, avoidance of double taxation, then, in relation to the assessee to whom such agreement applies, the provisions of this Act shall apply to the extent they are more beneficial to that assessee.

Impact of Double Taxation Avoidance Agreement:

1. WHERE DTAA EXISTS (SECTION 90):

There are two methods of granting relief under Double Taxation Avoidance Agreement.

Exemption method – A particular income is taxed in one of the both countries and exempted in the other

Example- For the Income from Dividend, Interest, royalty and fees for technical services Source Rule is applicable in treaty with Greece, Libyan and United Arab Republic. So for citizen of these 3 countries if the dividend, interest, royalty or fees for technical services is arising in India, then it will be solely taxable in India only and for a resident if such income is arising in any of these 3 countries then the income will solely be taxed in these 3 countries and it will not at all be taxable in India.

Tax Credit method- The income is taxed in both the countries as per the treaty and the country of residence will allow the tax credit / reduction for the tax charged in the country of Origin.

Example- Mr. A (an Indian resident) has received salary from a US company for job in US. Since Mr. A is a resident so his global Income will be taxable in India. In this case, source country is US (since the service has been rendered in US) and resident country is India. So at the time of computation of tax liability of Mr. A, the tax paid in US will be allowed as set off against his total tax liability but limited to the tax payable on such foreign income at Indian tax rates.

Therefore DTAA determines which method to be used first and, if the income is taxable only in one country then exemption method shall be used, but if the same is taxable in both countries then tax credit method comes into play.

In case where Bilateral agreement has been entered under section 90 of the Income Tax Act, 1961 with a foreign country then the assessee has an option either to be taxed as per the Double Taxation Avoidance Agreement (hereinafter referred as “DTAA”) or as per the normal provisions of Income Tax Act 1961, whichever is more beneficial to assessee.

Example- As per DTAA between India and Germany, tax on Interest is specified @ 10% whereas under Income Tax Act 1961, it depends on slab rates for individuals & HUF and flat rates (generally 30%) for other kind of assessees (like firm, company etc). Hence, one can follow DTAA and pay tax @ 10% only.

2. WHERE DTAA DOES NOT EXIST (SECTION 91):

i. If any person who is resident in India in any previous year, in respect of income which arose outside India (and which is not deemed to accrue or arise in India), and paid in any country with which there is no agreement under section 90 for the relief or avoidance of double taxation, then he shall be entitled to the deduction from the tax payable in India,

ii. Deduction shall be lower of:

Tax calculated on such double taxed income at the Indian rates.

Tax calculated on such double taxed income at the rate of tax of the said country

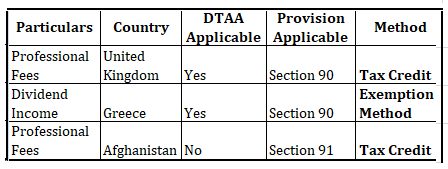

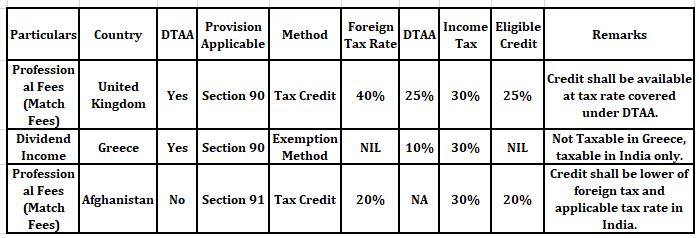

Example :Suppose Indian Sportsman, resident of India who earns foreign income in form of match fees being professional and dividend income as his other foreign income from the below mentioned countries, then in such case following provisions and method shall govern his taxability:

Therefore, both Tax Credit method u/s 90 and Section 91 deals with Foreign Tax Credit, but still having DTAA is beneficial because assessee is taxed at rate beneficial to him, which is not so in case of NO DTAA.

C. HOW CREDIT OF FOREIGN TAX IS AVAILED IN INDIA?

Rule 128 governs the credit of taxes paid on income earned in foreign country. An assessee shall be eligible to claim credit of foreign tax paid if he complies with provisions stated under Rule 128 of the Income Tax Rules which are discussed as follows:

1. Analysis of Rule 128 introduced under Indian Income Tax Rules

Applicability of the rules

The rules came into force with effect from 1.4.2017 applicable only for resident assessee for the amount of foreign taxes paid by him in a foreign country. The credit is available only if income corresponding to the taxes is offered for tax or assessed to tax in India during the year in which the credit is claimed.

In the cases where the income for which the foreign taxes paid or deducted is offered to taxes for more than one year, the credit will be given across the years in the same proportion to which the income is offered to tax in India during the year in which credit is claimed.

2. Foreign Tax Credit Defined under sub-rule 2:

i. FTC in case of DTAA countries: Taxes that are covered under the said agreement.

ii. FTC in case of other countries (No DTAA): Tax payable under the law in force in that country in the nature of income-tax referred in Section 91.

The LOWER OF tax payable under the act on such income or the foreign tax paid is eligible as FTC. However, while considering the foreign tax paid, it cannot exceed the amount arrived as per DTAA with that country.

3. Utilization of Foreign Tax Credit:

FTC is eligible for adjustment against the tax, surcharge and cess payable under the IT Act. FTC cannot be adjusted against interest, fee or penalty payable under the IT Act. FTC is not available in case foreign tax or part thereof is disputed by the assessee in any manner.

4. Exception & Conditions relating to Foreign Tax Credits:

Credit is allowed in the year in which the income is offered/assessed in India upon the assessee within six months from the end of the month in which dispute is finally settled and assessee furnishes:

Evidence of settlement of dispute

Evidence that the liability for payment of such foreign tax has been discharged and

Undertaking that no refund in respect of such amount is directly or indirectly been claimed. Further, credit for each source of income shall be calculated separately for a specific country and then aggregated. The rate of exchange to be taken for this purpose is TT buying rate on the last day of the month immediately preceding month in which the tax is paid or deducted.

5. Documents required under Foreign Tax Credit:

Furnish FORM 67 duly verified and certified by a Chartered Accountant on or before furnishing return of income u/s 139(1)

Furnishing following certificates or statement specifying:

Nature of income and,

Amount of Tax paid of which statement given by:

Tax authority of that country, or

Person responsible for deduction of such tax, or

Signed by the assessee:

In this case, it should be accompanied with – an acknowledgment of online payment or receipt or bank counterfoil for proof of payment of tax, if tax is paid by the assessee

In case of tax deduction, proof of such Tax deducted at source

D. JUDICIAL PRECEDENTS UNDER FOREIGN TAX CREDIT

1. WIPRO LIMITED F TS – 565 – HC – 2015 (KAR)

The judgment of WIPRO provides that merely because the taxpayer’s income is exempt from tax due to a limited tax holiday provided under the ITA, does not mean that foreign tax credit can be simply denied.

2. TATA SONS [2011] 43 SOT 27 (MUM AT)

Though DTAA with USA provides credit only the tax paid with the Federal Government, credit was extended to the Taxes paid to State taxes as well. It has considered the relief u/s 91 which was beneficial to the assessee than that of the DTAA.

3. VIJAY ELECTRICALS [2015] 54 COM 19 (HYD AT)

Tax credit is available even if the same is not deposited with the overseas Government in the year in which the income is taxable.

Income tax return filing due date: ITR FOR COMPANIES:- Deadline for filing income tax return for 2019-20 by companies extended by 15 days to Feb 15, 2021and for individuals by 10 days to Jan 10, 2021

In a major development, Income Tax department has extended the deadline for ITR filings. The deadline for filing income tax return for 2019-20 by companies extended by 15 days to Feb 15, 2021. Further, the deadline for filing income tax returns by individuals extended by 10 days to January 10, 2021. Also, the last date to declare under Vivad se Vishwas Scheme extended to 31st January 2021, it was expiring on December 31st.

Deadline for filing income tax return for 2019-20 by companies extended by 15 days to Feb 15, 2021 & deadline for filing income tax returns by individuals extended by 10 days to Jan 10, 2021

Taking to Twitter, Income Tax Department said, “In view of the continued challenges faced by taxpayers in meeting statutory compliances due to outbreak of COVID-19, the Govt further extends the dates for various compliances. Press release on extension of time limits issued today:”

Earlier, direct tax professionals had sought extension for tax audit report, income tax returns for audit cases and time limit for AGMs in the wake of the ongoing pandemic scenario. The Direct Taxes Professionals Association (DTPA) had urged Finance Minister Nirmala Sitharaman for extension of date of furnishing of tax audit report under section 44AB to February 28 and the due date of filing of income tax returns of assessment year 2020-21 in audit cases to March, 31, 2021.

Meanwhile, the IT department on Wednesday said more than 4.54 crore tax returns for 2019-20 fiscal have been filed till December 29. In the comparable period last year, 4.77 crore income tax returns were filed. At the close of deadline for filing ITRs without payment of late fees for fiscal 2018-19 (assessment year (AY) 2019-20), over 5.65 crore returns were filed by taxpayers.

In a tweet on Wednesday, the Income Tax department nudged taxpayers to file their ITRs by the due date. “More than 4.54 crore Income Tax Returns for AY 2020-21 have already been filed till 29th of December, 2020,” the I-T department said.

The data released by the tax department showed that over 2.52 crore ITR-1 have been filed till December 29, 2020, lower than the 2.77 crore filed till August 29, 2019.

Over 1 crore ITR-4 have been filed till December 29 as compared to 99.50 lakh filed till August 29, 2019. An analysis of the data showed that individuals filing tax return for fiscal 2019-20 have slowed so far in the current year, while filings by businesses and trusts have increased.

Returns in ITR-1 Sahaj can be filed by an ordinarily resident individual whose total income does not exceed Rs 50 lakh, while form ITR-4 Sugam is meant for resident individuals, Hindu Undivided Families (HUFs) and firms (other than LLP) having a total income of up to Rs 50 lakh and having presumptive income from business and profession.

Over 33.93 lakh ITR-2 (filed by people having income from residential property) were filed till December 29.

During last year, the due date for filing ITR by individuals who do not need to get their accounts audited was August 31. However, the date has been extended till December 31 this year on account of the COVID-19 pandemic.

ITR-5 (filed by LLP and Association of Persons) filings till December 29, 2020 jumped to 7.09 lakh from 4.14 lakh filed till August 29, 2019. ITR-6 (filed by businesses) filings skyrocketed to over 3.46 lakh till December 29, 2020 as compared to 21,962 filed till August 29, 2019.

ITR-7 (filed by persons having income derived from property held under trust) filings also jumped to over 1.04 lakh till December 29, 2020 as compared to 41,963 till August 29 last year.

Earlier, for the FY 2019-20, the government had also extended the date for making various investment/ payment for claiming deduction under Chapter-VIA-B of the IT Act which includes section 80C (LIC, PPF, NSC etc.), 80D (Mediclaim), 80G (Donations) to 31st July, 2020. Now the investment/ payment can be made upto 31st July, 2020 for claiming the deduction under these sections for FY 2019-20. In the income tax forms, Schedule DI enables taxpayers to claim exemptions on investments they made during the extended period, until June 30, 2020.

Under normal circumstances, the last date to take income tax benefits is till March 31 of the financial year. The government had also extended the last date for the issuance of Form 16 by employers to their employees. In fact, the extension has been given for all TDS ( tax deducted at source) certificates, including Form 16. The CBDT has already notified the Income Tax Return Forms for the assessment year (AY) 2020-21 and are available for e-Filing by downloading either excel or Java utility.