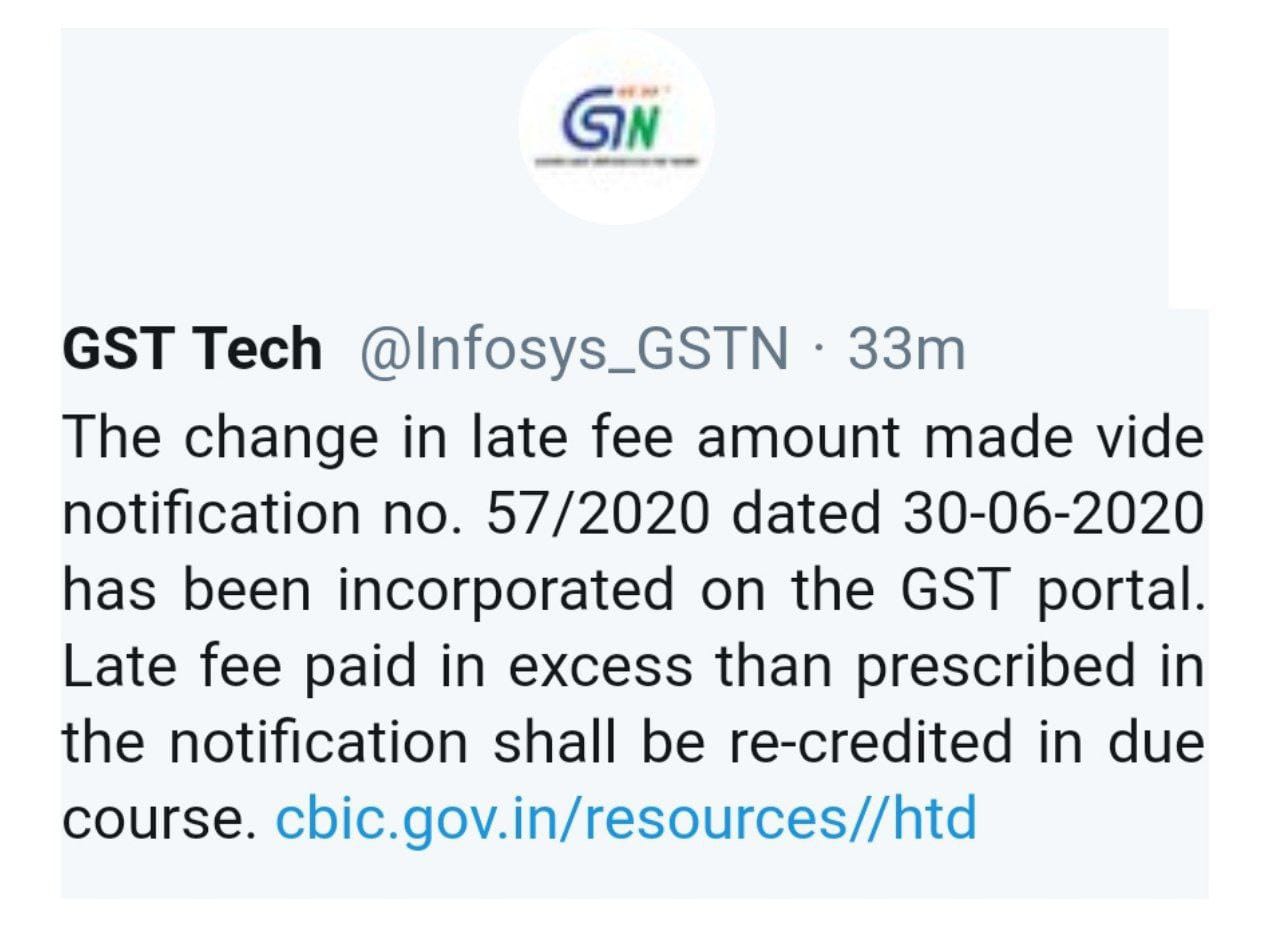

CBIC had vide Noti 57/2020 has stated that that maximum Late Fee for Form GSTR 3B has been capped at Rs. 500 for tax period July 2017 to July 2020 subject to returns being filed before 30th September 2020.

But portal was not updated and it has levied late fees as per old calculation. Hence, GSTN Tech twitter posted that “The change in late fee amount made vide notification no. 57/2020 dated 30-06-2020 has been incorporated on the GST portal.

Late fee paid in excess than prescribed in the notification shall be re-credited in due course.”

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)]

Government of India

Ministry of Finance

(Department of Revenue)

Central Board of Indirect Taxes and Customs

Notification No. 57/2020 – Central Tax

New Delhi, the 30th June, 2020

G.S.R…..(E).— In exercise of the powers conferred by section 128 of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereafter in this notification referred to as the said Act), read with section 148 of the said Act, the Government, on the recommendations of the Council, hereby makes the following further amendments in the notification of the Government of India in the Ministry of Finance (Department of Revenue), No. 76/2018– Central Tax, dated the 31st December, 2018, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub- section (i) vide number G.S.R. 1253(E), dated the 31st December, 2018, namely :–

In the said notification, after the third proviso, the following provisos shall be inserted, namely: –

“Provided also that for the class of registered persons mentioned in column (2) of the Table of the above proviso, who fail to furnish the returns for the tax period as specified in column (3) of the said Table, according to the condition mentioned in the corresponding entry in column (4) of the said Table, but furnishes the said return till the 30th day of September, 2020, the total amount of late fee payable under section 47 of the said Act, shall stand waived which is in excess of two hundred and fifty rupees and shall stand fully waived for those taxpayers where the total amount of central tax payable in the said return is nil:

Provided also that for the taxpayers having an aggregate turnover of more than rupees 5 crores in the preceding financial year, who fail to furnish the return in FORM GSTR-3B for the months of May, 2020 to July, 2020, by the due date but furnish the said return till the 30th day of September, 2020, the total amount of late fee under section 47 of the said Act, shall stand waived which is in excess of two hundred and fifty rupees and shall stand fully waived for those taxpayers where the total amount of central tax payable in the said return is nil.”.

2. This notification shall be deemed to have come into effect from the 25th day of June, 2020.

[F. No. CBEC-20/06/08/2020-GST]

(Pramod Kumar)

Director, Government of India

Note: The principal notification No. 76/2018-Central Tax, dated 31st December, 2018 was published in the Gazette of India, Extraordinary, vide number G.S.R. 1253(E), dated the 31st December, 2018 and was last amended vide notification number 52/2020 – Central Tax, dated the 24th June, 2020, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i) vide number G.S.R.405 (E), dated the 24th June, 2020.

First 15 features (1-15 points) as PART-I:-

First 15 features (1-15 points) as PART-I:-