The government extended the date for filing income tax returns for companies by one month to November 30.

Income Tax Department has extended the deadline for ITR filing for certain categories of taxpayers. This has brought great relief to the taxpayers/institutions falling in these categories and they have also been saved from paying heavy penalties due to delay.

According to the Income Tax Department, till September 5, about 6.98 crore individual taxpayers have filed ITR.

The Income Tax Department has extended the deadline for filing income tax returns for charitable trusts, religious institutions and professional bodies by one month to November 30. The Income Tax Department said in a statement that the due date for filing income tax return in Form ITR-7 for the assessment year 2023-24, which is 31 October 2023, has been extended to 30 November 2023.

Also, the due date for submission of audit report for 2022-23 by any fund, trust, institution or any university or educational institution or medical institution in Form 10B/10BB has been extended by one month to 31 October 2023. Earlier the last date for submission of audit report was 30 September.

ITR-7 is filed by institutions involved in charitable and religious activities, research institutes, professional bodies, political parties and electoral trusts also file tax returns through ITR-7.

The Finance Ministry said in a statement on Monday, the deadline for filing income tax return in Form ITR-7 for the assessment year 2023-24 has been extended from October 31, 2023 to November 30, 2023.

In the current financial year, till mid-September, net direct tax collection has increased by 23.51% to Rs 8.65 lakh crore. The Finance Ministry said that there has been a huge increase in direct tax collection due to more advance tax payment by the companies. During this period, advance tax payment has increased by 21%.

According to the data, net tax collection has been 47.45% of the budget estimate of Rs 18.23 lakh crore for the current financial year. In the last financial year 2022-23, direct tax collection was Rs 16.61 lakh crore.

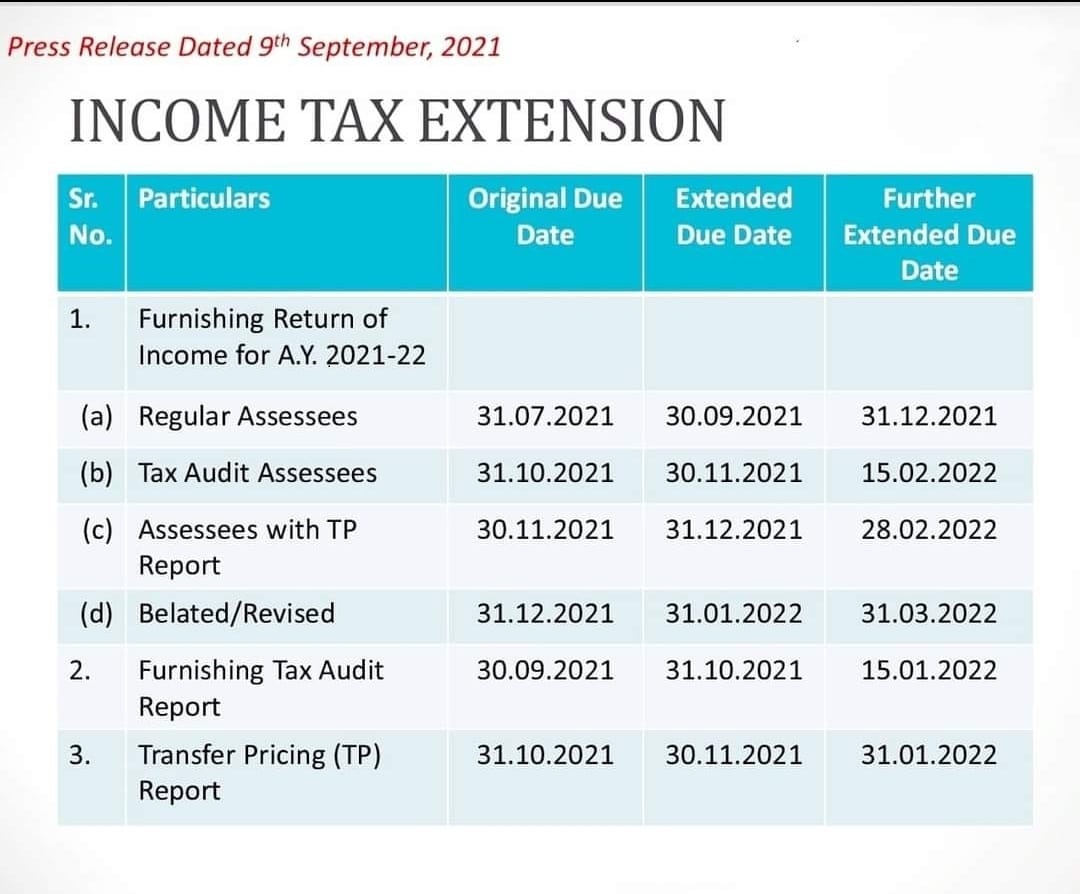

• This is the second time this financial year the government has extended the deadline of filing ITR for individuals whose accounts are not required to be audited. • The ITR filing deadline has been extended due to the many technical issues related to the government’s newly launched tax filing portal. • The deadline of filing belated/revised ITR has been extended by two months to March 31, 2022.

The government on Thursday extended the deadline to file income tax return (ITR) for FY 2020-21 by 3 months to December 31, 2021 from September 30, 2021. The extension of the deadline is for those individuals whose accounts are not required to be audited and who usually file their income tax return using ITR-1 or ITR-4 forms, as applicable.

In a statement, the Finance Ministry said that the decision has been on consideration of difficulties reported by the taxpayers and other stakeholders in filing of Income Tax Returns and various reports of audit for the Assessment Year 2021-22 under the Income Tax Act, 1961.

The income tax return (ITR) filing deadline for FY 2020-21 for individuals has already been extended, from the normal deadline of July 31, 2021. However, the new income tax e-filing portal has been marred by glitches and other problems from inception. Finance minister Nirmala Sitharaman has given Infosys, the company which set up the new income tax portal, time till September 15, 2021 to fix all the problems.

Last year too, the government has extended the due date of filing ITR for individuals four times – first from July 31 to November 30, 2020, then to December 31, 2020, and finally to January 10, 2021.

“On consideration of difficulties reported by the taxpayers in filing of Income Tax Returns(ITRs) & Audit reports for AY 2021-22 under the ITAct, 1961, CBDT further extends the due dates for filing of ITRs & Audit reports for AY 21-22. Circular No.17/2021 dated 09.09.2021 issued,” I-T Department tweeted on Thursday.

The due date of furnishing of report of audit under any provision of the Act for the previous year 2020-21, has been extended to January 15, 2022.

The due date of furnishing report from an accountant by persons entering into international transaction or specified domestic transaction under section 92E of the Act for the previous year 2020-21, is now January 31, 2022.

Again, the IT Department has decided to extend the due date of furnishing of Return of Income for the AY 2021-22, to February 15, 2022, among several other extensions.

The due date of furnishing of Return of Income for the Assessment Year 2021-22, which was December 31, 2021 has also been extended to February 28, 2022.

The due date of furnishing of belated or revised return of Income for the AY 2021-22 has been further extended to March 31, 2022.

Missing the ITR filing deadline would have had penal consequences. A late filing fee of Rs 5,000 would be levied if the ITR is filed by an individual after the expiry of the deadline.

Do keep in mind that government has also extended the deadline of filing belated ITR by one month from new deadline of December 31, 2021, to January 31, 2022. If the ITR is not filed by January 31, 2022, then the individual will not be able to file ITR for FY 2020-21, unless a notice is issued by the income tax department.

A late filing fee of Rs 5,000 along with penal interest at the rate of 1 per cent per month will be levied on the non-payment of tax dues in this case.

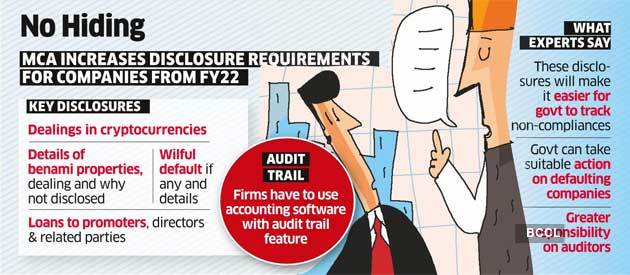

Starting April 1, companies must state if they have been declared wilful defaulters by banks, financial institutions or other lenders. The ministry also mandated companies to record audit trails of their accounts. Firms using accounting software to maintain their books need to use features that can record the audit trail of each transaction and create an edit log, including the date of such changes.

India Inc will have to declare investments in cryptocurrencies, relationships with dissolved companies and loans extended to related parties, among a host of other disclosures mandated by the government to improve transparency.

Starting April 1, companies must state if they have been declared wilful defaulters by banks, financial institutions or other lenders.

The ministry of corporate affairs announced a new set of disclosures rules under the Companies Act on Wednesday, significantly enhancing financial and general reporting requirements for companies.

The ministry also mandated companies to record audit trails of their accounts. Firms using accounting software to maintain their books need to use features that can record the audit trail of each transaction and create an edit log, including the date of such changes.

Amending the Companies (Accounts) Rules, the ministry said firms must ensure the audit trail feature on the accounting software cannot be disabled. The move is aimed at curbing backdated entries and will affect mainly smaller companies as the bigger ones already use such software, according to Shalu Kedia, a partner at Nangia & Co.

Additional disclosures to be made under schedule III of the Companies Act, 2013, relate to matters such as corporate social responsibility spending, cryptocurrency dealings, benami property, relationship with struck-off, or dissolved, companies, and ageing of payables & receivables with vendors.

These disclosures will make it easier for the government to track non-compliance and take action against defaulting companies, experts said.

“Earlier, the companies were only required to disclose trade payables and receivables, but there was no requirement to provide ageing details. This disclosure will mandate the company to disclose the ageing payment cycle for MSMEs and non-MSME vendors,” said Nischal Arora, a partner at Nangia Andersen LLP.

Dealings in cryptocurrencies must be disclosed with details of the profit or loss on such transactions, amounts of such currency held and deposits or advances from any person for trading or investing in these currencies.

“While the government is already working on a bill on cryptocurrency, the disclosure for such currency has made it clear that the government wants to gather data on cryptocurrency,” said Arora.

Another important change was related to the disclosure of any benami property holdings.

“This disclosure is another step to improve transparency for the stakeholders as they will have to disclose any proceeding that has been initiated or pending against the company for holding any benami property and also provide a reasoning and view on the same,” said Amit Maheshwari, a partner at AKM Global.

The additional disclosures will make it mandatory for companies to provide details of shortfall in CSR spending for the previous years, including reasons for not meeting targets.

Loans granted to promoters, directors and related parties that are repayable on demand or without specific repayment terms from companies must be declared in terms of amount and percentage to total loans granted.

While this will push firms to regularly service their loans, it “will be helpful for the investor and other lenders to be aware about these types of companies before making any investment or lending the money,” Maheshwari said.

MCA relaxes levy of additional fees in filing of e-forms AOC-4, AOC-4 (CFS), AOC-4 XBRL and AOC-4 Non-XBRL for the financial year ended on 31.03.2020 under the Companies Act, 2013

Keeping in view of various requests received from stakeholders regarding relaxation on levy of additional fees for annual financial statement filings required to be done for the financial year ended on 31.03.2020, it has been decided that no additional fees shall be levied upto 15.02.2021 for the filing of e-forms AOC-4, AOC-4 (CFS), AOC-4 XBRL and AQC-4 Non-XBRL in respect of the financial year ended on 31.03.2020.

During the said period, only normal fees shall be payable for the filing of the aforementioned e-forms.

Earlier, the Annual General Meeting for adoption of the Audited Financial Statements, Directors Report and Auditors’ Report was extended by 3 months from September 30 to December 30, 2020.

Accordingly, the companies were required file Audited Financial Statements before January 31st, 2021.

This has now been further relaxed for another 15 days up to February 15, 2021, for filing of the eForms with Ministry of Corporate affairs (MCA).

The RBI notified Rotation Policy instead of Cooling Period for Bank Branch Audit for CAs.

The Reserve Bank of India (RBI) notified the change in norms on eligibility, empanelment, the appointment of Statutory Branch Auditors in Public Sector Banks from years 2020-21 onwards.

The RBI notified Rotation Policy instead of Cooling Period for Bank Branch Audit for CAs. In other words, the concept of compulsory rest for two years for audit firms located in the specified centres, after completion of four years of continuous branch audit, followed till Financial Year 2019-20 has been done away with.

Instead, the branch auditors across all the centres of the country, on completion of four years of continuous branch audit, will be subjected to the policy of rotation i.e. they may be considered for appointment as SBAs of any other PSB.

However, the audit firms will not be eligible to be re-appointed as SBAs, in the same bank where they completed their audit assignment prior to rest/rotation, at least for one cycle of four years.

The RBI further notified the change on norms for selection of branches of Public Sector Banks (PSBs) for Statutory Audit.

Firstly, statutory branch audit of PSBs should be carried out so as to cover 90% of all funded and 90% of all non-funded credit exposures of a bank.

The selection of branches for statutory audit shall include a representative cross section of rural/semi-urban/urban and metropolitan branches, predominantly including branches which are not subjected to concurrent audit.

CPUs/LPUs/and other centralised hubs, by whatever nomenclature called, would be included for branch audit every year.

The selection of branches shall be finalised by each PSB with the consent of their Statutory Central Auditor/s. Secondly, in respect of those branches, which are subject to concurrent audit by chartered accountants and not selected for branch audit, LFARs and other certifications done by concurrent auditors will be submitted to the Managing Director & CEO of the bank.

The banks in turn will consolidate/compile all such LFARs and other certifications submitted by the Concurrent Auditors and submit to Statutory Central Auditor/s as an internal document of the bank.

The RBI notified the change in the procedure for appointment of Statutory Branch Auditors.

Firstly, the list of eligible auditors/audit firms will be prepared by the Institute of Chartered Accountants of India (ICAI) as per the norms prescribed by RBI.

Secondly, the list will be subjected to scrutiny by RBI for identifying the continuing and rested firms and excluding audit firms who have been denied audit.

Thirdly, RBI will, thereafter, forward the final list of all eligible auditors/audit firms to PSBs for selection of the required number of branch auditors/audit firms.

Banks will be required to clearly advise the selected audit firms that each audit firm can take up audit assignments (branch audit) in one PSB only. The audit firm should give its consent in writing for consideration of appointment in the bank concerned for the particular year and the subsequent continuing years.

Fourthly, the consent given by an audit firm is irrevocable and no request from audit firms for changing the bank, after giving its consent will be entertained.

Fifthly, after the selection of branch auditors, PSBs will be required to recommend the names of both continuing and selected branch auditors to RBI for seeking its prior approval before their actual appointment, as per statutory requirement.

The RBI while elaboration on the change in general guidelines applicable to appointment of Statutory Branch Auditors stated that SBAs will have a maximum tenure of four years in a particular bank.

The appointment of SBAs will be made on an annual basis, subject to their fulfilling the eligibility norms prescribed by RBI from time to time, and also subject to their suitability.

“While allotting branches, banks are required to select auditors/audit firms which are in close proximity to their offices/branches. Banks are also required to have a suitable mix of various categories of auditors / audit firms while selecting the branch auditors keeping in view the size of the branches to be audited.

Banks are advised to allot branches, to the extent possible, to the audit firms taking into consideration their category and audit experience in such a way that specialised and larger branches are audited by bigger/experienced audit firms,” the RBI said.

The audit firms retiring as Statutory Central Auditors from a PSB shall not be eligible to be appointed as SBAs of the same PSB during the prescribed cooling period for SCAs from that particular PSB.

The RBI notified change in the eligibility norms for the empanelment of audit firms to be appointed as Statutory Branch Auditors in PSBs.

The Institute of Chartered Accountants of India, in its gazette notification had made the generation of UDIN from the ICAI website mandatory for every kind of certificate/tax audit report and other attests made by their members as required by various regulators. This was introduced to curb fake certifications by non-CAs misrepresenting themselves as Chartered Accountants

The income tax department will validate with the Institute of Chartered Accountants of India (ICAI) the unique document identification number (UDIN) of chartered accountants when they upload tax audit reports, the finance ministry said on Thursday.

To curb fake certifications by non-CAs misrepresenting themselves as chartered accountants, the ICAI in 2019 made generation of UDIN from the ICAI website mandatory for every kind of certificate and tax audit report and other attests made by their members as required by various regulators.

The ministry said that in line with the ongoing initiatives of the income tax department for integrating with other government agencies and bodies, income-tax e-filing portal has completed its integration with the ICAI portal for validation of UDIN generated from the ICAI portal by the chartered accountants for documents certified/attested by them.

Income-tax e-filing portal had already factored mandatory quoting of UDIN with effect from April 27, 2020, for documents certified/attested in compliance with the Income Tax Act,1961 by a chartered accountant.

“With this system level integration, UDIN provided for the audit reports/certificates submitted by the chartered accountants in the e-filing portal shall be validated online with the ICAI,” the ministry added.

It said this will help in weeding out fake or incorrect tax audit reports not duly authenticated with the ICAI.

If a chartered accountant was not able to generate UDIN before submission of audit report or certificate, the e-filing portal permits such submission, subject to the CA updating the UDIN within 5 calendar days from the date of form submission in the income tax e-filing portal.

If the UDIN for the audit report/certificate is not updated within the 15 days, such audit report and certificate uploaded shall be treated as invalid submission, the ministry added.

In a statement, the Department of Revenue (DoR) reiterated that there will be no extra compliance burden on the taxpayers for GST turnover displayed in the Form 26AS, which is an annual consolidated tax statement that can be accessed from the income-tax website by taxpayers using their Permanent Account Number (PAN).

Prime Minister Narendra Modi launched GST into operation on the 1 st of July, 2017. GST was publicised as ‘one nation, one tax’ by the government, aimed to provide a simplified, single tax regime. GST is a dual levy where the Central Government levies and collects Central GST (CGST) and the State levies and collects State GST (SGST) on intra-state supply of goods or services. Centre also levies and collects Integrated GST (IGST) on inter-state supply of goods or services. The GST Portal is a website where all the compliance activities of GST can be done before and after GST login. Activities such as the GST registration return filing, payment of taxes, application for refund, etc. can be done on the GST Portal.

GSTN, recently launched many new features on GSTN portal. One of its features is that GSTN portal is now showing aggregate annual turnover for previous financial year after logging in to the portal.

The GST turnover is being shown in 26AS just for the information of the taxpayer. DoR acknowledged that there may be some differences in GSTR-3Bs filed and the GST shown in the Form 26AS but it can’t happen that a person shows turnover of crores of rupees in GST and doesn’t pay a single rupee of income tax.

The DoR said that the notified Income Tax Return for the current AY 2020-21 already requires reporting of GST outward supplies in the Schedule GST.

Therefore, the information displayed in Form 26AS would provide ease of compliance to the taxpayers in filling Schedule GST.

The revenue department has noticed that many unscrupulous persons are trying to avail or pass on input tax credit fraudulently by generating fake invoices and has already formulated a strategy for identifying these fake invoice generators which inter alia takes into account the income tax profiles of the suspected fake invoice generators.

These persons in most of the cases never file their income tax returns or disclose very meagre taxable income in the income tax return.

The suspected fake invoice generators are being identified for serious action under GST and other laws including suspension of their GST registration based on the fact that whether their income tax payment commensurate with the expected profit margin on turnover reported by them in the GST returns, the DoR said.

What “aggregate turnover” means?

“Aggregate turnover” is the aggregate value of all taxable supplies, exports of goods or/and services or both, exempt supplies and interstate supplies of persons having the same PAN, to be computed on all India basis. However, such taxable supplies do not include the value of inward supplies on which GST is being paid under reverse charge basis. The aggregate turnover also excludes Central tax, State tax, Union territory tax, Integrated tax and cess.

Basically, sum of the following shall be considered as an aggregate turnover:

Value of all taxable supplies of goods and services

Value of all Inter-state supplies

Value of all exempt supplies of goods and services

Value of all export of goods or services or both

However, the following items would be excluded from Turnover:

Inward supplies on which taxes are paid under reverse charge

Taxes and cesses under GST

Interstate supply of services

Transactions which are neither supply of goods or service.

Supplies provided outside India or received outside India

Extrapolation of Turnover at GSTIN level (for those who have not filed all the returns as per their eligibility or liability)

GSTIN-wise GSTR-3B turnover for FY 2019-2020 has been extrapolated by the formula: >> Total turnover declared as per all GSTR-3B filed / No. of GSTR-3B filed) X No. of GSTR-3B eligible or liable to be filed

GSTIN-wise CMP-08 outward supply has been extrapolated by the formula: >> Total outward supply declared as per all CMP-08 filed / No. of CMP-08 filed) X No. of CMP- 08 eligible or liable to be filed

Added both the values of S. No. (a) and S. No. (b).

For those taxpayers who have filed all the returns as per their respective eligibilities, value of S. No. (c) will be the actual turnover)

Aggregation of extrapolated turnover at PAN level or Annual Aggregate Turnover Resultant values as per S.No. (c) above are aggregated or rolled up at PAN level to arrive at the Annual Aggregate Turnover.

What is the relevance of knowing aggregate turnover?

The aggregate turnover is a crucial parameter for determining the following aspects:

Determining whether registration is required or not-

Aggregate Turnover is relevant for a person to determine threshold limit to obtain registration under GST.

Threshold turnover limit for exclusively supply of goods = Rs 40 lakh (Rs 20 lakh in case of supplies effected from special category states)

Threshold turnover limit for supply of Services or (goods and services both): Rs 20 lakh (Rs 10 lakh in case of supplies effected from special category states)

Determine the limit of composition levy – Threshold limit to opt for composition scheme: Rs 1.5 crore in a financial year (Rs 75 lakh in case of supplies effected from special category states).

To determine a “Taxable person” – Section 2 of CGST Act defines the “taxable person” as a person who has obtained registration or is liable to register as per section 22 and 24 of CGST Act. Here the Section 22 provides a liability to register when the tax payer’s turnover exceeds the limit as determined in certain cases. This is again based on aggregate turnover.

Calculation of Late fee –

Under section 33 any registered taxable person person who fails to file the return u/s 30 i.e Annual return shall be liable to pay late fees of Rs. 100 for every day when such failure continues subject to a maximum of an amount of 0.25% of his aggregate turnover.

This can escalate the amount of late fee because aggregate turnover will include all supplies except reverse charge.

To determine whether Audit is required –

Registered persons with an aggregate turnover exceeding the prescribed GST audit limit of Rs 2 Crore during a financial year are liable for GST Audit. The turnover limit of Rs 2 Crore is same for the registered tax persons across all States and UTs. Thus, no separate turnover limit is defined for Special Category States for GST Audit.

Therefore, it is advised to carry on the computation of aggregate turnover accurately as the same will be used at a number of places which will in turn determine the tax liability of a person.