Gujarat is followed by Delhi, Andhra Pradesh, Haryana, Telangana, Tamil Nadu, Kerala, Maharashtra, Karnataka and Madhya Pradesh.

Gujarat has retained the top position in the list of 21 states and UTs with most investment potential, according to a report by economic think-tank NCAER.

Gujarat is followed by Delhi, Andhra Pradesh, Haryana, Telangana, Tamil Nadu, Kerala, Maharashtra, Karnataka and Madhya Pradesh.

The ranking of 20 states and one Union Territory of Delhi was based on six pillars — labour, infrastructure, economic climate, governance and political stability, perceptions and land — and 51 sub-indicators.

While Gujarat topped in economic climate and perceptions, Delhi ranked one in infrastructure. While Tamil Nadu topped the chart in labour issues, Madhya Pradesh ranked one in land pillar.

The National Council of Applied Economic Research (NCAER) State Investment Potential Index (N-SIPI 2017) report ranks states on their competitiveness in business and their investment climate.

Compared to 2016, Gujarat and Delhi again top the list of states, while Haryana and Telangana have moved rapidly up the ranks to finish among the top five, it said.

NCAER Director-General Shekhar Shah said: “Investment opportunities are expanding in India in all sectors. The GST will weave India’s states together in ways that has not been possible before”.

Further the report said that although Bihar, Uttar Pradesh and West Bengal are ranked among the least favourable states for investment, they rank higher under individual pillars.

Indira Iyer, the team leader for the 2017 N-SIPI, stated that as per the report, “corruption” continues to be the number one constraint faced by businesses.

However, she said, the 2017 N-SIPI reports a decline in the percentage of respondents citing corruption as a constraint to conducting business from 79 per cent in 2016 to 57 per cent in 2017.

Getting approvals for starting a business is still the second-most pressing constraint faced by businesses in 2017 as was the case in 2016, she added.

Talking about this index, Department of Industrial Policy and Promotion (DIPP) Secretary Ramesh Abhishek said these reports are aiding states in improving the business climate and attracting investors.

PE, Venture Capital flows up 155% in May to $ 3 billion; SoftBank – Paytm deal tops

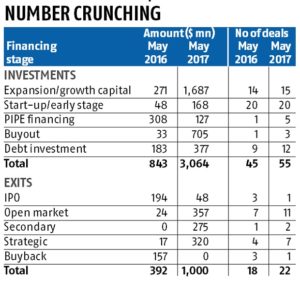

Private equity and venture capital (PE/VC) investments have recorded the highest monthly investments in the past 10 years at $3.1 billion in May 2017. For the third consecutive month in a year, the investment flow crossed the $2-billion mark.

The financial services sector topped the table on account of the $1.4-billion investment by Softbank in Paytm. This deal accounted 46 per cent of aggregate deal value for the month.

According to Ernst & Young (EY) data, the month recorded a 264 per cent increase in terms of value and 23 per cent in volume over May 2016. PE/VCs have invested $3,064 million across 55 deal in May this year as against $843 million across 45 deals in May 2016.

There were five deals of more than $100 million aggregating to $2.3 billion, accounting for 75 per cent of the aggregate deal value in May 2017.

Another important deal during the month was the $500-million investment by Canada Pension Plan Investment Board (CPPIB) in Indospace (a real estate platform for industrial and logistics parks) for a majority stake, thus taking the investments by Canadian pension funds in 2017 close to $2 billion.

Mayank Rastogi, partner and leader for PE, EY said that Indian PE/VC market has significantly matured over time. Five to seven years ago, the classic growth capital was the only meaningful capital pool available with limitations such as investment horizon and return expectations, and could not have suited some specific situations.

There are a variety of capital pools available ranging from angel/VC to buyout funds, family offices, pensions and sovereigns, corporate funds, debt funds, sector-focused funds providing solutions that address specific needs. This is one of the key drivers for continuing buoyancy in the PE/VC investments in India despite slow growth capital investing.

Financial services ($1.6 billion across 11 deals) emerged as the most active sector on account of the Paytm-Softbank deal, the largest deal in the financial services sector till date. The real estate sector bagged four deals worth $709 million, followed by e-commerce sector’s six deals worth $211 million in terms of activity.

May 2017 recorded $1 billion in exits and was the second consecutive month with more than $1 billion in exits.

The strong buyout trend established over the past two years continued into 2017 with $2 billion invested across 18 deals till date.

Between January and May, there was a significant increase of over 60 per cent compared to 2016 and over 100 per cent compared to 2015, both, in terms of value and volume.

Debt deals recorded the biggest monthly volume since 2014 with $377 million recorded across 12 deals.

Given the buoyancy in the public markets, open market deals emerged as the preferred mode of exit, accounting for 36 per cent of exits by value and 50 per cent by volume, similar to the trend seen in the previous month.

Till date, open market exits have accounted for 49 per cent of the total value of exits in 2017 compared to 25 per cent for the whole of 2016. May 2017 recorded $90 million in fund raise, a decline of 82 per cent and 76 per cent as compared to May 2016 and April 2017 respectively. The plans for fund raise announced during the month stood at $908 million.

There was one PE-backed initial public offering (IPO) in May 2017 (S Chand, a publishing company, primarily in the education space), which saw Everstone exiting a 13.9 per cent stake for $48 million. Till May 2017, PE-backed IPO tally stands at four compared to eight during the same period in 2016.

Financial services emerged as the leading sector with exits worth $466 million across six deals followed by the healthcare sector with exits worth $260 million across three deals.

The resolution of the vexed issue of massive non-performing assets (NPAs) in the banking system is a work in progress and some “visible action” will be initiated over the next few days under the NPA ordinance promulgated recently, finance and defence minister Arun Jaitley said.

The resolution of the vexed issue of massive non-performing assets (NPAs) in the banking system is a work in progress and some “visible action” will be initiated over the next few days under the NPA ordinance promulgated recently, finance and defence minister Arun Jaitley said on Thursday.

“The RBI was taking measures under the existing mechanism. We have now taken other steps and there would be visible action taken under the new mechanism in the next few days,” Jaitley said, addressing media on achievements of the ministries under him over the past three years. The Centre won’t provide any special package to any state to waive farm loans but the states are free to spend from their own budgets should they take any such decision, the minister said.

Here are few excerpts from FM’s media briefing:

On NPAs and other things constraining private investments

Massive toxic assets impact the ability of banks to support growth, although record levels of foreign direct investments (gross FDI inflows touched $60 billion in 2016-17) and higher government spending have offset inadequate private investments to a certain extent. Linked to it (NPAs) is the challenge of wanting to increase private sector investment, even though our FDI and public investments have significantly increased. And of course there is a significant (adverse) impact of the global situation also (on private investments).

“Note ban not sole reason for Q4 GDP slowdown”

Demonetisation could be one of the several factors, and not the sole reason, that contributed to the slowdown of GDP growth to an 8 quarter-low of 6.1% in Q42016-17. What you think is very clear (that note ban dragged down Q4 growth) isn’t very clear. There are several factors which can contribute to GDP in a particular quarter. There was some slowdown visible, given the global and domestic situations, even prior to demonetisation in the last year. Financial services, which used to have 9-10% growth, has come down (to 2.2% in Q42016-17). Under the current global situation, 7-8% growth, which is at the moment the Indian normal, is fairly reasonable by our own standard and very good by global standards.

And I am sure as the impact of all these policies (taken by the government) holds out, growth will gather momentum. There won’t be any adverse impact of GST on GDP growth. The GST by itself should normally add to growth.

(Chief economic adviser Arvind Subramanian pointed out that under the GST, the incidence of tax is going to come down. While there could be some teething problem in implementation, at the most, initially, the tax cut would be positive to both reduce inflation and stimulate consumption).

On Pradhan Mantri Garib Kalyan Yojana

PMGKY wasn’t an isolated scheme in last financial year. First we introduced the Income Disclosure Scheme; after the IDS, there was a (post-demonetisation) phase of people depositing cash in the banking system. And the PMGKY was over and above these. To assess the total amount of (black money) disclosures made, you have to look at all the three collectively.

Revenue secretary Hasmukh Adhia said the response to PMGKY hasn’t been very good; only Rs 5,000 crore has been declared under the scheme. There are mainly two reasons for it. First, even before the scheme was announced, people had tried to deposit their cash in different accounts and tried to “adjust their money”. Secondly, many people found the (PMGKY) rate – 50% tax plus 25% as interest-free for four years – too high).

No central funds for farm loan waiver by states

The Centre won’t provide any special package to any state to waive farm loans but states are free to spend from their own budgets should they take any such decision. The Centre will continue to provide the states funds in accordance with the latest Finance Commission suggestions, and not more to waive farm loans (clarified that states are free to take decision on farm loan waivers from their own budgets but they have to stick to the 3% fiscal deficit target, as stipulated under the fiscal responsibility legislation).

On Air India

As far as AI is concerned, Niti Aayog has given its suggestion to the civil aviation ministry and the ministry will have to explore all the options for divestment or privatisation of the airline. The civil aviation minister will now devise the methodology ( for disinvestment / privatisation). As far the merger of oil PSUs are concerned, the petroleum ministry will have to take a call.

On “jobless growth”

Jobs aren’t created outside the economic structure. If the economy grows then it’s only natural that the formal sector would create jobs and in this country job creation is even faster in the informal sector. Since there is no firm statistics available on job growth in the informal sector, the term ‘jobless growth’ is being bandied about.

On the amount of demonetised currency

On the total currency given to the banks, the RBI used to give the figures frequently during the process of demonetisation, but now that the exercise is complete, as a responsible institution it can’t give an approximation. Today, every currency note is to be counted and if there are counterfeits these also need to be counted before arriving at the real count. The exercise is enormous and large but the RBI will give the accurate figure when it is complete.

Even as the World Bank has revised India’s growth figures by 0.4 percentage points as compared to its January forecast, India remains the fastest growing major economy in the world, the World Bank officials said.

Noting that India is recovering from the temporary adverse effects of demonetisation, the World Bank has projected a strong 7.2 per cent growth rate for India this year against 6.8 per cent growth in 2016.

Even as the World Bank has revised India’s growth figures by 0.4 percentage points as compared to its January forecast, India remains the fastest growing major economy in the world, the World Bank officials said.

The growth projections for China remains unchanged at 6.5 per cent for 2017 and then 6.3 per cent for the next two years 2018 and 2019. The World Bank in its latest Global Economic Prospects, projects India’s growth to 7.5 per cent in 2018 and 7.7 per cent in 2019.

In both the years, the forecast has been downgraded by 0.3 per cent and 0.1 percentage points as compared to the January 2017 forecast.

“A downgrade to India’s fast pace of expansion,” the World Bank said, is “mainly reflecting a softer-than-expected recovery in private investment.”

In 2016, in India, activity was underpinned by favourable monsoon rains that supported agriculture and rural consumption, an increase in infrastructure spending, and robust government consumption, the report said.

“In India, recent data indicate a rebound this year, with the easing of cash shortages and rising exports. An increase in government spending in India, including on capital formation, has partially offset soft private investment,” it said.

“While manufacturing Purchasing Managers’ Indexes have generally picked up, industrial production has been mixed,” the Bank said in its latest report.

Observing that India’s growth is forecast to increase to 7.2 per cent in Financial Year 2017 and accelerate to 7.7 per cent by 2019, is slightly below previous projections, the Bank said this outlook mainly reflects a more protracted recovery in private investment than previously envisaged.

“Nonetheless, domestic demand is expected to remain strong, supported by ongoing policy reforms, especially the introduction of the nationwide Goods and Services Tax (GST),” it said.

“Significant gains by the ruling party in state elections should support the government’s economic reform agenda, which aims at unlocking supply constraints, and creating a business environment that is more conducive to private investment,” the Bank said.

M Ayhan Kose, Director of the World Bank Group’s Development Prospects Group, in response to a question, underscored the need of reforms in the banking sector.

“The government has especially taken steps to address the banking sector weakness, but that remains on the to-do list,” Kose told PTI.

“Second (to do list) of course is the initiative by the government to remove some of the public investments, exactly the right thing to do to stimulate – to try to reinvigorate -private investment, which has been weak,” the Bank official said in response to a question.

The Real Estate (Regulation and Development) Act , 2016, or RERA, aims to protect home buyers and encourage genuine private players

The much-awaited Real Estate Act comes into force from Monday with a promise of protecting the right of consumers and ushering in transparency but only 13 states and Union Territories (UTs) have so far notified rules.

The government has described the implementation of the consumer-centric Act as the beginning of an era where the consumer in king. Real estate players have also welcomed the implementation of the Act, saying it will bring a paradigm change in the way the Indian real estate sector functions. The government has brought in the legislation to protect home buyers and encourage genuine private players.

The Real Estate (Regulation and Development) Bill, 2016, (RERA Act), was passed by Parliament in March last year and all the 92 sections of the Act comes into effect from 1 May. “The Real Estate Act coming into force after a nine-year wait and marks the beginning of a new era,” Housing and urban poverty alleviation (HUPA) minister M. Venkaiah Naidu said. The minister said the law will make “buyer the king”, while developers will also benefit from the increased buyers’ confidence in the regulated environment.

“The Act ushers in the much-desired accountability, transparency and efficiency in the sector, defining the rights and obligations of both the buyers and developers,” Naidu said. The developers will now have to get the ongoing projects that have not received completion certificate and the new projects registered with regulatory authorities within 3 months from Monday.

Under the rules, it is mandatory for the states and UTs to set up the authority. However, only 13 states and UTs have so far notified the rules. The states that have notified the rules are Uttar Pradesh, Gujarat, Odisha, Andhra Pradesh, Maharasthra, Madhya Pradesh and Bihar.

The housing ministry had last year notified the rules for five UTs—Andaman and Nicobar Islands, Chandigarh, Dadra and Nagar Haveli, Daman and Diu, and Lakshadweep, while the urban development ministry came out with such rules for the National Capital Region of Delhi. The other states and UTs will have to come out with their own rules.

A HUPA ministry spokesperson said the ministry has been taking up the matter with all the states and UTs for implementation of the Act, requesting them to ensure action as per the provision of the Act within the time limit. The ministry had earlier formulated and circulated the model rules to the states and UTs for their adoption and it is their responsibility to notify the rules, the spokesperson said. Those states which have not notified the rules will face public pressure and even people could approach the court in the matter, he added. On reports that key provisions have been diluted by some states, he said it was pointed out to those states and they have assured the ministry that it would be corrected.

The Indian real estate sector involved over 76,000 companies across the county. Some of the major provisions of the Act, besides mandatory registration of projects and real estate agents, include depositing 70% of the funds collected from buyers in a separate bank account for construction of the project. This will ensure timely completion of the project as the funds could be withdrawn only for construction purposes. The law also prescribes penalties on developers who delay projects. All developers are required to disclose their project details on the regulator’s website, and provide quarterly updates on construction progress. In case of project delays, the onus of paying the monthly interest on bank loans taken for under-construction flats will lie on developers unlike earlier, when the burden fell on home buyers, said real estate service provider JLL India CEO and Country Head Ramesh Nair.

RERA also states that any structural or workmanship defects brought to the notice of a promoter within a period of five years from the date of handing over possession must be rectified by the promoter, without any further charge, within 30 days, he added. If the promoter fails to do so, the aggrieved allottee is entitled to receive compensation under RERA, Nair said.

Other highlight of the Act is imprisonment of up to three years for developers and up to one year in case of agents and buyers for violation of orders of appellate tribunals and regulatory authorities. As per industry data, real estate projects in the range of 2,349 to 4,488 were launched every year between 2011 and 2015, amounting to a total of 17,526 projects with investments of Rs13.70 lakh crore in 27 cities, including 15 state capitals. About ten lakh buyers invest every year with the dream of owning a house.

Real estate industry bodies Confederation of Real Estate Developers Associations of India (CREDAI) and National Real Estate Development Council (NAREDCO) said the implementation of this law will bring paradigm change in the way Indian real estate functions. They expect property demand to rise but supply may get affected in the near term. “It will bring a paradigm change in the real estate sector. It will protect buyers who have purchased flats in the past. The regulator under the RERA should find ways to help complete ongoing projects and provide relief to home buyers,” NAREDCO chairman Rajeev Talwar said.

CREDAI president Jaxay Shah said RERA will increase transparency in the sector and boost confidence of both domestic and foreign investors. He, however, said there will be some “teething problem” initially in implementation of this law. Asked about the impact on prices, Shah said, “Supply will dip during this year but demand will improve as buyers will have increased confidence about investing in the property market” The real estate prices will remain stable now but rates could rise by 10% in the next six months, he added.

A Universal Robots employee demonstrates how a model of their industrial robot arms works in Singapore March 3, 2017.

Foreign precision engineering firms are investing more in Singapore, drawn by strong semiconductor demand and government incentives aimed at re-tooling an economy short of skilled labor.

The city-state is running programs worth billions of dollars to support productivity, automation and research, attracting global chipmakers including U.S.-based Micron Technology Inc and Germany’s Infineon Technologies.

This investment rush into electronics helped the technology sector log 57 percent output growth on average in October-February from a year ago, and kept Singapore from recession late last year.

“I’ve lived in Europe, I’ve lived in Japan, I’ve spent a lot of time in Taiwan and other countries. From a proactive standpoint, Singapore is about as good as it gets,” said Wayne Allan, vice president of global manufacturing at Micron, adding the Singapore government’s long-term vision was key to Micron expanding its investment.

Taking advantage of government grants, Micron is investing $4 billion to make more flash-memory chips in Singapore. It increased output by a third in the second half of last year and expects similar growth in the first half of this year.

Linear Technology Corp, a maker of analog integrated circuits, has opened a third chip testing facility in Singapore, and will produce 90 percent of its global test equipment in the city-state.

All this has created something of a virtuous circle in the semiconductor supply chain, with chip testing equipment supplier Applied Materials reporting record shipments to Singapore last year, said its regional chief, Russell Tham.

It’s unclear how much of this revival in Singapore’s $40 billion chip industry is due to a so-called ultra-super-cycle in the global memory chip sector, and Singapore remains a smaller player than South Korea and Taiwan.

“It is vulnerable to a pull-back,” said Nomura economist Brian Tan. “If there’s a turnaround in the semiconductor industry … it becomes a lot more apparent that the underlying growth momentum is not great.”

MOVING UP

However, there are real signs that the targeted government incentives are helping firms move up the value chain.

One of the larger programs is the Productivity and Innovation Credit, where Singapore has budgeted S$3.6 billion ($2.6 billion) for 2016-18. Another S$400 million automation support package is aimed at small firms, and a S$500 million Future of Manufacturing plan encourages testing new technologies.

The Ministry of Trade and Industry says it encourages manufacturers to “embrace disruptive technologies” such as robotics. “These measures will help ensure the manufacturing sector in Singapore remains globally competitive,” it said, attributing the strong semiconductors performance partly to demand from China’s smartphone market and improved global semiconductor demand.

For Feinmetall Singapore, whose products are used for testing semiconductor wafers, grants covered about two thirds of the $100,000 cost of a needle-bending machine it needed to help overcome an island-wide labor shortage.

“If we use the same methods as before … I don’t think we can expect any growth,” said Sam Chee Wah, the company’s general manager, noting Feinmetall Singapore struggled to retain some workers for much longer than a year, even after nine months of training.

GlobalFoundries Singapore, a wafer maker, has spent $50 million on 77 robots, each able to perform the tasks of 3-4 workers. This has helped the company move up the value chain into parts for self-driving cars and security-related chips for credit cards and mobile payments, says general manager KC Ang.

Singapore now has about 400 robots per 10,000 workers, the world’s second-highest density after South Korea. Most robots are used in electronics, according to the International Federation of Robots.

And further developments are in the pipeline.

AUTOS, IOT

At its Singapore manufacturing hub, Infineon is developing productivity tools such as robotics and automated guided vehicles which it hopes to deploy to other production sites. Dutch chipmaker NXP Semiconductors is also developing vehicle-to-everything technology, enabling vehicles to communicate with each other and roadside infrastructure.

Instead of trying to compete with high-volume producers such as China or Malaysia, Singapore has shifted to higher-end products, said Jagadish C.V., head of Systems on Silicon Manufacturing, another firm making semiconductor wafers.

“So you do the products which others can’t do so easily,” he said, adding his firm had shifted most of its output to specialized products, such as chips used in smartphones.

CK Tan, President of the Singapore Semiconductor Industry Association, noted the global chip industry is automating faster than other sectors because of cost pressure, a need to eliminate or reduce error, and have a consistent process control.

“In Singapore, it’s even more important for us to … look at how to speed up or increase the level of automation because of the lack of skilled resources,” he said. “The industry has recognized it has to move upscale. The government incentives play a part to allow the manufacturing side to be relevant, to be at least cost competitive.”

The Ministry of Trade and Industry said first-quarter growth in manufacturing – up 6.6 percent year-on-year, while overall GDP was up 2.5 percent – was due mainly to output expansion in electronics and precision engineering.

Integrated circuits were Singapore’s biggest export product among non-oil domestic exports in January-March, topping S$6 billion ($4.29 billion), according to trade agency IE Singapore.

Japanese investor SoftBank has pumped in about Rs 1,675 crore in fresh funding in Indian transportation startup Ola to give it more muscle to take American rival Uber head-on.

SoftBank subsidiary SIMI Pacific Pte picked 12,97,945 shares valued at Rs 10 at a premium of Rs 12,895 in ANI Technologies — which runs Ola — filings with the Registrar of Companies showed.

The allotment of shares was done in November last year, it added.

The latest funding, however, is believed to have come at a lower valuation.

According to sources, the move comes at a time when Softbank is working on selling Snapdeal, an e-commerce platform it invested heavily in India, to larger rival Flipkart.

The Bengaluru-based firm was aggressively looking at raising funds to compete with Uber, the world’s most valuable start-up. After selling its Chinese business to Didi last year, Uber has now set sights on India making it one of its top priorities.

Though Indian Internet companies have seen a boom in user base, their valuations have come down as investors are now focusing on path to profitability and building a sustainable business model. Flush with private equity and venture capitalist money, many start-ups continue to have high burn rate that has been a concern for investors.

Earlier this week, India’s largest e-commerce firm Flipkart raised $1.4 billion from Tencent, eBay and Microsoft in a round that saw its valuation fall from $15 billion to $11.6 billion now.